But it’s still not a long.

Kimberly Clark reported $1.44 adjusted EPS this morning versus consensus of $1.40. The better-than-expected results were driven by organic sales growth of 5%, which is being well-received by the market. Management raised the lower end of its FY13 guidance range to $5.65-5.75 versus $5.60-5.75 prior. Strong organic sales numbers took us by surprise; we see no reason to be involved in KMB at this stage.

Summary

We have been bearish on Kimberly Clark since mid-July and, while the stock has underperformed, the recent performance strength and strong organic growth numbers reported by the company have weakened our conviction in shorting the stock here, in a pair with EL (as we proposed) or otherwise.

Contrary to our prior expectations, KMB will likely meet the Street’s FY13 EPS expectations as top line performance has accelerated into 2H13, despite some industry data previously suggesting that this could be a tall task. Dollar weakness is certainly helping and will be worth monitoring going forward.

Risks

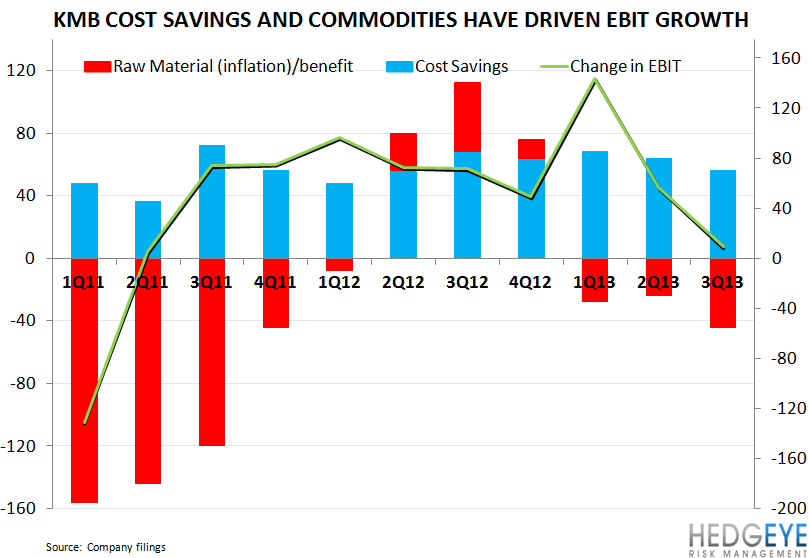

- EBIT growth is being driven by cost savings alone as revenue growth remains anemic. The market may be unwilling to pay an above-average multiple for peer-lagging revenue and earnings growth.

- We believe that input costs are worth monitoring over the remainder of the year as management’s guidance may be underestimating costs in 4Q13.

What we liked in 3Q13 Results:

- EPS beat, supported by organic sales growth of 5%

- Mgmt raised the low end of the guidance range by 5 cents

- Strong KC-International organic sales of 10% boosted by emerging markets (China, Russia, to a lesser extent Brazil) accelerating

- Sustained strong volume growth in emerging markets

- Operating cash flow aided by improved working capital efficiency

What we didn’t like in 3Q13 Results:

- EBIT growth decelerating further to 1% despite easier comp

- No Operating Margin expansion year-over-year

- Personal care operating margins declining 20bps

- Organic growth in Europe being boosted by phasing out of weak businesses

- Negative 3Q FCF growth (-0.5%) with EBIT growth slowing to +0.9% from +5.8% in 2Q13 despite management expecting cash flow generation to improve in 2H13 as of 7/22

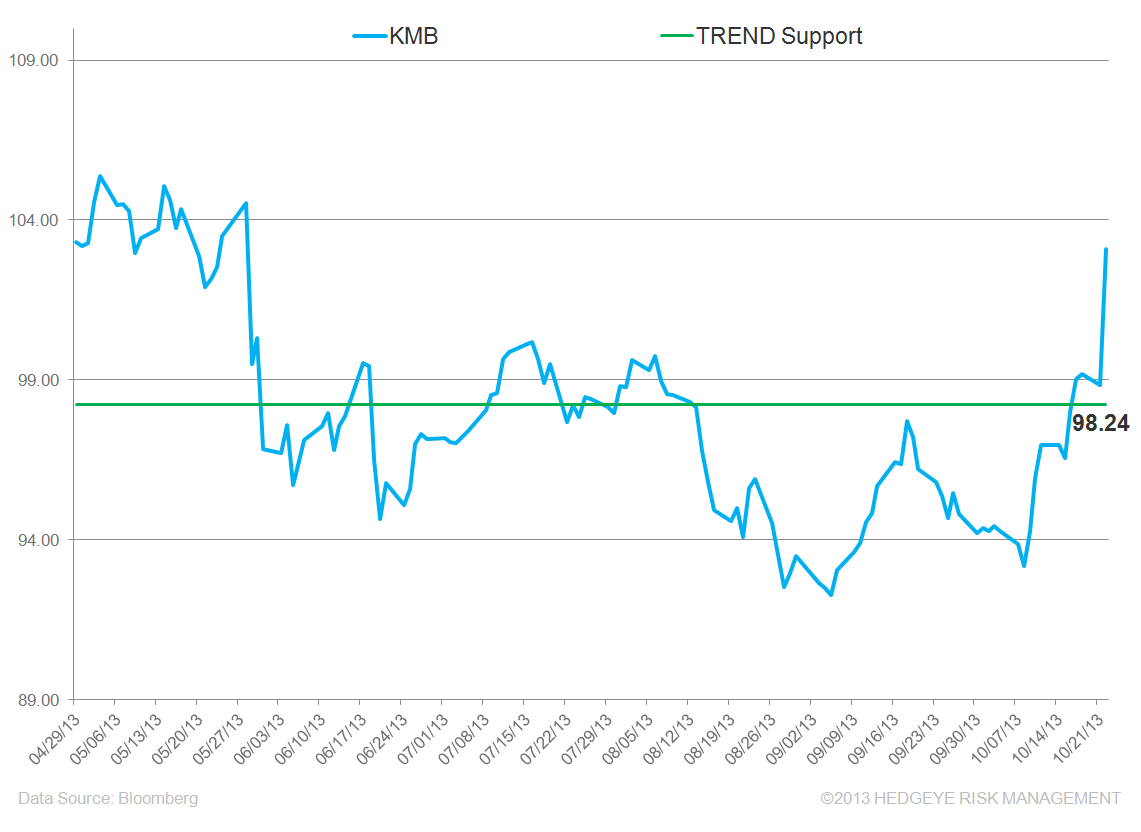

Quantitative Levels

From a quantitative perspective, KMB has broken out above its intermediate-term TREND line of $98.24.

Rory Green

Senior Analyst