Summary

Investors do not seem very negative on the outlook for CAT’s 3Q earnings for an odd reason. They tend to think that everyone else thinks that CAT will miss, limiting the relevance. Investors are also looking for an announcement on structural cost actions at Resource Industries, which may cloud the 2H outlook. Our view is that CAT has an end-market demand problem, not a cost problem.

CAT is also expected to issue preliminary sales and revenue guidance for 2014. Many expect that it will be the Industrials guide of the quarter. We think not – few analysts take guidance from CAT seriously anymore. Remember “steady as she goes” for the 2013 outlook given in 3Q 2012? Sales and revenues were supposed to be “roughly the same as 2012, in a band of about plus-or-minus 5%.” Recall that 1Q 2013 sales and revenue were actually down 17.3%. Following some short-term reaction, the market is likely to take a 2014 outlook with an excavator full of salt.

We generally do not bet on quarters – it is a tough game. A change in assumptions for warranty or accounts receivable allowances could leave even the best estimate off target. A simultaneously announced buyback or acquisition could render the reported results old news before they are even read. That said, there are a number of reasons why we expect weaker results this quarter.

While we will be ‘surprised’ if results do not disappoint, we are not ‘in’ CAT for this quarter’s results. Rather we are focused on the long-term down-cycle in resources-related capital spending. In the long run, resources-related capital spending requires rising commodity prices to remain far above maintenance-type levels. Currently, resource-related capital spending is well above the levels needed to support long-term demand growth.

Key Items

CAT Inventories: CAT has guided flat company level inventories for 2H 2013, meaning that inventory levels at year end should be roughly the same as at the end of 2Q 2013, as we understand it. However, in the third quarter “inventory could come down some as we have many of our Northern Hemisphere facilities take vacation shutdowns during the months of July and August.” The company level inventory headwind should have continued into 3Q 2013, but consensus doesn’t seem to reflect it. Dealer inventories are also expected to decline through 2H 2013.

Can CAT Get To $6.50? That inventory outlook intersects poorly with the implied margin in current guidance. Here is what we wrote on 8/9/2013 - our view is unchanged:

To hit guidance, CAT’s margins in 2H would need to improve ~30% vs. 1H with NEGATIVE MIX and NEGATIVE PRICING in Construction Industries and Resource Industries. Sure, that might happen – and 795F Trucks might fly. As we have written repeatedly – CAT is letting us down easy (gradually) and we have a tough time getting to $6.00 in 2013 EPS. This is just a rough sketch of guidance - not what we expect, which we published here.

Current consensus has margins at about 11.5% in the back half of the year, which would also represent a substantial and unlikely improvement in profitability from 1H. Given the expectation of continued inventory reduction in 3Q, we are not sure why consensus expects margins to expand. A guide down seems quite likely.

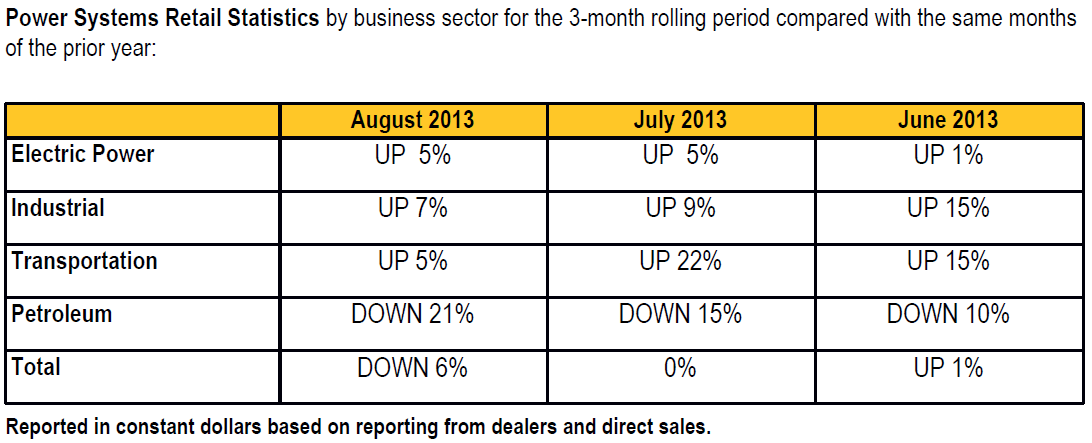

Not Just Resource Industries: CAT management admonished us not to hyper focus on mining capital spending, shifting investor attention instead to Power Systems. That may not be a great plan. We have long expected the resource-related capital equipment portions of Power Systems to also experience meaningful pressure. The most recent dealer statistics (below) show declining sales in Power Systems. That seems consistent with our broader definition of resource-related capital spending. It is also not a great set-up for 2014 sales and margins.

Construction Industries: In a noticeable omission, CAT does not fully discuss the >500 basis point drop in Construction Industries margin in 2Q 2013 YoY. It apparently relates to dealer inventory reductions, too, but that explanation does not fit the ‘it’s just a mining equipment demand drop’ narrative. CAT’s construction equipment division participates in an intensively competitive business, but we are a bit surprised by the recent weakness. As we understand it, lower capacity utilization in Resource Industries impacts the other divisions as well, given shared platforms, and that is a very hard problem to isolate or correct.

3Q and 4Q Expectations: Forecasting quarterly earnings for CAT is challenging, in no small part because we do not know how much revenue will come out of the backlog. Last quarter, CAT emphasized inventory headwinds, but not the draw on backlog and the likely favorable pricing in it.

- We expect charges in 3Q for the structural capacity reductions at Resource Industries. We also think a goodwill impairment charge is likely in 4Q for BUCY goodwill, as impairment testing should come at year-end.

- Excluding those factors, we would expect a 3Q result in the neighborhood of $1.30-$1.50 vs. consensus of $1.67. We could be wrong for several reasons beyond backlog, including currency and cost controls, but that is what we get. Once a company gets into identifying restructuring charges, as CAT seems likely to do this quarter, lots of interesting items can be called special. That said, we think current guidance is a long-shot and expect CAT to struggle to earn $6.00 this year.

- Instead of a buyback, we expect a miss to be paired off with a cost reduction plan targeted at Resource Industries. Of course, the cost impact of low volume at Resource Industries is not easily isolated, so that is where we will be interested to see some detail. We could obviously be wrong in this expectation.

- We expect comments about 2014 to be positive and focus on the eventual end of dealer inventory draw downs. We note that JOY and Sandvik have seen large mining order and revenue drops without a dealer network.

Other Indicators: While we do not rely on these sort of tea leaves, secondary indicators for CAT are do not suggest an approaching inflection point:

- Insiders Selling: In the last couple of years, insiders have only bought 2,000 shares in the open market while selling hundreds of thousands. Selling may have slowed down in recent months, but we do not see the open market purchases that might accompany an inflection for CAT.

- Sell Side Estimate Revision Trends: Since the first week of October there have been a number of downward revisions to estimates. Quiet period or not, we all should have a sense of how this ‘revision’ process works.

We continue to see CAT as exposed to a significant, multi-year decline resources-related capital spending through both its Resource Industries and Power Systems segments. Investors appear to be hoping for a cost reduction plan capable of resolving a lack of demand/cyclical downturn problem. We continue to expect CAT shares to underperform through the down-cycle.