We continue to believe EAT is one of the best managed companies in the restaurant space. Following the earnings report on 10/23, we will be hosting a call with the CFO, Guy Constant, on Friday, October 25th at 12pm.

We believe Brinker’s macro commentary from last quarter still applies. This is a very difficult operating environment for many restaurant companies and we expect to see slightly diminished margins given current sales trends. Looking back to 4Q:

- EAT continued to see a fairly lethargic category and the macroeconomic environment was not as strong as they had expected.

- The restaurant industry was not recovering as quickly as they had expected.

- In 4Q, the company was negatively affected by the deep discounting of their peers.

- Management decided not to match this aggressive discounting and remained committed to their Plan to Win strategy.

- Company-owned same-restaurant sales were down slightly for the quarter.

In 1Q14, EAT’s Chili’s brand is up against its most difficult comparison of the year at +2.8%. In our opinion, the current Consensus Metrix estimate of -0.4% for Chili’s appears to be aggressive, as this would represent a 40 bps acceleration to +1.2% in the two-year trend. Given what we know about current industry trends, EAT is unlikely to significantly beat sales estimates. In 4Q12, Chili’s company-owned same-restaurant sales and traffic were down -0.6% and -2.1%, respectively. Depending on where same-restaurant end up for 1Q14, management may need to address the current full-year guidance of 1-1.2% same-restaurant sales growth.

During the quarter, the company decided it will roll out tabletop tablets to all U.S. company-owned restaurants by the middle of next year. Franchisees have been given the option to include the devices in their locations. These devices are all-encompassing, as they can take menu orders, accept credit cards, let customers play games and more. In our opinion, this should enhance the customer experience at a manageable cost, as the installation costs are minute compared to the returns they will generate. We view this announcement as a positive, and believe Brinker is well-positioned, particularly compared to other casual dining chains, to take advantage of a changing consumer landscape. However, we do not expect to see the tabletop rollout have a material impact on sales until the second half of next year.

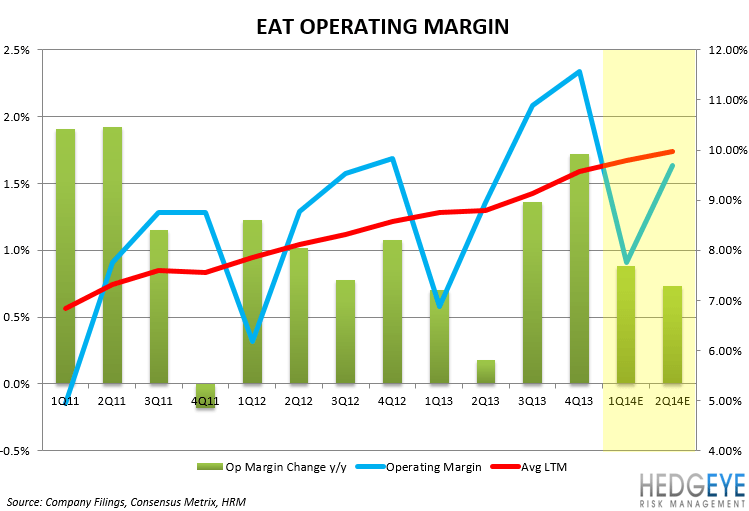

Looking past the near-term sales pressure, the company business model remains in good shape. In our opinion, food costs is one segment of the P&L that could come in better than expected. Guidance is for this line to improve in 1Q14. Consensus Metrix estimates indicate the street is looking for a 20 bps improvement in the quarter, which we believe may be too conservative. The company will also continue to benefit from new operating initiatives, which will result in continued labor and efficiency gains, specifically in the first half of FY14. We are expecting restaurant level margins to improve 80 bps y/y in 1Q14.

The bottom line is, we aren’t expecting to learn anything shockingly new when EAT reports on 10/23 and we do not know how the stock will react. Short interest has been coming down over the past month and the sell-side has been becoming more bearish of late. In our view, the recent incremental bearish bias toward EAT is simply a byproduct of the current industry conditions as opposed to anything company specific. The excessive discounting from DRI is hurting everyone in the industry, but particularly EAT. With that being said, Brinker would be one of the biggest beneficiaries from our dismantling Darden thesis, if it played out.

Despite the difficult operating environment, EAT remains financially robust. In 4Q13, the company passed the $1 billion share repurchase mark since its fiscal 1Q10. Over the same period, management reduced the share base by nearly 33%. Looking out over the next 12 twelve months, we expect EAT to repurchase another $250 million in stock, effectively reducing the share base by another 7%.

Howard Penney

Managing Director