CCL looks washed out (as are the bathrooms on the Triumph, finally) while RCL may be the stock at risk.

This is indeed a pivot for us - we’ve been crapping on CCL all year. But with most of the issues flushed out, the stock may be bottoming out. In our latest pricing survey, Europe looks stable and with easy upcoming comps, CCL’s large European exposure should be an asset. Moreover, CCL is doing better than the competition in Alaska and while the Caribbean outlook is still somewhat cloudy, our pricing survey did not indicate any further deterioration for early 2014 itineraries. Could we be early? It’s happened before but the hedge of RCL on the other side might be the solution, for those so inclined to a pair trade.

Our pricing survey actually presented a more uncertain 2014 for RCL. Given RCL’s newfound position as the Cruise bellwether and recent stock appreciation to match, the risks look greater for that stock. RCL won’t feel the Europe tailwind (“Europe tailwind”? it’s no longer an oxymoron) to the extent of CCL. Regionally, RCL faces pressure in all of its markets – potentially from CCL’s aggressive marketing strategy. Pricing is way down in Alaska and Europe and RCL is overexposed to the Caribbean (highest since 2007) where visibility is the lowest. Sell-side sentiment seems the most bullish in over 2 years. While valuation is in-line with historical levels, RCL's earnings are at risk.

Here are some of the differentiating factors between CCL and RCL:

CCL HAS MORE EXPOSURE TO THE EUROPEAN TAILWIND

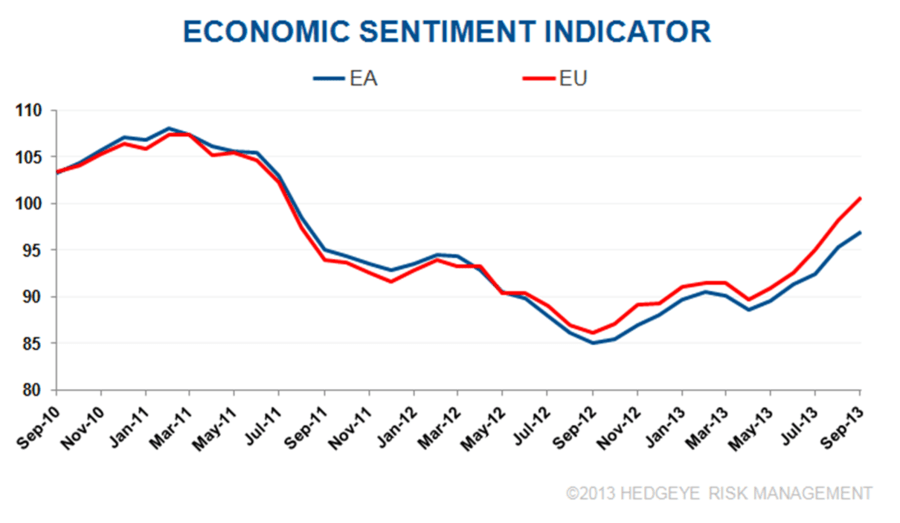

If the European economies and consumers continue to recover from the depths of a painful recession, Carnival benefits disproportionately given its outsized exposure to Europe and easier comps. Our macro team is seeing an improved risk climate in the region, which bodes well for Q4 and 2014. Please see Hedgeye Macro Themes Q4 2013 that presents their view that the environment is ripe for the European consumer – strong currency, growth accelerating and inflation decelerating. Our Cruise Pricing Survey corroborates the Hedgeye macro view. We estimate CCL, RCL have 30% and 22% of its itineraries in Europe for 2014, respectively.

The British Pound also looks bullish for the consumer. According to a recent TripAdvisor survey, UK consumers are likely to cut back on daily living expenses to protect their holiday budgets for 2014. Despite an economy that is still fragile and recovering, this could result in a higher travel budget for some UK consumers. Carnival’s P&O Cruises UK and Cunard, which accounts for roughly 10% of overall itineraries, could benefit from the UK rebound.

PRICING DIVERGENCE IN EUROPE/ALASKA

Our Cruise Pricing Survey is showing quite a divergence in pricing between RCL and CCL brands in Europe and Alaska for 2014. In Europe, RCL is discounting heavily while most of CCL’s brands are maintaining price. The discrepancy is more stark in Alaska. One reason why RCL may be lowering price in Europe could be due to tougher 2014 comps; we believe RCL’s 2H 2013 pricing was strong.

RCL YIELD RISK

One of the primary reasons why many analysts have been so positive on RCL is that they believe the company can achieve +2.5% to 3.0% net constant currency yield for 2014 and beyond. We believe that Street forecast is too rosy based on early trends from our pricing survey; +1.0% to +2.0% yield growth is probably more reasonable guidance for 2014 (we’re at +1.7% constant currency net yield). While it’s true that RCL may get a yield bump in Q4 2014 with the delivery of Quantum of the Seas, the Caribbean is very crowded market and cannibalization remains a risk.

For Carnival, 1H 2014 yield guidance would suggest the lowest net yields seen since 2004. Unless there is another ship catastrophe, the bottom may finally be in. We are forecasting +1.5% yield for 2014. We believe F1Q yields will be the worst, with sequential improvement each subsequent quarter.

CCL ESTIMATES FINALLY IN LINE?

We think so. When Carnival Triumph became kaput in February, the sell-side tried to reassure investors that this was a ‘normal’ ship incident that would only have a temporary adverse effect on the business. We thought otherwise as we noted in "CHART DU JOUR: CCL: IT COULD GET SMELLIER” (02/14/13) given our concerns of the deterioration of the Carnival brand and that the incident was widely publicized and US-based. Since then, Carnival has lowered guidance three times and boosted capex to shape-up their ships. This past quarter, we thought some of the CCL bulls were still too early as we noted in "CCL: IS NOW REALLY THE TIME FOR A VALUATION UPGRADE? (08/15/13).

With Wall Street finally pessimistic on CCL (see the Sentiment section below), we think FY2014 estimates are finally achievable and a meet may be good enough for the stock to work. For FY 2014 EPS, we’re in-line with the Street for CCL at $1.64 and below the Street by 6% for RCL at $2.88.

SENTIMENT DIVERGENCE

Sell-side sentiment on CCL appears to be at its lowest since July 2010 as 15% of the analysts have stamped a sell rating on the stock, stemming from a flurry of downgrades following 2014 guidance. On the other hand, analysts love RCL – the highest % of buy ratings since October 2011. The upside potential implied by their average price targets has narrowed between the two names – CCL +7% and RCL +9%.

CONCLUSION

Being contrarian for contrarian sake is not our goal, but when that same contrarian call is backed by catalysts, it becomes compelling. The RCL/CCL sentiment divergence is as wide as we’ve seen it yet CCL is the one with the better fundamentals, on the margin. CCL comps are easier and pricing looks more stable than for RCL, particularly in Europe and Alaska. Europe on the margin is a tailwind and a bigger one for CCL. Estimates look reasonable – finally – for CCL while we’re below the Street for RCL. 2013’s big cruise stock performance divergence could reverse as we move into 2014.