This note was originally published October 10, 2013 at 08:14 in Financials

Investment Company Institute Mutual Fund Data and ETF Money Flow:

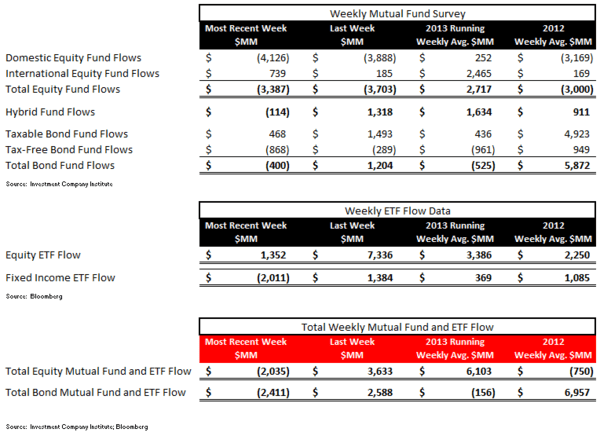

Fixed income mutual funds flow showed no follow through with an outflow of $400 million this week, a reversal from the $1.2 billion inflow last week which was the first inflow in 9 weeks

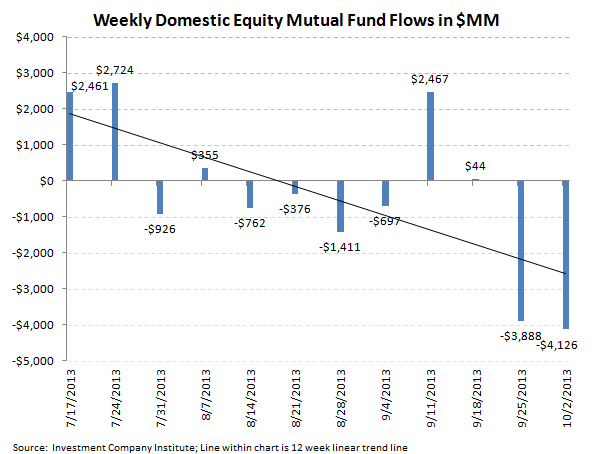

Equity mutual funds booked an another outflow of $3.3 billion for the 5 day period ending October 2nd, a continuation from the $3.7 billion redemption from last week

Within ETFs, passive equity products experienced inflow of $1.3 billion for the 5 day period ending October 2nd with Bond ETFs losing $2.0 billion of investor funds during the week

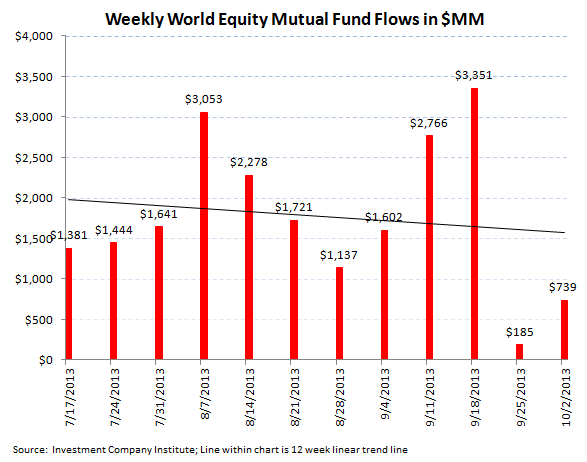

For the week ending October 2nd, the Investment Company Institute reported another weekly outflow in combined stock funds to the tune of $3.3 billion, essentially in line with the $3.7 billion outflow last week. The $3.3 billion outflow for the week broke out to a $739 million inflow into international equity products and a $4.1 billion outflow within domestic stock funds. The equity category has been a tale of two tapes recently with domestic equity funds having had outflows in 7 of the past 12 weeks compared to international equity funds which have had inflows every week in the past 12. Despite this weak run in domestic stock fund flows, the year-to-date weekly average for 2013 for all equity mutual funds now sits at a $2.7 billion, a complete reversal from the $3.0 billion outflow averaged per week in 2012.

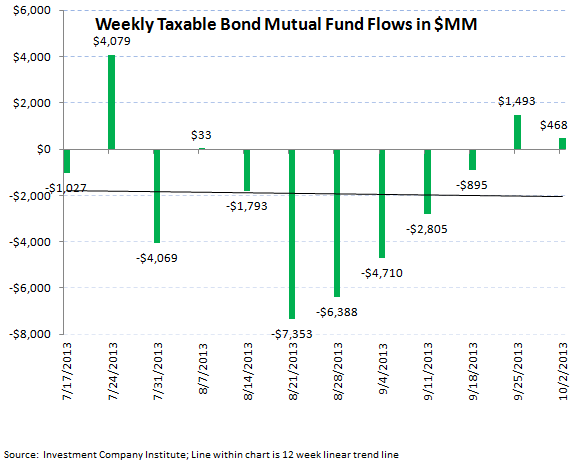

On the fixed income side, bond funds were not able to maintain the momentum from last week and for the 5 days ending October 2nd, the aggregate of taxable and tax-free bond funds booked a $400 million outflow. The taxable bond category had slight inflows of $468 million which was washed over by the $868 million outflow in tax-free or municipal bonds. While the sharp outflows that marked most of the summer and the start of the third quarter have moderated, the appetite for bonds has hardly rebounded. The 2013 weekly average for fixed income fund flows is now a $525 million weekly outflow, a far cry from the $5.8 billion weekly inflow averaged last year.

We highlighted the year-to-date tallies of this rotation from bonds and into equities last week with the first inflow into total equity funds in 6 years with stock funds running at a $106 billion inflow thus far in 2013. Conversely bond mutual funds are working on their first annual outflow since 2004 with a $23 billion outflow thus far in '13. This is a substantial reversal from the $303 billion inflow into fixed income funds as laid out in our research last week.

Within our asset management sector launch in the middle of the summer, we released our regression models that forecasted an prospective inflow for stock funds of $80 billion and conversely a forward 12 month outflow of $100 billion for bond funds. Thus far into our coverage of the asset managers, the equity rotation has occurred at a faster than expected rate and bond fund flows have been fairly stubborn, although our forecasts have been directionally relevant. As such, we continue to recommend investors are long leading equity manager T Rowe Price (TROW) to capture this shift and conversely avoid or be short a manager more dependent on bonds like Franklin Resources (BEN).

Hybrid funds, or products that combine both fixed income and equity allocation had a surprisingly light week with the first outflow in 14 weeks. The year-to-date weekly average inflow for hybrid products however is still $1.6 billion for '13, almost a 100% increase from 2012's $911 million weekly average.

Passive Products:

Exchange traded funds experienced mixed trends during last week with equity products booking an inflow and bond ETFs experiencing redemptions. Equity ETFs gathered $1.3 billion in funds, a deceleration from the $7.3 billion in the prior week and also down from the impressive $25.8 billion two week's ago. Including this week's production however, 2013 weekly average equity ETF trends are averaging a $3.3 billion weekly inflow, a strong improvement from last year's $2.2 billion weekly inflow average.

Bond ETFs experienced the first redemption in 5 weeks of $2.0 billion which was a reversal from the $1.3 billion in new funds garnered last week. Including this most recent outflow within passive bond products, the 2013 weekly bond ETF average is flagging at just a $369 million inflow, much lower than the $1.0 billion average weekly inflow from 2012.

In last week's ICI report we outlined the brewing ETF record for equities with 2013 thus far having produced $129 billion in stock ETF flow, well above the $117 billion produced in 2012 with still a quarter left in the year. Fixed income ETFs are struggling with just a $15 billion annual inflow year-to-date thus far in '13. This is well below 2012's trends of a $56 billion inflow.

Jonathan Casteleyn, CFA, CMT

203-562-6500

Joshua Steiner, CFA

203-562-6500