One that doesn’t appreciate high growth, high cash flow, and a newfound propensity to distribute cash to shareholders.

LVS posted a great quarter. We’re very happy with the Macau fundamentals, the stability in Singapore, and potential expansion of gaming in Asia. Within that favorable industry construct, LVS is nailing it operationally. The LVS properties yielded up their Mass tables impressively which contributed to higher margins (see the charts in the Quarterly Review section below). And they’re not done yet. Table yields have a long way to go and with the company’s extensive room base, cross marketing initiatives, and premium Mass push, LVS is likely to continue share growth in the rapidly growing Macau market. On the margin and from a stock perspective, we’re probably most excited about LVS’s broadening appeal, growth and dividend investors alike.

LVS announced yet another dividend hike – this time a 42% increase, pulling the yield up to nearly 3% and $300 million in stock buybacks during the quarter. Meanwhile, leverage remains too low around 1x. With over $3.6 million in free cash flow next year, LVS could up its yield to a whopping 6% without levering up. And that cash flow will continue to grow with the opening of The Parisian in late 2015 and continued same-store EBITDA growth. We have no feel for whether LVS will pay out a special dividend – they could easily do it – but we would prefer continued buybacks and regular dividend hikes.

Valuation is the main push back but with LVS’s combination of growth and cash flow, should we really be concerned with an EV/EBITDA multiple of 13.x (excludes debt associated with Parisian)? Certainly not, especially when considering that a good portion of LVS’s profits are not taxed (approximately 55%), a benefit that isn’t captured by EV/EBITDA. Future high ROI projects in Macau (The Parisian), potential developments in Japan and South Korea are also not captured. LVS should continue to garner more widespread investor appeal with its emerging cash distribution focus (dividend investors welcome) along with the existing growth investors. We would argue that valuation concerns are of little relevance.

Q3 REVIEW

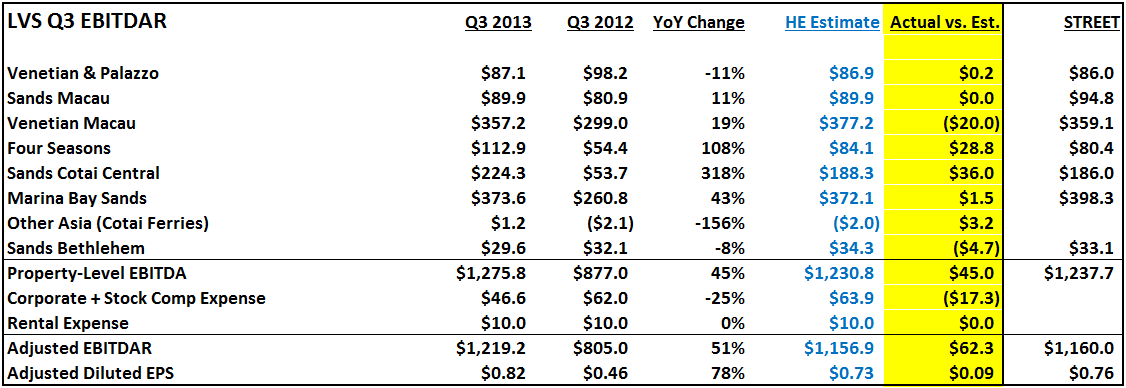

Per usual, we don’t want to recap the entire quarter. As can be seen in the chart below, LVS beat us quite handily.

Our focus is on table yields, specifically at Sands Cotai Central and Four Seasons. These are clearly the two properties with the most upside. Operationally, LVS is pushing the underpenetrated (for them) Premium Mass segment. Both Sands Cotai (who will have more mass tables coming in Q2 2014) and Four Seasons made significant progress as can be seen in the following table yield chart.

Table yields should continue to move higher for LVS and drive market share gains in the coming months (probably through year end 2014).