EVENTS TO WATCH OVER THE NEXT 24 HOURS

Hedgeye RH Black Book: Today at 11am.

CALL DETAILS

- Toll Free Number:

- Direct Dial Number:

- Conference Code: 779954#

- Materials: CLICK HERE

CONTACT

Please email for further details

ECONOMIC DATA

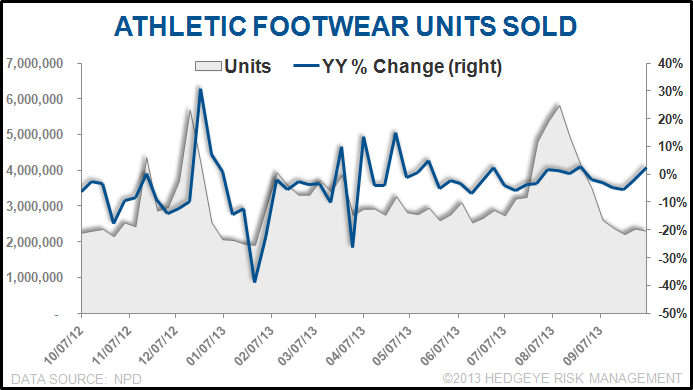

Weekly Athletic Footwear Data -

Takeaway: Here's a shocker…athletic shoe sales last week were up nearly 7%, which marks a 1,000bp acceleration from the prior week -- and the run-rate from the past two months. The key driver was a double in the growth rate for the Nike Brand, and a colossal acceleration in Brand Jordan.

COMPANY NEWS

WWW - Sperry Top-Sider to Launch Apparel for Fall

- "The 78-year-old brand, best known for its boat shoes, has turned to LF USA to launch a men’s and women’s lifestyle collection for fall. The collection will be unveiled to retailers at an event in New York on Thursday."

- "Paul Raffin, president of LF USA...expects the line to be a $100 million business at wholesale."

- "The apparel will reflect that same pricing. Tops will retail for $70 to $100 and bottoms from $80 to $100. Outerwear will average $100 to $300, but certain pieces will sell for up to $600."

Takeaway: Like all things with WWW, they're lowballing on the $100mm goal. Every $100mm grows the Sperry business by about 20%.

M - Macy's stores to open on U.S. Thanksgiving for first time

(http://www.reuters.com/article/2013/10/14/us-macys-thanksgiving-idUSBRE99D0R620131014)

- "[Macy's] said on Monday that most of its stores will open on the U.S. Thanksgiving Day holiday for the first time in its history, in a sign of how competitive the holiday season is shaping up."

- "Macy's will open the doors at most of its 800 namesake department stores, at 8 p.m. on Thursday, November 28. The company said the shift was voluntary for workers and that the move was 'consistent' with what many rivals are doing."

Takeaway: We didn't think that Black Friday could kick off any sooner. On one hand, we question how many people will shop on Thanksgiving. With the exception of the Fourth of July, it is the only major holiday that is literally celebrated by all -- regardless of race or religion. On the flip side, it is going to be tough for all competitors to follow suit -- especially on such short notice. This might give M a little leg up this holiday. On the flip side, the cost to open the store on Thanksgiving will be very high (it's overtime for anyone that punches in). They'd better.

NKE - Nike Unveils Nike+ FuelBand SE

- "Stefan Olander, Nike Inc.’s vice president of digital sport, unveiled the Nike+ FuelBand SE at a forum in TriBeCa here Tuesday, setting the new model apart from the original, which was released in early 2012."

- "One of the most significant new features addresses a gripe many had with the band’s first iteration: it wasn’t able to track specific activities. The first version of the band is unable to discern if a user is indoor cycling or going for a run."

- "The Nike+ FuelBand app will also see an update, including a Groups functionality that allows users to form groups with their friends and easily share fuel data."

Takeaway: These are major improvements to the Fuelband (spoken by a die-hard user). With the old Fuelband, if you wanted to go for a bike ride, you had to clip the bracelet onto your shoelaces, which is a major pain. It also had an accuracy rate of 50-60% for non-running activities -- which is simply ridiculous.

WMT - Wal-Mart Sets Sales Goal of $500B

- "Wal-Mart Stores...aims for sales of $500 billion by 2016 — without acquisitions. Mike Duke, the company’s president and chief executive officer, revealed the target at Wal-Mart’s annual meeting for the investment community on Tuesday."

- "...the retailer’s e-commerce activities, which were expected to generate revenues of $9 billion in the current fiscal year, but in May that was raised to $10 billion. Walmart.com is seen having sales of $13 billion in 2014…"

Takeaway: $13bn in dot.com sales is a big number, but relative to the size of WMT in aggregate, it actually puts the company at the bottom of the barrel as it relates to e-commerce as a percent of total.

JCP - Penney denies rumor of bankruptcy counsel hire as stock falls

(http://www.reuters.com/article/2013/10/15/us-jcpenney-rumor-idUSBRE99E0TN20131015)

- "A [JCP] spokeswoman denied a market rumor on Tuesday that the department store chain had hired bankruptcy counsel, as shares slid as much as 8.3 percent."

- "Penney spokeswoman Kristin Kays said there was 'no truth to the rumor,' origins of which were unclear."

Takeaway: All it takes is a flat-out false rumor to get this stock down 8%. Just goes to show how people shoot first and think second with JCP.

LVMH - LVMH Sales Rise 1.7% in Q3

(http://www.wwd.com/business-news/financial/lvmh-sales-rise-17-in-q3-7225261?module=hp-topstories)

- "The French luxury goods giant said third-quarter revenues rose 1.7 percent to 7.02 billion euros, or $9.3 billion, with selective retailing the only business unit logging a double-digit gain, up 12.8 percent."

- "Stripping out the impact of currency fluctuations and acquisitions, the third-quarter gain stood at 8 percent, LVMH said, noting that only the wines and spirits and watches and jewelry divisions saw growth accelerate from the first half."

Takeaway: Booze and Timing drove sales -- not exactly a bullish statement on its' LV luxury goods business.

HBC - 424 Fifth: Hudson's Bay's New Sportswear Address

- "Hudson’s Bay Co. has big expectations for its new women’s private-label sportswear brand, 424 Fifth."

- "Named for Lord & Taylor’s Manhattan flagship address, the sportswear line is designed to rival brands such as Lauren Ralph Lauren, Calvin Klein, Michael Michael Kors and Vince Camuto on the better-price sportswear floor. The lifestyle collection will be carried in 49 Lord & Taylor stores in the U.S. and 92 Hudson’s Bay stores in Canada, as well as online. The line will be unveiled tonight at an event at The Glasshouses here."

Takeaway: A private label brand rivaling Ralph, Calvin and Kors? Sorry HBC, but I'll believe it when I see it.

SCC - Sears Canada’s head office braces for more layoffs under new CEO

"Head office employees at Sears Canada are bracing for more layoffs as the struggling retailer moves forward under its new turnaround specialist CEO…The scope of the pending cuts was not revealed, and no store-level employees will be affected, sources said."

Takeaway: Seriously…does this surprise anyone?

WTSL - The Wet Seal, Inc. Updates Third Quarter Comparable Store Sales and Earnings Per Share Guidance

(http://ir.wetsealinc.com/releasedetail.cfm?ReleaseID=797680)

- "[WTSL]...today announced that it is revising its financial guidance for the third quarter of fiscal 2013 ending November 2, 2013. The Company expects to report a comparable store sales increase in the low-single digits and net loss per diluted share in the range of $0.10 to $0.12, before non-cash asset impairments. This compares to prior guidance of a comparable store sales increase in the mid-single digits and net loss per diluted share in the range of $0.02 to $0.03, before non-cash asset impairments."

Takeaway: I can't believe this concept still exists. Just goes to show that retailers can hang on by a thread for far longer than anyone thinks.