We have been bearish on the casual dining sector since early July and, on Friday, Black Box gave us a look at September sales trends, which show a marginal improvement from an ugly July and August. Traffic trends, however, remain anemic. But, before we delve further into the details of the release, we thought it would be useful to point out which casual dining companies saw consensus metrix same-restaurant sales estimates adjusted in September.

The following companies saw 3Q13 same-restaurant sales estimates revised upward over the past month: EAT

The following companies saw 3Q13 same-restaurant sales estimates remain unchanged over the past month: BOBE, CBRL, CEC, KONA, RRGB, TXRH

The following companies saw 3Q13 same-restaurant sales estimates revised down over the past month: BBRG, BJRI, BLMN, BWLD, CAKE, CHUY, DIN, RUTH

Moving back to the release, Black Box reported that September 2013 same-restaurant sales increased +0.1%, while comparable traffic trends decreased -1.9% – same-restaurant sales improved +30 bps sequentially, while comparable traffic trends held flat. These estimates come against September 2012 comps of -0.8% and -2.4%, respectively. For the third quarter, same-restaurant sales and traffic are estimated to have declined -0.3% and -2.0%, respectively. Both metrics declined -70 bps and -10 bps, respectively, over the prior quarter.

Malcolm Knapp also released his September estimates last week. Knapp-Track casual dining comparable restaurant sales declined -1.9%, while comparable guest counts declined -3.6% – comparable restaurant sales decreased -10 bps and guest counts decreased -40 bps, sequentially. These results come against September 2012 comps of -0.5% and -2.3%, respectively.

For the third quarter, comparable restaurant sales and comparable guest counts are estimated to have declined -2.5% and -4.0%, respectively. This would indicate that both metrics declined -220 bps and -250 bps, respectively, over the prior quarter. Knapp also noted that comparable restaurant sales and comparable guest counts were negative for all four weeks in September.

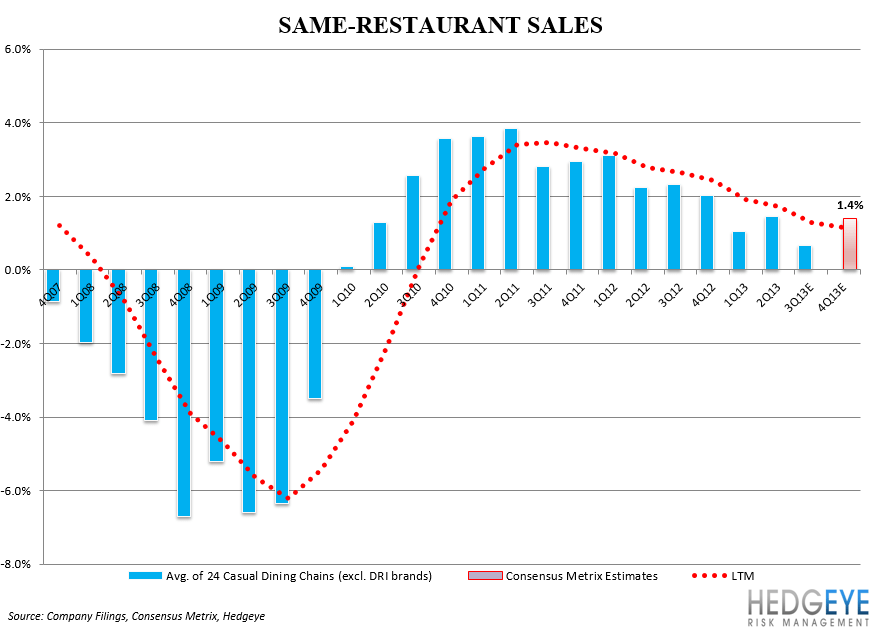

Currently, consensus metrix estimates for the 24 casual dining chains we track in the space are for 3Q13 same-restaurant sales growth of +0.7% (excluding DRI brands) versus +1.5% in 2Q13. This would imply a -40 bps sequential deceleration in same-restaurant sales on a trailing twelve month basis over the prior quarter.

Howard Penney

Managing Director