"Get Busy Living or Get Busy Dying"

-Morgan Freeman, Shawshank Redemption

Earlier this week, I raced a 95 year old lady down the Merritt Parkway on my way home from work.

Well, kinda.

To review: while driving north from our new HQ in Stamford, I watched in my rearview mirror as a navy blue Mustang darted back & forth between lanes before pulling up beside me, then speeding ahead.

After racing to catch-up for a confirmatory, second look…90 is, apparently, the new 25.

The age was undeniable, but there were no coke bottle glasses, no cautious, granny-fied 3 o’clock- 9 o’clock hand positioning, no squinty eyed lean forward, no Buick or Oldsmobile.

Just a sharp gaze and tangible life energy.

The experience was a pleasant surprise and a welcomed contrast to the latest, consuming iteration of beltway brinksmanship – which, unsurprisingly, lacked both pleasantness and originality.

Back to the Global Macro Grind…..

I don’t know granny’s life recipe for sustained physiological alacrity – but the ‘pleasant surprise’ of her apparent vitality dovetails nicely with one of our top 3 Macro Investment themes for 4Q: #GetActive

Without giving away the full, institutional macro alpha thunder, our call for an increase in active investment management is predicated on a few key points:

1. Big Government Intervention: Our fiscal policy creation process remains a circus and the new golden boy in the monetary policy arsenal – the “communication tool” – remains in beta testing and breeding decidedly more market uncertainty than price stability at present. Collectively, we expect policy intervention to continue to perpetuate Market/Currency/Economic Volatility. Volatility breeds both opportunity and a heightened probability for an expedited drawdown in equities and …

2. Active Management outperforms in down markets: Historically, on average, the HFRX Equity Hedge index outperforms the SPX in down markets and that outperformance increases as the magnitude of negative monthly S&P500 performance increases. At extremes of negative market performance, the HRFX has outperformed by ~800bps on a monthly basis. Hedge funds apparently hedge after all.

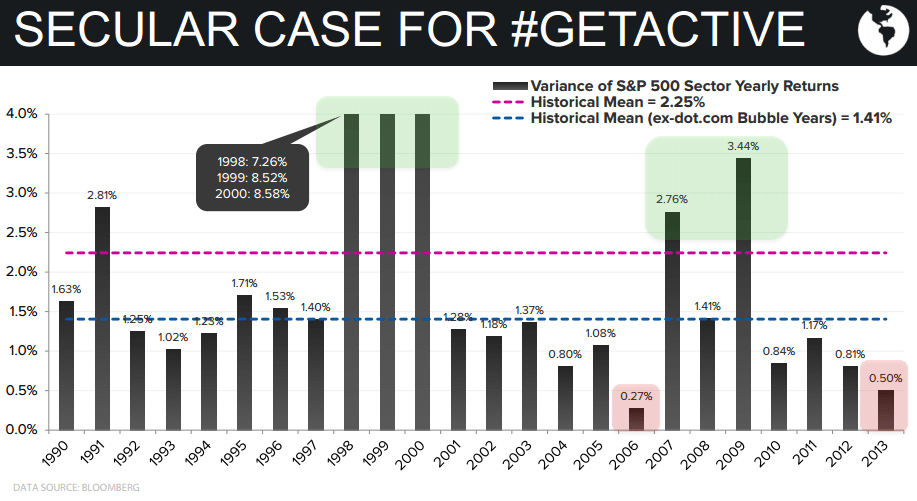

3. Sector Picking will Matter: As the Chart of the Day below illustrates, the variance in sector performance this year is near a historic low Put differently, it hasn’t really mattered what sector you bought – beta has been the new alpha and simply buying the market was the best allocation decision. Over the intermediate term, a mean reverting breakout in the variance of sector returns is almost a guarantee. Consider the performance delta between Financials and Utilities in the quasi-analogous post-1994 period, after Greenspan began his rate raising campaign. Financials returned 50%, 32%, and 45% in 1995, 1996, and 1997 respectively. Utilities returned 25%, 0%, and 18% over that same period. A 3Y CAGR of 42% for Financials vs 14% for Utes.

In truth, #GettingActive is really just an investment euphemism for Trading.

Trading generally gets a bad rap because it doesn’t fit the canonical ‘stocks for the long-term’ dictum, it doesn’t market well and, well, it’s hard – the recent multi-year trend in collective hedge fund benchmark underperformance hasn’t been a siren song for incremental actively managed AUM either.

Keith has actively managed market risk in the Hedgeye portfolio for 5+ years, actively manages the Hedgeye HFT (High Frequency Tweet) machine and is probably more” active” than constrained in opining on markets, policy and policy makers.

To the latter point, sometimes I think the punditry of the Early Look prose occasionally belies the reality of our risk managed positioning.

For instance, while we were highlighting an increased likelihood for a policy induced deceleration in domestic growth back on Oct 9th/10th, at the same time, we were taking up both our gross and net long positioning into the back end of the 4% market correction.

From a process perspective, our conviction level rises and we typically get louder about an idea when both the research (fundamental) view and the quantitative risk management signal are both in agreement.

But what if there is no fundamental data?

The gov’t shutdown the last two weeks has served as an illustrative example of how our risk management process works in practice – primarily because there was no incremental fundamental data to inform our marginal macro view, leaving the risk management signal as our principal signaling mechanism for driving portfolio decisions.

Contrasting yesterday’s price signals and subsequent allocation decisions with those made a week ago exemplifies the process.

What were the market and price signal dynamics back on Oct 10th and why did we buy the dip:

- $USD – V-bottomed off its long-term tail line of support at 79.21

- VIX – was breaching its TREND support level of 18.98 on the downside

- SPX – recaptured TREND support at 1663

- 10Y Treasury – Held TREND support of 2.58%

- U.S. Stocks moving towards immediate term oversold, down for 11 of the prior 15 days

With all the price signals in agreement, the highest probability swing was to get longer and play for the 24 handles of immediate term upside.

Yesterday’s price signals were very similar:

- 10Y Treasury – 10Y was back to flirting with a TREND breakdown through 2.58%

- $USD – The dollar was moving back towards testing TAIL support at 79.21.

Down Rates + Down Dollar + Rising Policy Uncertainty is not a factor setup we want to be long of over the intermediate term, but we kept the portfolio unchanged at 6 Longs, 3 short into the close. Why?

- SPX – higher highs are bullish and equities were not signaling immediate term overbought

- VIX – Debt Default fear remained for sale with the VIX continuing in free fall

- Squeezage – with hedge fund short positions as YTD highs there’s room to let the squeeze rally breath a bit.

- Hilsenrath’s mid-afternoon proclamation that Oct-Taper is officially a no-go & Bernanke/Yellen risk remains acute juices the immediate term downside risk for both the dollar and interest rates.

So, we didn’t buy the rip or tighten up net exposure.

What will we do today? I don’t know – and that’s largely the point. As always, we’ll let the market signal tell us which way to lean.

Does timing matter? Implicit in allocations to active strategies is a belief that it does.

As Keith queried on twitter yesterday afternoon:

“If timing didn't matter, why are you watching Twitter right now?”

Similarly, are markets efficient or irrational and reflexive?

Fama won the Nobel prize for “proving” the former. At the same time, Shiller won for proving the latter. Seems about right.

Activity/Variety is both the spice of life and nature’s most potent cerebral exfoliant.

Take a different route to work in the morning, eat dinner with your left hand, simplify a few radical expressions, invest some incremental capital in the growth inflection happening across the pond, turn down CNBC and turn on #tweetshow today at 3pm.

Switch it up, Get Busy.

Our immediate-term Risk Ranges are now:

UST 10yr Yield 2.55-2.67%

SPX 1

VIX 12.61-15.24

USD 79.21-80.31

Euro 1.35-1.37

Pound 1.60-1.62

Enjoy the Weekend.

Christian B. Drake

Senior Analyst