PNRA remains on the Hedgeye Best Ideas list as a short.

We need to understand the following issues before we can determine the appropriate time to back off of our bearish call. Moving forward, the true test of capitulation will be on display in the form of new unit capital spending. Will management continue to accelerate unit growth, as they have stated they will, or will they reassess and decide to scale back this spending?

That being said, we had several questions come to mind following the 3Q13 earnings call:

- Do the planned “changes” represent a real solution? Or is management putting a band aid on the problem?

- How long will it take to implement these “changes”? Management was very vague in this regard.

- How are they addressing value and affordability?

- Despite strong new unit AUVs, should they really be accelerating, or even maintaining, new unit growth?

- Can the system handle all of these “changes” at once?

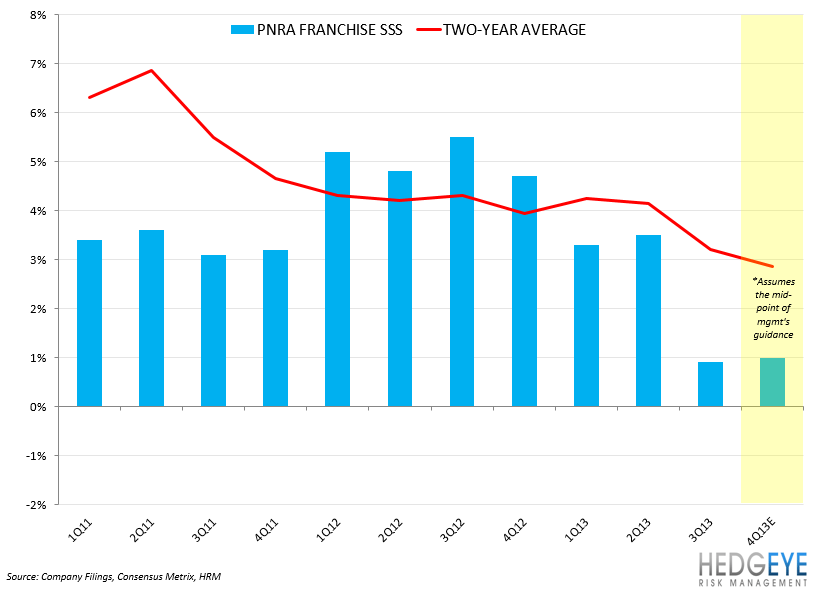

PNRA 3Q13 same-store sales of +1.7% missed consensus estimates of +2.9% and fell below the company’s guidance of +2-4%. Even worse, traffic was down -1% during the quarter, and has now been down for four consecutive quarters. We attribute this decline in traffic to the following:

- Choppy consumer environment

- Increased competition from Casual Dining companies due to aggressive discounting

- Self-inflicted throughput bottlenecks during the lunch day part

- The value equation is out of sync – price/mix is falling

- Cannibalization from new stores

What we liked in 3Q13 results:

- Management is aware of PNRAs issues

- Repurchased $174 million worth of shares in 3Q13

- Repurchased $69 million worth of shares to date in 4Q13 and have $317 million remaining under the authorized repurchase program

- Easier comps in 2014

- More achievable guidance is now in place

What we didn’t like in 3Q13 results:

- Low quality print

- Same-store sales growth missed consensus expectations and the guidance range

- Two-year sales trends are decelerating

- 3Q transaction growth was down -1%

- Two-year transaction trend is negative

- 4Q comp guidance revised down from +3-5% to +0-2%

- 4Q EPS guidance revised down from $2.05-$2.11 to $1.91-$1.97

- 4Q operating margin expected to be down 100-150 bps

- FY13 operating margin expected to be down 0-50 bps y/y

- FY13 comp guidance revised down from +3-5% to +2-2.75%

- Targeting FY14 EPS growth below the low-end of its long-term target (15-20%)

- The company has legitimate capacity and throughput issues

- Management does not appear to have a plan in place to improve their value proposition

The Wild Card:

- Will capacity and throughput issues inhibit the “demand drivers” PNRA has in place?

Management failed to give us the confidence to believe that they have a feasible plan in place to fix these operational issues and reverse negative traffic trends. In our view, increased advertising, menu additions, and other initiatives could exacerbate the problems the company faces today. Until management reveals their plan in more detail, we fear that they could be trying to do too much at one time.

Howard Penney

Managing Director