This note was originally published at 8am on October 08, 2013 for Hedgeye subscribers.

“You know, men do nearly all die laughing”

-T.E. Lawrence

As a young enlightened man in the field of war in the Middle East, that’s what T.E. Lawrence wrote to his Mom in 1916. At the time, he was also tasked with writing a weekly letter to the “Mother” (Britain’s War Office) of his homeland. Not surprisingly, this is when he started to “incense his military superiors” with on-the-ground truths (Lawrence in Arabia, pg 125).

“We edit a daily newspaper, absolutely uncensored, for the edification of twenty-eight generals; the circulation increases automatically as they invent new generals. This paper is my only joy. Once can give the Turkish point of view of the proceedings of admirals one dislikes, and I rub it in my capacity as editor-in-chief.” (pg 125)

Ah, the power of the pen. You either have it, or you do not. For an amateur writer like me, I get that my moments are fleeting. But, especially when attacking the tyranny of government spin, I feel as liberated as a man who believes in truth and freedom can feel. That’s why I do this at the top of every risk management morning - to feel free.

Back to the Global Macro Grind…

This is not a “free-market.” At least not in its purest definition. At any given moment of the trading day, the government can announce that it is officially saving us from itself. For that, I’ll be damned if I give thanks and praise.

Can money buy your freedom? What if the purchasing power of that “money” is being burned at the stake? What if your money is borrowed from the future of your grandchildren?

These aren’t new questions this morning. Montaigne started asking these questions in 1571 with “Essais” and Shakespeare personified the money/power/freedom conundrum with the Merchant of Venice too.

Can the world’s reserve currency (US Dollar) hold its long-term TAIL risk line of $79.21 support?

It’s still the #1 question in my notebook this morning. And I suspect it will be for some time to come. If you ask Gold, the answer is maybe. If you ask Bernanke, Obama, and Boehner, it’s no.

In addition to the US Dollar’s TAIL risk line imposed upon us by central planners, here are some critical US TREND lines to consider:

- US Treasury 10yr Yield = 2.58% TREND support

- US Equities (SP500) = 1663 TREND support

- US Equity Volatility (VIX) = 18.98 TREND support

That last one is what’s going to drive the other two. For all of 2013 I’ve been Bearish on Fear (VIX). As of the last 2 weeks, that’s changed. I am as afraid of US government intervention in our markets and economies as the VIX has become.

Yesterday’s move on the front-month of fear (VIX) was telling – follow Mr. Market’s flow:

- US Equities had a big newsy down-open in the pre-market built on the false media message that the US could “default”

- US Bonds and Credit Default Swaps didn’t care about all of the “default” fear-mongering; stocks acknowledge the same

- US Equities eventually lifted off the lows and were only down -0.3% by lunchtime

Then …

- As the lunch-time lull passed, US Equity market players started to realize that this correction is not just about “default” noise

- Almost everything that’s been killing it YTD (Growth Stocks) started to roll over in the early afternoon

- Financials (XLF), Consumer Discretionary (XLY), and Small Caps (IWM) all ended up closing down -1.2-1.3% by end of day

And all this happened as US Equity Volatility (VIX) broke out above the @Hedgeye TREND line (18.98) for the 1st time since June. Our process would suggest that there was absolutely no irony in that.

I won’t re-hash the Growth “Style Factors” that I outlined in yesterday’s Early Look again, but the risk management point to embrace was a very simple one. As a market expectation, #GrowthAccelerating has plenty of downside.

The US Government is not going to default on its debt, but it may very well slow growth.

Put another way, the longer that both the fiscal and monetary policy sides of the US House lean on:

A) Down Dollar

B) Falling US Interest Rates

The less likely it is that the US economic cycle will be allowed to occur.

Policies to Inflate (devaluing the Dollar) don’t create economic growth; they perpetuate inflation. Under our #StrongDollar + #RatesRising scenario (that may have died 2 weeks ago), inflation is not an issue. Now it is. Mother, be forewarned.

Our immediate-term Risk Ranges are now as follows (we do all 12 Global Macro ranges in our Daily Trading Range product):

UST 10yr Yield 2.60-2.68%

SPX 1671-1685

VIX 16.23-20.15

USD 79.67-80.71

Euro 1.34-1.36

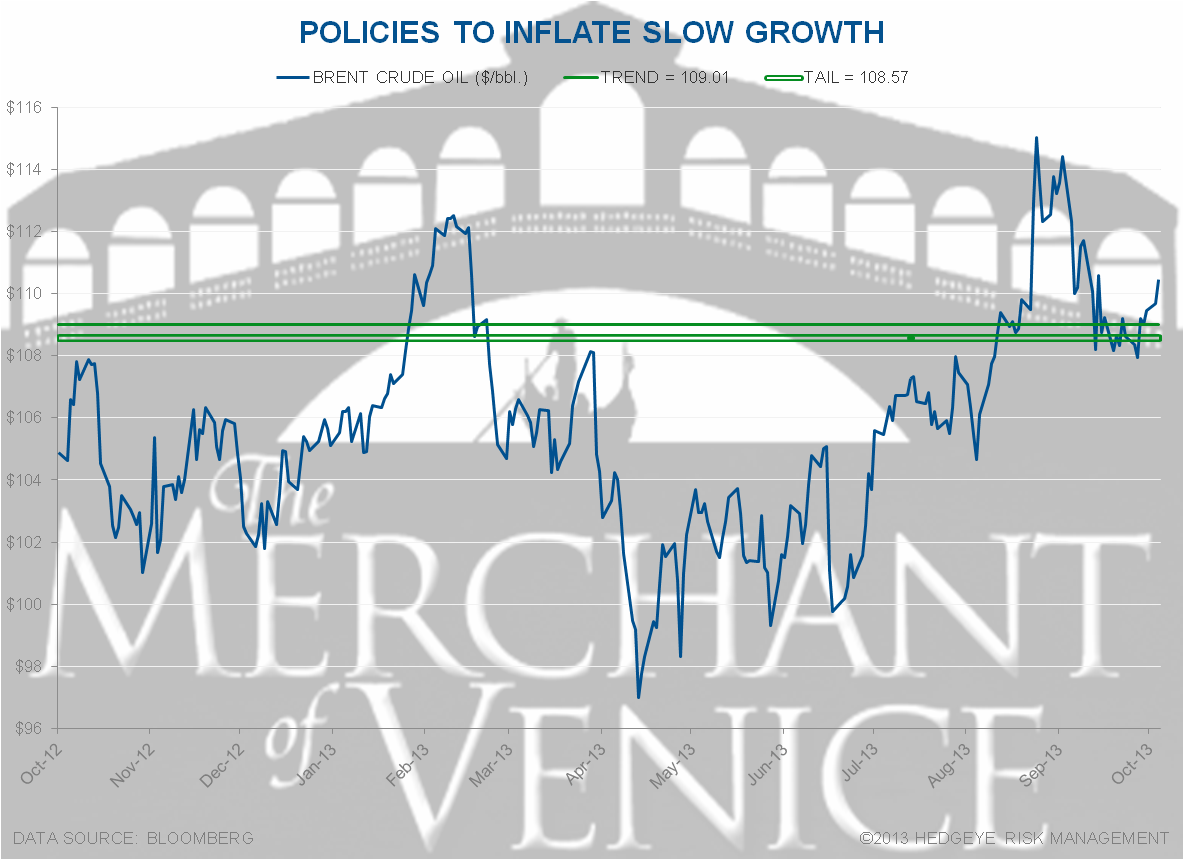

Brent 107.97-109.99

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer