“Someone has to protect this family from the man who protects his family.”

-Skyler White

Who is Bernanke’s family? Who is Ben Bernanke? Who is John Galt? The People getting jammed with a trashed currency and 0% rate of return on their savings accounts want to know, “yo.” And they want to know now.

Yesterday’s all-time highs in the US stock market put a bloody pit in my stomach. I will not mince words about that and why this morning. Standing up to the tyranny of an un-elected-anti-dog-eat-dog-government-man is my Canadian-American patriotic duty.

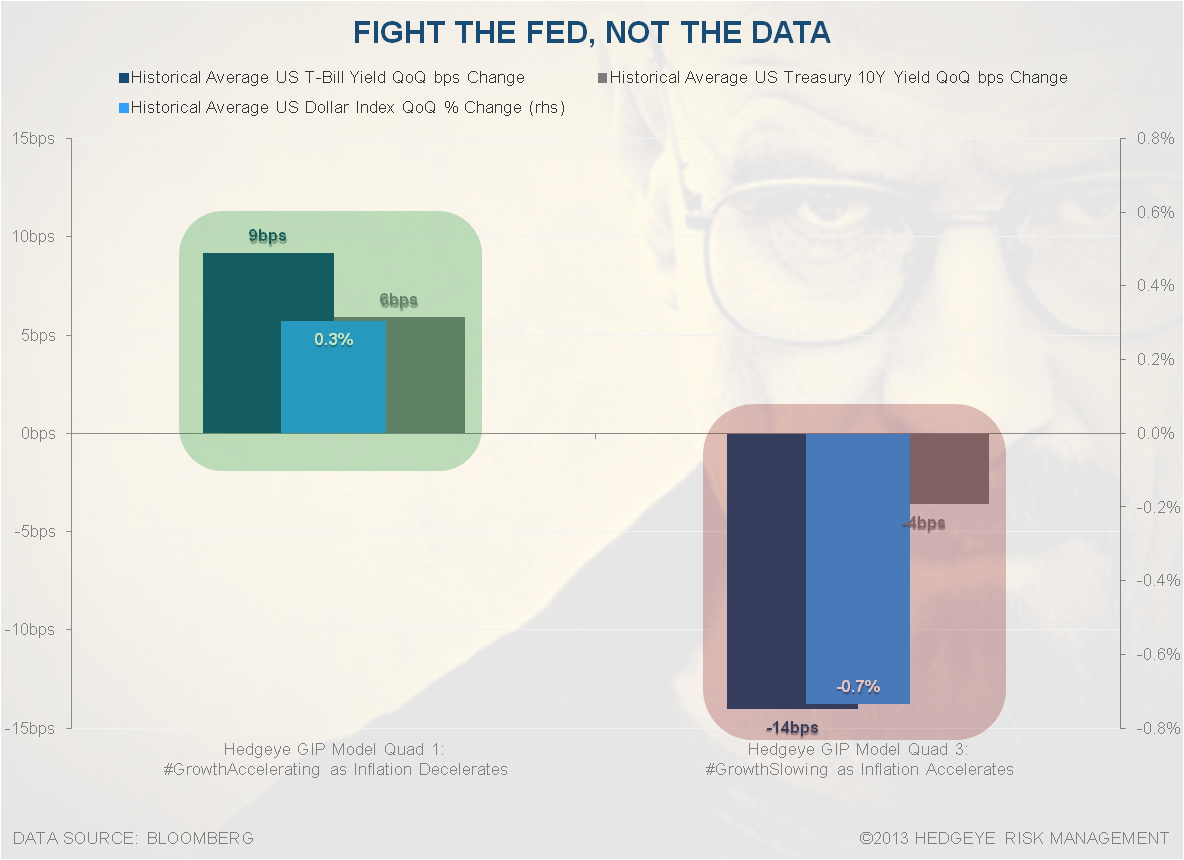

Ben, seriously. If you aren’t going to taper, ever, why? Who do you represent? Is it the people in the business of being long bonds? Or is it the government that appointed you to lead this ongoing fear-mongering campaign? Both of our leading indicators on US #GrowthAccelerating (#StrongDollar + #RatesRising) are breaking bad, again. This one is all on you.

Back to the Global Macro Grind…

“You clearly don’t know who you are talking to, so let me clue you in. I am not in danger, Skyler. I am the danger. A guy opens his door and gets shot, and you think that of me? No! I am the one who knocks!” –Walter White

That’s right Bernanke, I’m the one knocking. And it’s going to get louder if you keep this up. You can cart out everyone from PIMCO to Zervos at Jefferies to parrot whatever you think you are accomplishing here. I don’t buy it. You’re suspect.

I respect David Zervos’ penmanship and market views, so let’s break down why I think this could break bad versus what he thinks. We are two of the only consistent US stock market bulls of 2013 who have been bullish for completely different reasons:

- ZERVOS - he thinks US stocks up in 2013 is all about QE and that we cannot afford to taper as that would end it all

- MUCKER – I think the most important part of the 2013 rally was on expectations of ending QE; not tapering is a disaster

Bernanke and the entire levered long bond bull lobby agree with Zervos. And I actually have no idea who agrees with me, which is probably why our call on US #GrowthAccelerating from 0.38% in Q412 to 2.5% now was the only one of its ilk. Our growth model called US #GrowthSlowing in October 2007 too. US Dollar Devaluation back then was my leading indicator.

So which one is it?

Oh, by the way, all of US economic and market history agrees with my view that:

1. Strengthening currency + Rising Interest Rates = Pro-Growth Signals

2. Devalued currency + Falling Interest Rates = #GrowthSlowing signals

In buckets of time, you only have to look past your nose and go beyond the #EOW (end of the world) stuff (2008) and look at the last 40 years of US economic history to understand my point. Both Reagan and Clinton understood this. Nixon/Carter (1970s) and Bush/Obama (last decade) did not. Markets can go up when growth slows; especially slow-growth styles like Gold and Bonds.

For those of you who think “the stock market going up reflects the economy, so Bernanke is nailing it”, I’ll remind you that’s a crock. Venezuela devalued its currency by 32% this year; its stock market is +312%; and its economy sucks – a Policy to Inflate via currency debauchery is not growth. It’s called inflation.

From Nero (50 AD) to 1920s Germany to whatever Chavez left in Venezuela, do not get me wrong, Zervos is quite right that keeping your government stimulated with a meth market can take you for quite a ride, yo! But, again, do not confuse the kind of move we saw yesterday with the one we saw before Bernanke decided not to taper on September 18th.

Rewinding the tapes, here’s what happened yesterday:

- US monthly payroll number missed by enough to validate Bernanke’s bs storytelling that we don’t need to taper

- US Dollar got smoked to a fresh YTD low

- US Treasury Yields snapped my 2.58% TREND line on the 10yr

- Gold ripped

- Slow growth sectors like Utilities (XLU) had triple the intraday move of the SP500

Is that what you want, yo? Another epic 2007 style US stock market bubble? If you do, we can go right back to reflating the Housing, Gold, Bond, Utility, Foreign Currency, etc. Bubbles. Kinder Morgan can trade at 85x earnings on that too. Rock on, yo.

So what do you want? As my man Walter White would say, “you all know exactly who I am. Say my name.” That’s right. I’m the guy who believes in fiscal conservatism, monetary tapering, a strong currency, and rising interest rates. “Now say my name.”

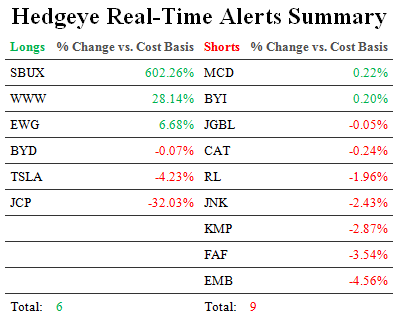

I’m the guy who went to net short yesterday (6 LONGS, 9 SHORTS in #RealTimeAlerts) and 54% Cash. Timestamped, yo. He’s Heisenberg. I’m going to roll with him, book gains, and protect my family and firm’s hard earned savings.

UST 10yr Yield 2.47-2.58%

SPX 1

VIX 11.55-14.96

USD 79.02-80.12

Euro 1.36-1.38

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer