Research Edge Portfolio Positions: LONG TIP/SHORT SHY

With no indication that the Fed has any intention of changing rate policy in the near term, the current spike in interest rate volatility is being largely viewed as a measure of fear in the face declining global confidence in the US balance sheet colliding with the reflation trade head on. The replacement rhetoric in advance of next week's BRIC summit may become louder over the weekend as the manic media refines its hysteria.

Yesterday's $11 billion 30-year auction drove volatile trading as the highest yields since 2007 drew in anxious buyers causing the futures to swing sharply back into firmly positive territory intraday . The prevailing perception that this buying was committed longs who agree with the Japanese finance minister's assessment of the US balance sheet is tempting, but the post auction yield also presented spread players already short the short end of the curve like us a chance to get off the bench at a lower low. With relentless supply showing no signs of letting up anytime soon it will be critical to us to see if buying can sustain through today's session into next week.

Volatility:

Currently, the implied volatility on July at-the-money options on TLT, the Barclays 20+ year treasury ETF, are registering at 20/21 -down slightly from levels earlier this week but still close to the VIX, which closed at 28. These converging volatility levels are visible in historical measures as well -as illustrated in the chart below, which shows realized 30 day volatility on TLT vs. the S&P 500. Clearly the jitters in the market support higher absolute yield levels in the intermediate term.

CORPORATE SPREADS:

Although the spread between investment grade debt and treasuries have now contracted to pre-Lehman levels, the chart below illustrates what a 450 basis point premium looks like in historical context. While it would be tempting to view the decision by management to issue bonds at these levels as an indication that their view is that absolute rates can rise faster than spreads will contract, but the reality for mid and lower grade issuers is probably much simpler: they are simply taking liquidity whenever and wherever they can find it after a long drought, and are likely more focused on their cash needs in 2 months than prevailing rates in 2 years.

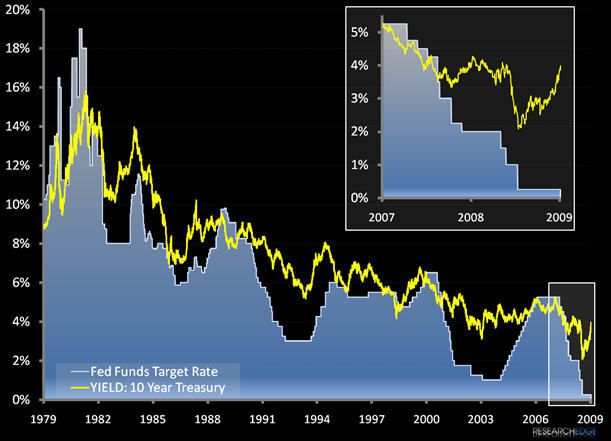

CONCLUSION

We remain of a mind that absolute rates can begin to rise in advance of any sentiment shift by Bernanke & co. as the market puts a premium on liquidity and discounts rhetoric, and also that the widening spread between the 10-year and the target is the beginning of a intermediate period trend that will see a flattening of the curve regardless of policy.

Currently we are short the short end of the curve via SHY and long reflation via TIP.

Andrew Barber

Director