The Kinder Morgan Complex (KMI, KMP / KMR, and EPB) delivered modestly negative 3Q13 results and implied 4Q13 guidance after yesterday’s close. In our view, both MLPs have growth problems and significantly understated maintenance CapEx figures.

Below we provide some thoughts following the results; we’ll have additional color after the 10-Q’s are filed next week.

Short Kinder Morgan remains a Best Idea.

KMP

- Can KMP grow on a per unit basis? KMP’s 3Q13 DCF/unit fell 1% YoY to $1.27 (0.94x coverage). We don’t consider DCF overly useful because we believe that KMP’s sustaining CapEx is significantly understated. KMP’s net income/unit (before Certain Items), which we do find useful, came in at $0.51, down 11% from $0.57 in 3Q13. The delta between the drop in earnings relative to DCF is likely due to the CPNO acquisition. KMP closed on CPNO on 5/1/13, and CPNO’s maintenance CapEx is likely more understated than legacy KMP’s – the “Copano Case II Projections” published in CPNO’s 4/22/13 8-K lists maintenance CapEx of $20MM and adjusted EBITDA of $361MM for 2013 (maintenance CapEx = 5.5% of EBITDA). CPNO is an operationally-levered G&P that needs to build new infrastructure to keep throughput from declining wells flat; maintaining “capacity” is near irrelevant. Many MLP G&Ps have this problem; KMP inherited CPNO’s. In 3Q13, KMP’s total organic expansion CapEx was ~$875MM, while sustaining CapEx was $92MM. Over the TTM, KMP has invested more than $10B (acquisitions and CapEx), and KMP’s earnings and DCF per unit are down YoY. And this is a longer-term problem. KMP’s net income per unit was $0.54/unit back in 3Q08, higher than it was in 3Q13. Is KMP too big to grow? Is KMP’s cost of equity (IDR burden) too high? It seems that way to us…

- Where’s the Natural Gas segment growth? Is KMP’s natural gas segment growing? On a pro forma basis, natural gas transport volumes were down 5.7% YoY, sales volumes were up 1.0% YoY, and gathering volumes were up 1.4% YoY. Not impressive – especially when considering the wide gap between sustaining and expansion CapEx. Using the CPNO Case II projections (full-year 2013) and KMP’s 2013 budget, annual Natural Gas segment expansion CapEx is ~$1,560MM (ex. acquisitions) and maintenance CapEx is $139MM. On the conference call, we asked management to give us G&P maintenance and expansion CapEx, which they could not do. We find it hard to believe that KM does not have these figures, as it does break out EBDA for the midstream business (TX Intrastate + G&P) in its annual investor presentation. KMP’s midstream segment + a full-year of Copano would generate ~$1,200MM of annual EBDA, according to management’s projections. If these segments are growing, it is low, single-digit growth. What is run-rate CapEx for this business? How much total CapEx is needed to maintain unit volumes over the long-term? And how much of that CapEx is currently included in sustaining CapEx? It’s difficult to know with publicly-available data. But CPNO Case II calls for $672MM in expansion CapEx in 2013 on its own – so pro forma CapEx number could be $800MM - $1,000MM, but only a small fraction will be in sustaining CapEx. We believe that KMP’s G&P business – especially after the acquisition of CPNO – is another maintenance CapEx problem.

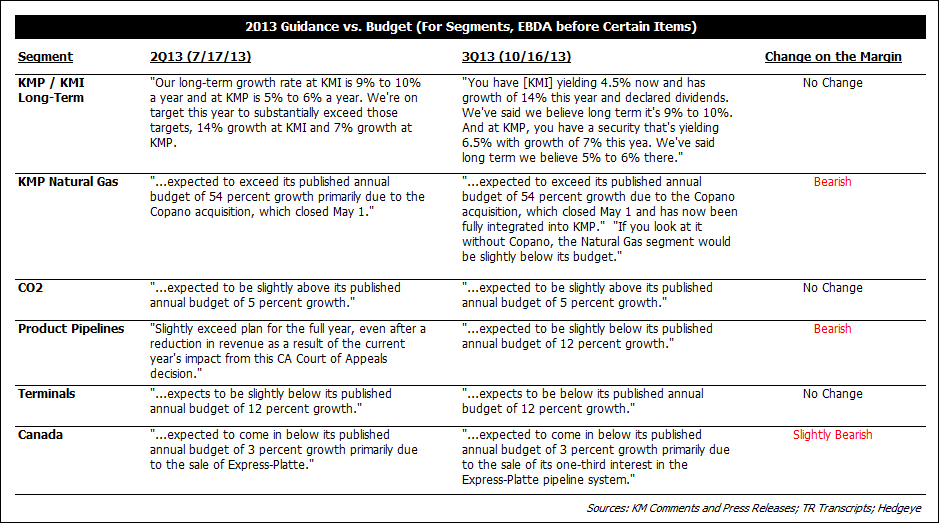

- Bearish tone to guidance…Kinder Morgan guided down its 2013 EBDA outlook for Product Pipelines (KMCC volumes cited), and was incrementally negative on KMP Natural Gas and Canada. Management noted that, “If you look at [the Natural Gas segment] without Copano, the Natural Gas segment would be slightly below its budget.” Not great news for KMP’s most important segment. The outlooks for CO2 and Terminals were in-line with prior guidance. No change to LT distribution / dividend growth rate guidance. See Table below:

- Questions remain on El Paso maintenance CapEx cuts. As management noted on its 9/18/13 investor call, the 2013 maintenance CapEx budget for the acquired El Paso subsidiaries is $132MM, down $222MM (-63%) from the $354MM that EP spent in 2011, which was in-line with the run-rate over the prior decade. Kinder Morgan again attempted to reconcile the drop with the general argument that an increase in O&M expense explains it; 2013 O&M expense for pipeline integrity is expected to be +$63MM and non-pipeline O&M expenses -$33MM, or +$30MM net. This doesn’t do it for us. First of all, on the prior call, KM spoke to FERC financials. Now, it is pointing us to the GAAP financials. The FERC financials show that transmission maintenance expenses (mains and non-mains) are down ~80% from 2011 (annualizing the 1H13 numbers). Second, let’s not lose sight of the big picture – Kinder Morgan cut more than $400MM of annual expenses and maintenance CapEx from these budgets, with only $161MM on the G&A line. Perhaps some of the maintenance CapEx found its way into the expansion CapEx budget (TGP pig launchers / receivers, for instance), but it’s difficult to know with publicly-available data. The important point is that, as Kinder Morgan said on its 9/18/13 call, “…everything that you do eventually gets into the rates you charge for your transportation services.”

- $285MM Goldsmith acquisition cost should be deducted from DCF. In June 2013, KMP CO2 acquired Goldsmith Landreth San Andres Unit in West Texas from Legado Resources for $285MM. This acquisition serves to replace declining production from SACROC and Yates. It makes no difference whether or not KMP invests organically or via acquisition to keep total oil production and reserves flat – the capital is needed to maintain the total cash flows, and it all should be deducted from DCF to acknowledge that fact (note: VNR, PVR, and NRP know this issue well).

- We find it funny that…The sub-title on KMP’s press release reads “Third Quarter DCF 22 Percent Higher Than 3Q 2013.” Let’s be clear – this is KMP’s absolute DCF number, not DCF/unit, which was down 1% YoY from $1.28/unit to $1.27/unit. Great marketing though…

KMI

- KMI 2013 dividend guidance flat…KMI is to declare dividends of “at least” $1.60/share in 2013. Similar guidance to prior comment on 7/17: “We remain on target to meet or exceed our goal of $1.60 declared dividends for full-year 2013.”

- KMI reloads the share / warrant repurchase program…KMI approves $250MM share / warrant repurchase; in addition to (but a smaller program than) the $350MM share / warrant repurchase approved in July 2013, of which $16MM of capacity remains.

- KMI dividend coverage = 1.00x...KMI is running tight dividend coverage, which could be a problem with growth issues at the MLPs, exposure to oil prices, natural gas contract rolls, and the 348MM warrant overhang. YTD coverage is 0.99x vs. 1.10x in the first 9 months of 2012.

EPB

- Lackluster quarter and outlook…EPB’s DCF/unit came in at $0.58 (0.89x coverage), down 18% YoY, and earnings/unit came in at $0.40, down 27% YoY. Lower revenues from SNG and WIC due to adverse rate cases, as wells as a higher IDR fee to KMI, weighed, and could not overcome the drop in sustaining CapEx (down 31% YoY) even as D&A moved marginally higher (up 7% YoY). Transport volumes were 7.3 Bbtu/d, down 9% YoY, largely due to cooler summer temps. The near-term outlook is uninspiring with the Gulf LNG drop pushed out and still widely anticipated (priced-in?), and the additional, negative revenue impact from the rate cases and contract expiry's. In our view, EPB is a sell, but not a short; we prefer the KMP short for several reasons, including our belief that KMP may acquire EPB at some point.

Conference Call Q&A

We got some air time on the conference call yesterday, and we used the opportunity to explore what we believe is one of KMP’s biggest issues, understated sustaining CapEx. While the questions weren't exactly answered, we got our point across - DCF is not FCF:

"Question – Kevin Kaiser: A question on CapEx for gathering and processing. What is CapEx budget for gathering and processing on a quarterly basis including Copano?

Answer – Steve Kean: I don't know if we have that number broken down.

Answer – Rich Kinder: We don't break it out separately. It's part of our natural gas CapEx.

Answer – Steve Kean: We have CapEx on Copano and Altamont and some in Texas, some in other -- in Texas as well but we don't have a break out of that.

Question – Kevin Kaiser: Okay so no break out for G&P by sustaining CapEx versus expansion CapEx either?

Answer – Steve Kean: No, I think that's just aggregated in our total Gas Group.

Answer – Rich Kinder: Total Natural Gas segment aggregates all of the -- whether sustaining CapEx or the expansion CapEx is all aggregated.

Question – Kevin Kaiser: Okay, and then on the Company wide -- so the budget for this year for sustaining CapEx will be $339 million. That's before Copano. If KMP only spent that on an annual basis, so no organic expansion CapEx, how would the segments perform over the long term? Would the Company be able to keep cash flow flat?

Answer – Rich Kinder: I'm sorry, I don't--

Answer – Kim Dang: Well, I think that we have growth -- are you asking if there's growth absent spending CapEx in KMP?

Question – Kevin Kaiser: The question is really if the budget was only limited to the sustaining CapEx, would the additional asset base be able to -- would it be maintained -- would the cash flows be maintained over the long term $339 million?

Answer – Rich Kinder: Oh, I see your question. Yes, we've said this several times and these are ballpark numbers, of course, but generally speaking that 5% or 6% this year happens to be 7% growth in distributions. We think probably 1.5% to 2% is organic growth, in other words, if you didn't spend any capital you would get that. At KMP that comes from a number of things. One is, of course, the inflation escalator that we have on our FERC-regulated products pipelines. The second is on automatic escalators that we have on some of our terminal assets. So you'd probably have we estimate 1.5% to 2% growth if you didn't spend any capital. And then the rest of that growth comes from -- primarily from new projects that come on line.

Answer – Steve Kean: That's obviously subject to market conditions. Market conditions determine the growth on just the existing asset base on a stand-alone basis.

Question – Kevin Kaiser: Right and how would 1% to 2% organic growth be possible with just $339 million if you spend about $400 million in E&P alone and that's not in the sustaining CapEx budget?

Answer – Rich Kinder: As I just said, I'm not following your question I guess. You ask how much organic growth you had without expansion CapEx and that's the kind of number that we use, about 1.5% to 2%. Kim?

Answer – Kim Dang: Kevin, is your question if CO2 production would stay flat if we weren't spending expansion capital?

Question – Kevin Kaiser: No, the question is really if you -- on the business, the entire KMP business how would cash flows trend over the long term if we only spend $339 million a year in Capital Expenditures.

Answer – Kim Dang: I think Rich just answered it.

Question – Kevin Kaiser: Okay and then the last question I have is do you consider distributable cash flow to be synonymous with free cash flow?

Answer – Kim Dang: Kevin, look, what we're looking at is how much cash flow that the MLP generates before expansion capital. Because our partnership agreement requires us to finance expansion capital, to distribute everything that we generate and to finance our expansion capital. So what we are comparing, distributable cash flow is to the cash flow that we have available for distributions to our unit holders before we factor in expansion CapEx.

Question – Kevin Kaiser: Okay, so you would say it's not -- you would not say that free cash flow and distributable cash flow are the same thing?

Answer – Kim Dang: If you're defining free cash flow as cash flow after expansion CapEx, then I would say that distributable cash flow and free cash flow are not the same thing but it depends on how you're defining free cash flow.

Question – Kevin Kaiser: I would define free cash flow as cash flow from operations minus the capital expenditures needed on an annual basis to maintain those cash flows from operations?

Answer – Kim Dang: Well that is not, unfortunately, that is nice that you would interpret it that way but that's not the way that our partnership agreement defines it and therefore, that's not the way we are allowed to segregate it." (Source: Thomson StreetEvents)

Kevin Kaiser

Senior Analyst