While broadly Consumer Staples names could now be considered a “defensive” play given the political uncertainty in Washington and Bernanke’s no-taper call (pushing yields lower, making staples names relatively more attractive), we think beverages remain overvalued with macro forces playing against the group.

To not mince words, but we’re not interested in getting long the trend of a ~ 3% annual decline in carbonated soft drink (CSD) volumes across the industry and a weakening emerging market environment – well-established as the growth engine for the sector. PEP is of course more diversified with 51% of its portfolio food, and we think the stock could continue to be supported on activist breakup news within the beverage business, however we’re not buyers of KO or PEP on the quarter’s print.

KO – There was much macro commentary on the call. The company again cited a “volatile” emerging market business, which we do not expect to inflect in Q4, despite management’s claim that it’s only a “temporary” impact. Europe broadly remains weak, with outperformance from Northwestern Europe (Germany in particular) and underperformance across the South.

Strong marketing plans for Q4, easier comps in the back half, and any pricing taking it’s able to capture, could help insulate Q4 performance, however, given the consumer moving out of CSD (including diet), and a still very weak macro environment globally, we’ll remain on the sideline on KO on the trend duration.

On Q3 2013 results: KO reported earnings yesterday morning, inline revenues ($12.03B vs $12.05B), declining -2.5% year-over-year, and inline EPS of $0.53 (incl. 5 cent FX headwind), up +3.9% year-over-year.

- Total volume was up +2.0% in the quarter (Americas +1%, International +3%)

- Company forecasts a currency headwinds of 5-6% in Q4

- CEO Kent said that the Mexican government’s decision to increase taxes on soda is the wrong step: regressive taxes have proven in the past not to work and that consumers are the ones that suffer in the end (article). He made no comment on how the company may handle/prepare for the results in Mexico

- Optimism around volume growth in China going forward. Volume +9% in the quarter

- Volume weakness (flat) in LatAm (Brazil and Mexico greatest neg. contributors) on more difficult +5% comp

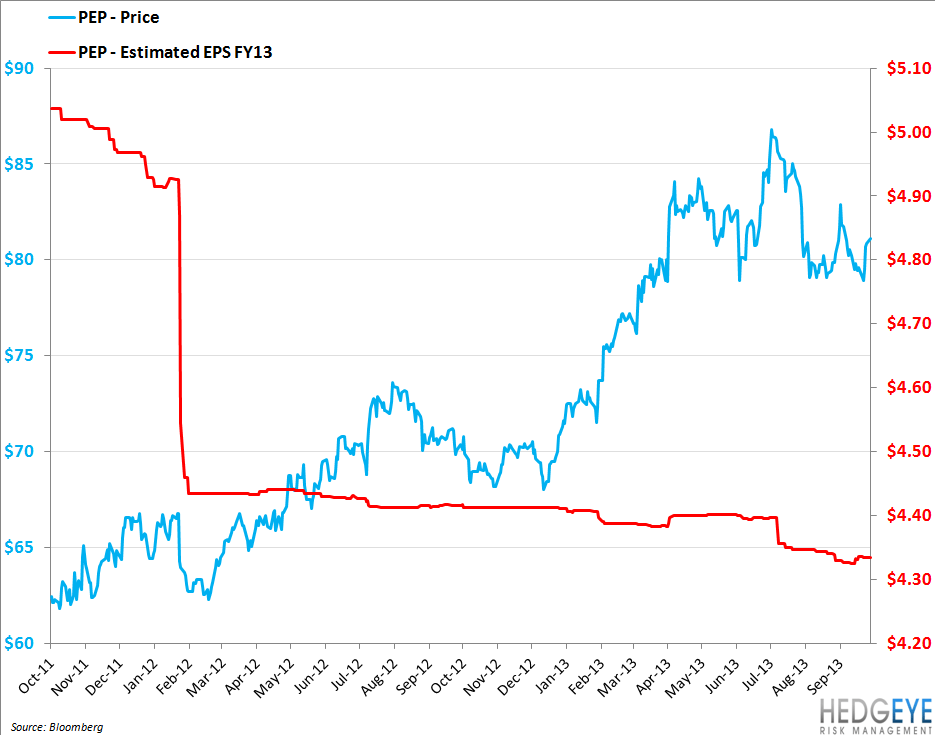

PEP – We believe the stock could continue to get support on activist news, including such options that PEP acquires Mondelez (MDLZ) and spins off the beverage business or PEP separates the existing business between beverage and food. CEO Nooyi addressed questions on the call by saying the company is looking into “sensible value-creating structural solutions” on beverages. All that said, we’re not buyers of the stock here. As our charts below suggest, we think the stock price has more risk than reward given the trend of declining earnings estimates and its premium P/E valuation over an overvalued group.

On Q3 2013 results: this morning, PEP reported revenues that slightly missed consensus estimates (reported $16.9B vs $17B), up 1.5%, and EPS outperformance ($1.24 vs $1.17). The 10.7% EPS increase year-over-year was driven primarily by a lower than expected tax rate (25.5% or 80bps below last year) that contribute 6 cents of upside. The company reaffirmed its FY2013 EPS growth guidance of 7%.

- Total volume was up +3% on the quarter (Snacks 3%/Beverages 1%)

- Asia, Middle East & Africa (AMEA) sales underperformed, down -3.4% Y/Y

- Frito Lay North America sales were strong at +4.7% Y/Y

- PepsiCo Americas Beverages sales were down -2.2% Y/Y with volume down -4%

- Took price up ~$3 in the quarter

Valuation: While we never base our investment preference on valuation alone, the chart below shows that both the Beverage group and KO and PEP are overvalued and trading well above historical averages. Further, we think the direction of earnings estimates going into next quarter is flat to lower, suggesting that price has more downside than upside going forward.

Matthew Hedrick

Senior Analyst