First, we'd like to say that we do not believe management has adequately recognized the seriousness of the situation they find themselves in. Therefore, it goes without saying that, in our opinion, earnings estimates are too high for the remainder of 2013 and 2014.

We’ve recently spoken to an unnamed industry insider in order to clarify our understanding of the cycle that many companies in the restaurant industry tend to go through. Typically, when a concept gets in trouble, the management team’s decision-making process tends to follow a certain pattern:

- Overconfidence – The concept loses its value proposition when management raises prices too aggressively or lowers the quality of food.

- Stage 1 Denial – Consumers catch on and begin to frequent the concept less often. Traffic begins to decline and management usually begins to blame the weather or another external event.

- Stage 2 Denial – In an effort to avoid the inevitable and appease the street, management begins to accelerate growth through the form of new unit acceleration or the acquisition of new brands. Normally, the core business continues to deteriorate alongside a decline in ROIIC (return on incremental invested capital).

- Stage 1 Panic – Analysts begin to catch on and management responds by slowing new unit growth, although often not by enough. The core business continues to decline, as senior management begins to replace the operating team. Simultaneously, the search for a new advertising agency begins.

- Stage 2 Panic – Now it really begins to get ugly, as management sacrifices margins to increase customer counts by implementing a deep discounting strategy. It then becomes clear that major changes need to be made across the enterprise.

- The Healing Process – Management decides to stop growth and attack the middle of the P&L.

Starbucks, Brinker, and McDonald’s are all companies that have successfully worked their way through this cycle, as management from their respective companies aggressively cut CapEx and began to grow it very conservatively for the next few years. By slowing growth and attacking the middle of the P&L, EBITDA began to consistently increase in each situation. In our view, SBUX and EAT are currently two of the best managed companies in the restaurant space. DRI, on the other hand, is a company which, similar to PNRA, is currently going through this cycle (Stage 2 Panic). But, unlike DRI, PNRA is in the early stages.

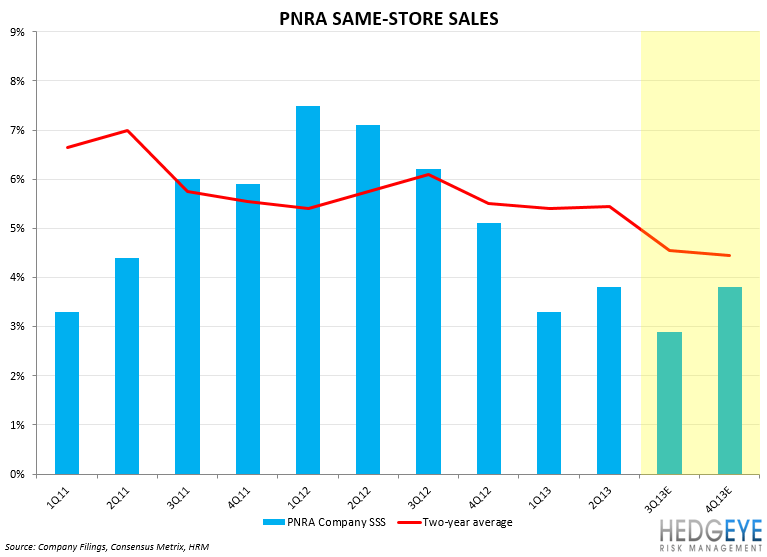

While 2Q was a disaster for PNRA and a number of analysts have downgraded the stock recently, we are sticking with our short thesis. We believe the stock will continue to underperform until the healing process begins. Last quarter, management warned investors that 2013 would be more volatile than expected and that this trend should continue for the next 3-4 quarters. Looking past 3Q13, we believe the challenges the company faces will extend into 2014. How far into 2014 these challenges will persist depends on how management reacts to them.

On the 2Q13 earnings call, management lowered the 2013 outlook to properly reflect the operational improvements they are making. Management’s guidance for 3Q13 EPS was between $1.32-1.36, and the street is coming in at $1.35. Given the likelihood of a top-line miss, we believe the street is giving the company the benefit of the doubt, which could lead to further disappointment when the company reports on Tuesday.

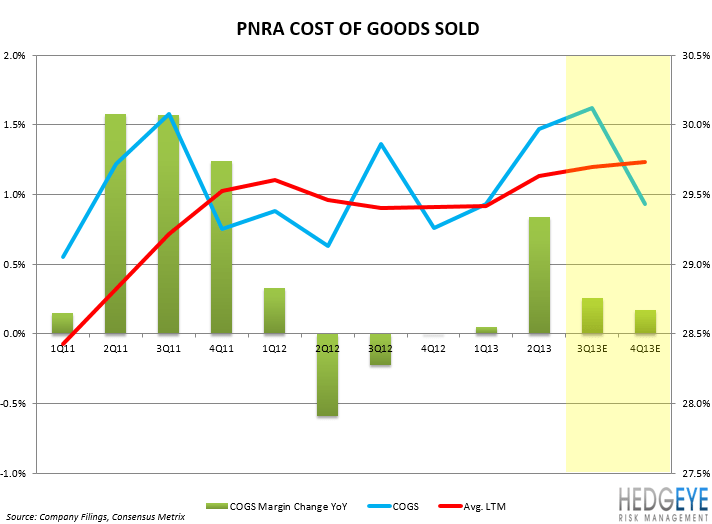

With the company trying to drive incremental throughput, we believe that an EPS miss could come from incremental labor costs. Current consensus expectations are for labor costs to be up 11 bps y/y, which is, in our opinion, generous. Given sluggish sales trends, limited pricing power, and the need for incremental investments, we believe labor costs will be higher than the street is expecting.

Looking out to 4Q, it is difficult to tell whether PNRA will be able to hit the numbers, particularly given the company will have an additional week this year. The street is coming in at $2.09, or 19% EPS growth, on 19% revenue growth, while management has guided to $2.05-2.11. Given the early reads on October sales trends, we suspect it will be challenging for PNRA to accelerate SSS in 4Q.

Admittedly, the biggest risk to being short PNRA is that it appears to be a consensus short. The sell-side has turned on the company. Only 57% of analysts have PNRA rated a Buy and short interest in the stock is at 6.3% of the float, which is one of the highest in the QSR space.

Howard Penney

Managing Director