While this morning’s nonfarm payroll data was a continuation of a steady multi-month growth trend, the market remains focused on the magnitude of the absolute number and the read through to prospective Fed policy adjustment. Given the unremarkable, +148K MoM change and the sequential softening in the rolling 3M/6M averages, a Taper delay is increasingly likely.

The absolute NFP numbers have been trending lower since 1Q13 while, on a rate of change basis, the YoY growth in total payrolls has been stable-to-higher over that same period – a dynamic largely stemming from the existent seasonal distortion in the data.

September reflected this same dynamic as total nonfarm payrolls were 45K lower than in August (revised) and the 3M rolling average fell -8K sequentially while YoY growth in payrolls ticked marginally higher.

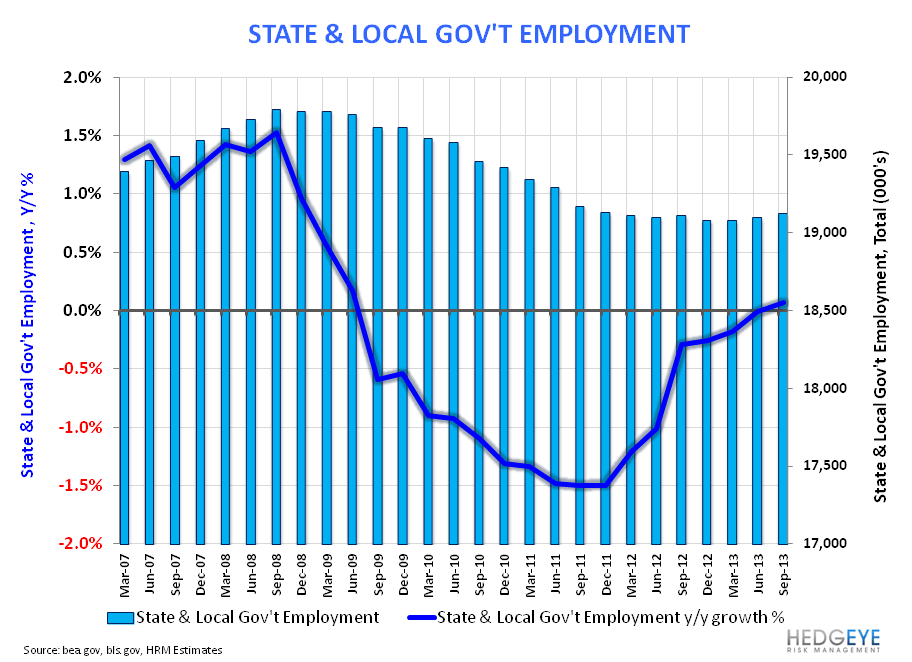

Elsewhere in the report, the unemployment rate declined to 7.2% on a static participation rate, part-time employment declined -594K MoM, State & local government employment showed positive growth for a 3rd consecutive month, and the U-6 Unemployment Rate and level of LongTerm Unemployed both continued to decline.

On balance, September was another month of middling employment growth with small, ongoing under-the-hood improvements. All-in, the preponderance of data is unlikely to get the Fed to move in the near term.

We expect seasonality to drive strengthening headline improvement in the employment data over the next 6 months with peak positive impact (again) occurring in March. Incidentally, prevailing expectations are shifting towards March as the likeliest timeline for Tapering – at which point Yellen should be fully confirmed at the helm of the Fed, Fiscal Policy uncertainty should (hopefully) be rearview, and the domestic marco data will, optically, be at peak strength.

Below is a summary review of the September Employment data along with a visual re-highlight (see: Initial Claims: "Tis the Season) of how seasonality has manifest in the macro data, expectations, and market prices over the last 4 years.

NFP: Net Non-Farm payrolls gained sequentially coming in at +148K – holding flat on a YoY growth basis at +1.66% while the 2Y average decelerated 3bps to 1.64%.

NFP Revision: The net two month revision was +9K with July revised lower from +104K to +89K and August revised higher from +169K to +193K.

Household Survey: The net employment gain as measured by the Household Survey was positive at +133K vs. -115K in August

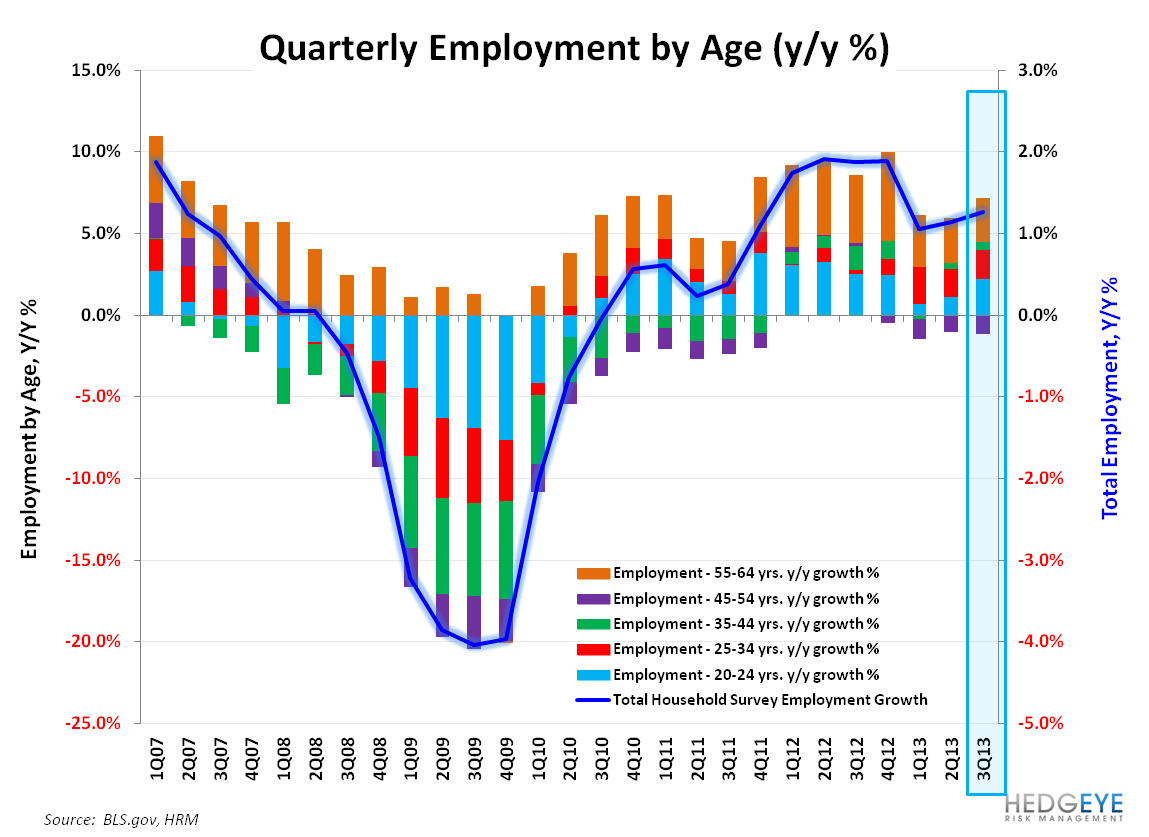

Employment by Age: Employment growth held positive but decelerated across all age cohorts except for 45-54 year olds, where payrolls remain mired in negative growth.

Unemployment Rate: The Unemployment Rate dropped to 7.2% from 7.3% as the total labor force increased +73K alongside a -61K decrease in Total Unemployed and +133K increase in Total Employed.

Labor Force Participation: A positive +209K change in the working age population alongside a +73K net change in the labor force pushed the Labor Force Participation Rate down to 63.19% from 63.22%.

Part-time/Temp Employment: Part-time employment declined by -594K (2M chg = -828K) while Temp employment gained +20K, registering its 12th consecutive month of net gains.

Industry Employment: Leisure/Hospitality and Finance were the lone losers with employment declining -13K and -2K, respectively in September.. Manufacturing gained jobs for a second straight month while Trade/Transportation and Construction posted their largest gains in 10 and 21 months, respectively.

State & Local Government Employment: Net positive change of +28K in September and a third consecutive month of positive YoY growth.

Ave Weekly Hours for Private Employees: Hours held flat at 34.5 MoM and YoY.

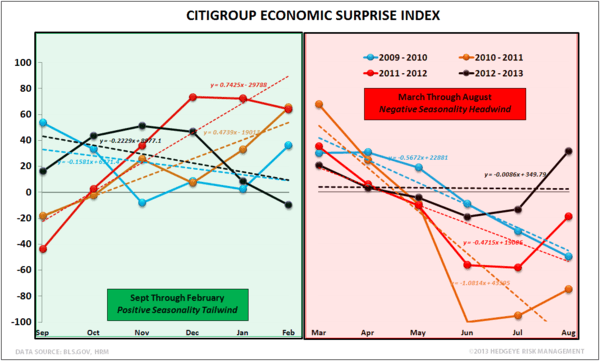

Seasonality Reminder: The September Trough

Positive Seasonal impacts build from September through March then reverse to a headwind that builds over the April to September timeframe. The seasonality impacts have been pervasive across the reported domestic macro data, sentiment, and market prices. From here, seasonality should manifest via strengthening improvement in the employment data through 1Q14.

Christian B. Drake

Senior Analyst