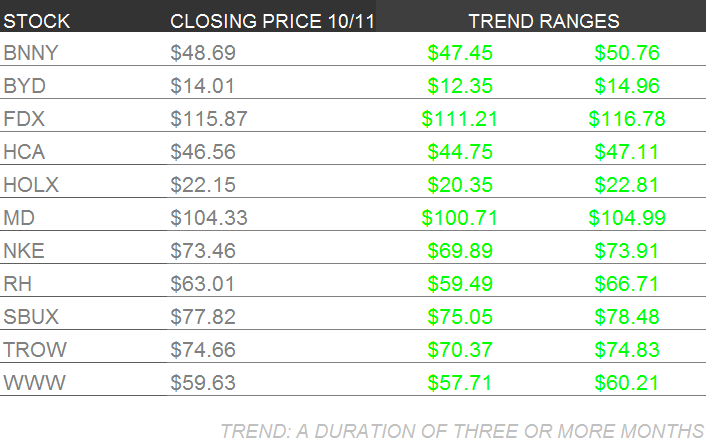

Below are the latest comments from our Sector Heads on their high-conviction stock ideas.

INVESTING IDEAS

BNNY – Consumer Staples analyst Matthew Hedrick says the long-term bullish picture continues to look rosy for Annie’s, as the health-conscious premium dining segment looks here to stay come economic rain or shine. This is truly what analysts call an “organic” story in both senses of the word – a fundamental long-term societal trend towards foods that are truly better for you. Hedrick notes that Keith’s proprietary risk management system flashed a buy signal on BNNY this week (see Real-Time Alerts for 10/9 which shows a buy on BNNY on an immediate-term TRADE pullback in the stock) and that the stock promptly snapped back to the upside. Hedgeye, keeping our eyes on your fries!

BYD – Boyd Gaming’s Borgata location, in Atlantic City, was awarded the first-ever Internet Gaming permit to be issued by the State of New Jersey. That’s eye-catching news, but Gaming, Lodging & Leisure sector head Todd Jordan says it will be some time before on-line gaming becomes a significant revenue source for the industry. Among the unknown issues are the demographics of gaming: how many people go to the casino for the “experience”? Let’s face it, not too many go there to actually win money…

The Las Vegas housing market continues to improve – as we note in this week’s Sector Spotlight: Retail (see below), Las Vegas luxury retail outlet rents have soared 25% over last year’s rent per square foot, indicating there may be additional gold in them thar hills. Jordan reminds us that the Las Vegas locals market was the worst performing gaming segment throughout the Great Recession. He looks for it to have the most upside as it travels back to peak revenues and profits.

FDX – As we head into the high-volume holiday shipping season, FedEx announced that it will add more labor to higher the bulge in volume than it did last year. Industrials sector head Jay Van Sciver says this is likely a positive sign for holiday activity, given FDX’s broader view into the economy. Van Sciver continues to think that FDX’s Express cost reductions can create significant shareholder value. Stronger US package volume wouldn’t hurt, either.

HCA – We held a call with the Jon Kingsdale this week. He knows a thing or two about Obamacare having led the effort to build the Health Connector in Massachusetts. In recent years, he has been acting as a consultant to many of the state and federal agencies, as well as private sector participants as the Exchanges went live this week (well sort of). Our takeaway was that there is likely to be further operational problems, and potentially cost overruns.

But in many other ways, the rise of the Exchanges and Obamacare, may be a bit player in the future of the US Medical Economy where Private Exchanges and defined health benefits are likely to have far reaching consequences. In the short term it appears many state Exchanges have managed to get their Exchange websites operational, although the true test won't be for another month when the real demand heats up.

As we look into Q3 results, expectations appear reasonable and falling, which is good since it lowers the likelihood of an HCA miss. Quest Diagnostics announced they had a weak quarter this week, and while there is a decent correlation between volume at DGX and HCA, HCA shares went up! That's the benefit of having low expectations in the short term and a big opportunity longer term. We'll be reviewing our long case up here near $47; between Obamacare, consolidation, pricing, Birth Recovery, and Utilization recovery, we need to review our thesis drivers. Some things have worked, and others, maybe not so much.

HOLX – Our October OB/GYN Tracking Survey launched this week. We'll have an update on the results next week.

MD – We wrote a note on MD yesterday updating our outlook. We're expecting a soft but not awful quarter for MD. Our OB/GYN survey is reporting a weak quarter for deliveries and pregnancies, as well surgical procedures, which are all very important to company trends. The year ago comparisons for volume growth are very difficult in the next two quarters, and we already saw some sequential softening in Q213. Despite the tough compare, results should be inline or potentially even a tiny bit better than consensus expectations.

Our primary concern is how the street reacts to a second negative, and potentially worse, volume number, and what has been a slow period for acquisitions for the company. Regarding acquisitions, MD needs to spend what looks to be another $250M out of a targeted $400M buying practices before the end of the year. If the company misses that target, I think everyone will be getting a very concerned, including us. Assuming they get the deals done, there is still plenty to look forward to as we head into 2014, though. Rising reimbursement rates (Obamacare), increasing numbers of insured (Obamacare) a Maternity Recovery (Economy) and another round of acquisitions, all appear likely to lead to earnings beats.

NKE – Retail sector head McGough attended this week’s Nike analyst meeting. While there were “no startling revelations,” McGough says “the focus and cohesiveness of the new management team was exceptional.” Among McGough’s high points were the company’s “maniacal quest to innovate,” its upside surprise in women’s apparel, and what looks like a truly earth-shaking retail development – the rollout of point-of-sale custom manufacturing capacity, where the consumer can have a shoe made “while-U-wait” right at the checkout counter.

To McGough’s surprise, none of the analysts even asked any questions about this initiative (Could it be Wall Street is already jaded by just-in-time manufacturing? Or have we watched so many reruns of Star Trek that we think the Replicator already actually exists?) “ . Simply put,” says McGough, “NKE deserves its 20x+ multiple all day. This stock won't make you rich here, but it'll still make you money -- and with a very low risk profile.”

RH – Retail sector head Brian McGough is looking for Restoration Hardware to earn $8 per share by 2018. His projections are far above the street consensus. Who will be right? The key lies with the consumer: will enough folks buy enough furniture from RH’s locations – and will on-line orders compensate for discontinuing their mail catalogue business – to make RH the long-term grand slam that McGough believes it will be? Will the consumer react favorably to RH’s new and expanding product lines? Can we expect the recent growth in sales per sq. foot to continue as RH continues to revamp its real estate portfolio; moving from 7,000 sq. ft. Legacy Stores to 45,000 sq. ft. Design Galleries?

The answers lie with the consumer – so McGough and his team asked consumers. Lots of them. McGough will present his proprietary review of the Home Furnishings space next week. Watch this space.

SBUX – Hedgeye Restaurants Sector Head has no update on Starbucks this week.

TROW – Senior Financials analyst Jonathan Casteleyn says the setup for the rotation from fixed income and into equities remains intact. The latest data this week from the Investment Company Institute (the trade group for the asset management industry in D.C.) flags continued weakness in bond fund flows and conversely stronger equity fund inflows.

The year-to-date averages for equity mutual fund flow is now $2.7 billion in new investor money per week, which compares to the $3 billion outflow on a weekly basis in 2012. This translates into a much improved environment for equity managers. Indeed, 2013 is working on the first net inflow into all stock funds since 2007. Fund flow chases performance. Like stocks (and housing) people want to invest with funds that have already done well.

T Rowe Price continues to maintain the industry’s top investment management performance, which should allow the company to gather up a disproportionate amount of nascent equity fund flow versus competitors. Casteleyn maintains his high-conviction call on the rotation into equities, with TROW as a major long-term beneficiary.

WWW – Retail sector head McGough continues to swing for the fences, focusing on names he thinks can return outsize profits to patient holders. In Retail terms, we might say he’s shopping strictly in the Big & Tall section, where 3X is considered skinny. This week he turned up the volume on Wolverine World Wide, saying the stock looks like a 2-year double.

McGough recognizes that this is a very non-consensus call – most of the street is down on WWW for a variety of reasons all, says McGough, very valid concerning problems the retailer used to have, but has now left behind them. With a “high quality management team and a very consistent long-term track record,” says McGough, WWW should see growth through market share expansion, coupled with improving margins and reduced leverage. McGough says this combination could “propel earnings growth into the 20%-30% range” and he likes WWW’s risk / reward profile for the coming year to 18 months.

Macro Theme of the Week – It’s De-Lightful, It’s De-Licious, It’s De-Fault

Hedgeye CEO Keith McCullough has been leading the charge to hold Washington nincompoops of all political stripes to account, not for differing political or economic ideologies, but for the rank fear-mongering that is the order of the day across the spectrum, all the while trading the patrimony of We The People for a mess of pottage. Whether your political emblem is a donkey, an elephant, or a chest full of tea, folks are increasingly reaching for the pitchforks, and we can’t blame them.

Moody’s CEO Raymond McDaniel threw cold water on Washington’s tempestuous teapot this week when he told CNBC “It is extremely unlikely that the Treasury is not going to continue to pay” its debts. McDaniel was noncommittal on whether Congress would pass a resolution to raise the debt ceiling, saying “Hopefully it is unlikely that we go past October 17 and fail to raise the debt ceiling…” How’s that for temporizing over a prediction? But in a key takeaway, Bloomberg quoted McDaniel as saying “Even if there’s not resolution on the debt ceiling, we think that the likelihood that Treasury security payments would be prioritized highly is strong.”

In this week’s Investing Term (see below), we take a look at the implications around the “D-word”. For now, let’s look at how the markets are reacting to the screaming match in Washington.

Scoping out the pre-market tea leaves on Monday morning, Keith said “Some might argue that US futures down 17 is a ‘capitulation’ signal – but context, when considering the emotion of it all, is always critical. At 1671 (my next line of immediate-term TRADE support), this will only be a -3% correction from the SP500’s all-time closing high. That’s hardly a capitulation.”

From a market technical point of view, spreads widened on US credit default swaps (CDS) – bets on the credit-worthiness of America’s sovereign debt – indicating that markets saw increasing risk of default. By contrast, CDS spreads narrowed on the PIIGS (Portugal, Italy, Ireland, Greece, and Spain – not as politically correct as the “BRICS,” but the money business isn’t always pretty), meaning the market was feeling relatively more sanguine about the outlook for Italy’s government-issued paper than ours. We get it that Italy watchers can finally exhale, now that the l’altra scarpa has dropped. Ex-PM Berlusconi has been convicted of fraud (a one-year sentence, possibly under house arrest) and of having sex with an underage prostitute (seven years bedroom arrest…?) The only open question remains: will he have to withdraw from Italy’s senate, or is he still fit to govern? Now how do you like Boehner and Obama?

As the week began, all the Fed-Fed jaw-jaw notwithstanding, the growth “style factors” in Hedgeye’s Macro model have barely corrected. Measured year-to-date, growth stocks as a group started the week up over 32%; the top 25% EPS growth companies in the S&P 500 were up 28%; and the top quartile of sales revenues growth stocks were up 27%. These figures were accompanied by 25% or better increases in stocks with high short interest, high beta (market-equivalent volatility), and the small cap stocks as a group.

“In other words,” Keith wrote, “given Bernanke re-established his Policy To Inflate (via Down Dollar) and D.C. has gone full gong show at the same time, the US #GrowthAccelerating style factor embedded in Friday’s closing prices is almost absurdly high!”

By Thursday of this week, the markets had cycled back (and forth… and back… and forth…) to the point where Keith was feeling a bit queasy (“As I was walking from one client meeting to another yesterday in Boston,” he noted, “I think I changed my US stock market view at least 3 times. Government sponsored volatility does that to a simple folk like me.”) As we have often observed, efforts by governments to meddle in market processes have two guaranteed outcomes: they shorten economic cycles by moving money through the system at unrealistic velocity (whether too fast or too slow), and they amplify market volatility – the knock-on effect of crunching economic events together like an out-of-tune accordion.

Add to that the tongue-wagging coming out of Washington. Here are just a few selected quips from Treasury Secretary Jack Lew testifying before Congress – “default,” “catastrophic,” “very dangerous,” and the “real risk of a financial crisis and recession that could echo the events of 2008 or worse.”

But wait a minute. Politicians don’t tell us when there’s a crisis in the markets. The markets tell us when there’s a crisis in the markets. We call your attention to Exhibit A – a Hedgeye TV video with CEO Keith McCullough and Director of Research Daryl Jones discussing the possibility of a debt default.

As we noted above, the spread on the US CDS has widened a bit lately – but it is nowhere near what market wags call the “Lehman Line.” Indeed, Jones says despite having widened in recent weeks, the spread remains low compared to the past few years, and is well below any hint of an actual risk of default. The “Lehman Line” measure kicks in at about 300 basis points of spread (three full percentage points), while the current spread is around 41 basis points, or 4 tenths of one per cent. (Jack Lew, are you reading this?)

Jones goes on to point out that the federal deficit has narrowed substantially over the past three years, saying this is a key fundamental driver of the bond market. So, while investors and fund managers are listening to the hysteria coming out of Washington – and its resonating echoes in the media – the bond market has largely shrugged off the fear talk. The market is focused on the fundamentals, which are not so dreadful as the headlines would have you believe. If there were imminent risk of a financial implosion, one imagines the 10-year Treasury would be trading at way above its current yield of 2.69%. This is a classic case of “watch what I do, not what I say,” where the markets totally get it, while investors perhaps not so much.

Jones notes that the narrowing deficit is a key measure of US creditworthiness, and that it indicates a significantly improving picture, all the hubbub aside. Put simply, the deficit is a measure of America’s ability to service its current debt obligations. This is probably what Moody’s CEO McDaniels was looking at when he said it is unlikely that the nation defaults on its debts.

And the debate needs to be viewed in its component parts: failure on the part of the government to raise the debt ceiling does not automatically translate into debt default. All the screaming and finger-pointing notwithstanding, if there’s not agreement come October 17th, the Chinese will not be mobbing the Federal Reserve in lower Manhattan demanding three trillion dollars is cash. Washington will do what Washington does best. They will move stuff around to keep their own paychecks flowing.

To be sure, there will be some discomfort. Veterans, the disabled, and the poor on special assistance programs may get temporarily screwed out of their benefits – but that’s business as usual. The substantial difference is that a family whose benefits check is delayed for a month may find themselves in default on their mortgage. That’s not the same as the US defaulting on its debt. Between now and the “drop dead date” of October 17th, the real risk is not that the US might default on its debt. It is that government inability to move forward will significantly slow economic growth domestically, while at the same time further undermining the confidence We The People have in our elected officials. One would think even the folks in Washington would understand that.

One apparently does. Or didn’t you catch the speech on the House floor by Rep. Alan Grayson? We admit to having a soft spot for Grayson. During the Financial Crisis hearings he turned out to be one of the only people in the room (Wall Street executives included) who actually understood what was going on. This week the Speaker pro tem tried to gavel Grayson out of order as the Florida Democrat quoted a national survey that found Congress is now less popular than hemorrhoids, toenail fungus, and dog poop.

Of course, the survey only asked Americans. Come October 18th, we’ll find out what the Chinese think.

Sector Spotlight – Retail

If “the business of America is business,” then the consumer is truly king. America’s economy is 70% driven by the consumer. And when we say “the economy,” that very much includes the consumer’s impact on the stock market.

Between brushing your teeth, combing your hair, showering, dressing, and grabbing that quick bagel and latte, by the time you get to work in the morning you have used products manufactured and marketed through dozens of companies – among them some of the premier listed companies in America. Wall Street analysts often start out covering the Retail sector, largely because it provides excellent basic training in analytical concepts.

Such notions as Same Store Sales, inventory turnover, and critical basic accounting concepts such as FIFO / LIFO, cost of goods sold, and decisions around when to recognize revenues and profits – all these and many more are the very nuts and bolts of retail. They translate into similar concepts across nearly every industry group – but it is the Retail analyst who sees these in their purest form.

That is not to say that getting a handle on Retail is a simple exercise. The fact that you routinely buy such items as coffee, socks, newspapers, blouses, cigarettes, wine and athletic shoes in no way qualifies you to project the success of a retail business. Still, many folks on Wall Street look at Retail analysts the way guys at a frat house dance look at the drummer – “Oh, Dude! I could totally do that!” Take it from Hedgeye’s star Retail sector head McGough: it ain’t that simple.

McGough is well represented with the Investing Ideas listed above – long-term portfolio positions where he has a very high level of conviction. But his sector is not necessarily sanguine across the board. This week we offer a few key takeaways – both high points and low ones that caught McGough’s expert eye as he scanned the trades.

NKE

Apparel analysts follow sales trends closely. This week – which McGough calls positively “gnarly looking” – saw athletic footwear sales volume down 4.9%. McGough says “ASP, which had been the big saving grace for the past three months, took a complete nosedive,” while UnderArmour and Timberland managed to toe the mark on reasonable sales figures (our stupid pun – please don’t blame McGough.) McGough says “polar opposite results” are coming from apparel data – notably from Investing Idea Nike. It’s too early to tell whether we should expect a Christmas disappointment. If so, NKE will be the best house in a bad neighborhood.

JCP

JCP announced that Stephen Sadove, who is about to step down as CEO of Saks, after successfully completing his company’s merger with Hudson’s Bay Co, will join the JCP board of directors. McGough calls this big news for JCP. He notes that critics are concerned that Sadove is too “luxury oriented” and will take the wrong view of JCP’s customer base. But after the failed experiment that tried to turn JCP into an “Apple Genius Bar” for sweatshirts, says McGough, “we could care less about what KIND of product he sold throughout his career, the reality is that Sandove gets retailing, and that’s a positive.”

UGG

NKE is not the only footwear maker to go custom. UGG just announced the launch of “UGG By You,” which it calls “an online customization tool putting customers in control of the design process.” UGG says there are over 11,000 design and material combinations possible using their new customization tool – though we wonder how many of those will end up being as useful as those extra 900 channels on our HD-cable box. McGough says this is inevitable. “Everyone is ultimately going the customization route,” he notes. This may be a bigger thing than many consumers recognize. There is a segment of the population (your correspondent among them) who consider themselves “hard-to-fit” for footwear. But it’s a basic retail adage that People Never Know What They Want Until They See What They Can Have. We would expect this to be today’s gimmick, tomorrow’s necessity. As to the immediate splash UGG may have expected from this announcement, McGough says, “Unfortunately, Nike just upped the ante with location-based customization. In other words, you order your shoes, and get them in 3 hours instead of six weeks.”

AMZN

Last, and most definitely not least, the on-line retailer that started it all. Bricks and mortar stores continue to attract a seemingly permanent upscale clientele made up of the kind of people who slum with their buddies Oprah and Bianca Jagger. Collier’s International reports this week that retail space on Manhattan’s Fifth Avenue is the highest on the planet – at an average of $3,052 per square foot. In fact, Collier’s reports that popular retail destinations across the US are seeing big increases in rent. Some of this is no doubt thanks to easy comparison to last year’s depressed prices. Las Vegas, for example, saw rents on the Boulevard leap by 25%. But the fact remains that ultra-high-end retail never seems to go out of style.

At the other end of the real estate spectrum, AMZN is launching its Luxury Beauty Store to sell “prestige cosmetics” on line. “We have luxury shoppers,” says the AMZN executive in charge of the project, calling this the first step in bringing luxury brands to AMZN’s high-end customers. Does this finally herald the end of bricks and mortar? We guess people used to spending $25,000 and up on a handbag will continue to value their “shopping experience.” (If you are one of them, please give us a call. We’d be fascinated to find out what it feels like to spend more money on accessories in one shopping spree than the average American middle-class family lives on in an entire year.)

And Finally… Caveat Emptor

Speaking of Amazon, in the excitement over the upcoming Twitter IPO, the Wall Street Journal observes “investors are showing increasing hunger for initial public offerings of unprofitable technology companies.” (WSJ, 11 October, “In New IPOs, Profits Aren’t the Point”) AMZN is, famously, a company that hadn’t made money when it went public, and that kept not making money for years – as its stock price continued to rise. And today… well as they say, the rest is history.

Who wants to own the next AMZN? The Journal say 68% of US-listed tech IPOs this year were companies that lost money in the prior fiscal year or trailing twelve months, noting “That is the highest percentage since 2007, and 2001 before that.”

That’s an aside that should send you scurrying to your history books (on your Kindle, presumably). We note that 2001 was the year that led into the bursting of the internet bubble and substantial stock market losses the following year. And even a seasoned Wall Street investment banker with no clue of what happened in the world the day before yesterday must remember what happened in 2008. Are consumer preferences leading indicators? Is this the wisdom of crowds, or the madness?

For now all we can tell you is that market participants continue to participate, while market watchers continue to watch. It’s always like this right before people lose a whole lot of money.

Investing Term – Default: It Depends On What The Meaning Of “Is” Is

Government word-Meisters must be going into overdrive as the 17th of October looms, scurrying to piece together a working definition of “Default” broad enough and flexible enough to permit the President to lay blame where he will, while sidestepping responsibility himself.

Speaking of “word-Meisters,” have you noticed how the (unelected) folks running the nation’s financial system have a particular penchant for perpetuating panic? It was none other than Ben Bernanke who coined the fearful term “Fiscal Cliff.” Now we are being told there is a fiscal drop-dead date of October 17th – a date seemingly conjured up out of the ether. That if we fail to come to a full and definitive resolution by October 17th, giving the government a free hand to run the printing presses flat out, the entire American Way of Life and all we stand for will vanish with a gurgle down the Johnny-flusher. Congress and Presidents hew as timorously and unquestioningly to their monetary PhDs as did Agamemnon to his readers of entrails and bird flight – generally with as successful an outcome.

But we digress…

The basic definition of financial Default is, failure to make a required payment on schedule. In the context of the current hysteria, the word is being thrown about with abandon. We suggest that context is critical – and must be borne in mind when contemplating policy options.

Who actually decides when the US goes into “Default”?

If you guessed “The Government,” congratulations. Normally we would send you to the head of the class, but the schoolhouse is closed, having been deemed a “non-essential service” during the partial government shutdown.

For that matter, who decides what is “essential”? Or which “parts” get shut down? For starters, you should fully expect that any “parts” of the government that remain shut down come October 18th will not be making their routine payments to the persons or entities they normally service. And we would bet that failure of those shut down non-essential offices will be called not a Default, but a “suspension.”

Treasury Secretary Lew said the Congress is “playing with fire” if they think they can pick and choose which debts to service, and which to allow to go unpaid. He went so far as to say that even waiting until the eleventh hour before striking a bargain constitutes an outrage and poses a threat to the nation’s well-being. Imagine.

A Trillion Here, A Trillion There…

According to the Treasury’s own statistics (www.treasurydirect.gov) there is currently nearly $17 trillion in Treasury debt outstanding, of which $4.8 trillion is actually owned by the government itself. In our more deranged moments, we have allowed ourselves to muse on the implications of repudiating the nation’s debt entirely. More recently, we have contemplated seriously the implications of cutting that debt into tranches, the way investment banks did with the proliferation of asset-backed securities (ABS) that contributed so mightily to sinking the ship of our economy in recent years.

Our idea would be to slice up Treasury debt, not by its creditworthiness – all Treasury debt is by definition equally creditworthy – but by priority of debt service. At the top of the pyramid would be the approximately $5.6 trillion held by foreigners. Led by our friends the Chinese ($1.3 trillion), followed immediately by Japan ($1.1 trillion). Europe combined holds another trillion, while Brazil all by itself is the third-largest single country holder of Treasury debt, with about $256 billion. Clearly, in order to maintain our standing as Top Dog in the global reserve currency pit, we would have to provide ironclad guarantees on all that debt.

But what about other, less important holders? The argument is being made in Washington – albeit mostly obliquely – that we can stiff some less powerful holders of federal IOUs without losing our global status.

First off, note that the Treasury makes some 80 million payments a month. Who’s gonna notice if a few of them go missing? If you are not the one whose payments failed to come through, no one else will know about it.

We offer the example of a military family. Unlike the contractors who furnish materiel and advanced weaponry, families of our men and women in uniform often suffer ongoing financial hardship, as military wages fail to quite make ends meet. Like so many other undertakings that look like a lot of fun, the military life is economically viable for an unattached 19 year-old, but becomes suddenly and rudely a challenge with spouse and two or three children in tow.

We put it to you that one of the most damaging sequelae of this whole nauseous debate has already left its imprint on our nation. The idea of divvying up payments to stave off the D-word rests on the assumption that some payments are more important than others. That is, that some payees are more important than others. The trillion-plus held by China ranks much higher than the death benefits owed to the widow and children of a Marine who died in the mountains of Afghanistan. The economic reality of America as a high-low society has long since been established. It is now being ratified as Congress brands certain classes of people not worthy of having the government keep its word to them.

Given the shameful record of so much of our government – and our broader society, for that matter – in treatment of veterans, we were not shocked that vets’ payments were deemed “non-essential” in the first go-‘round, and that Congress actually needed to be shamed into restoring the beggar’s mite that goes to those who lay their lives on the line to protect us. As a public service, we remind Congress that American men and women in uniform continue to die almost daily in distant parts of the world.

An Immodest Proposal

Our idea is radically different. We hope Washington is listening.

In the world of High Finance, CDS are negotiated between major banks. Key among the terms of the contract is the “credit event,” commonly defined as any impediment, speed bump, or alteration in required payments. In normal banking – on consumer loans, for example – an individual who misses a payment will be put into arrears. After a certain period of time, especially if multiple payments are outstanding, the individual will be deemed “Delinquent.” Part of the reason is that banks need loans to always appear to be fully current, otherwise it weakens their balance sheets and they are required to post more capital. This became a major issue during the financial crisis, when no bank wanted to write down its mortgage portfolio, even though house prices were down by as much as half in many areas of the country.

In the world of CDS, missing a single payment can be deemed a Credit Event – even making the payment late – throwing the banks on either side of the contract into a legal battle, as the buyer of the CDS demands payment in full, while the issuer drags their feet.

But not so our government. The government actually has the power to fail to make payments, while declaring itself to be not in default. (Remember, this is the government that said the Egyptian army arresting the elected president and gunning down demonstrators was not a “coup.”) Failure of Congress to authorize a debt ceiling increase does not constitute a “credit event.” And it certainly does not, by itself, constitute “Default.” We would admonish politicians to be more circumspect in their choice of words, but there you are… sort of thing…

We propose that the government chop up the nearly $5 trillion of Treasury debt owned directly by the government into high-pay and low-pay tranches.

The QE-endless program would be an excellent way to start. Janet Yellen could make her indelible mark on monetary policy history by simply retiring all the Treasury debt bought by the Treasury under the range of QE programs. What’s that?!!! you ask, horrified. The US will simply cancel its debt?! If you think about it, the Treasury issues debt, then prints money to purchase that debt back in the open market. It does this in order to inject liquidity into the financial system, in a bid to stimulate economic activity (how’s that working out for you, Mr. Bernanke?) Since it is the government’s own debt that is being bought back by its original issuer – and with dollar bills issued by ditto – canceling the debt would be the equivalent of you forgiving yourself a loan that you never made to yourself.

When you put it that way, it becomes absolutely compelling.

Economists recoil in horror at this proposition, saying the first thing that would happen is the interest rates on US debt would soar as the bottom falls out of the Treasurys market.

But first, we have wiped out nearly $5 trillion in debt, lowering the annual deficit by a massive number. And this also means we can buy China’s trillion-worth back a lot cheaper. As a prelude to this massive plug-pulling, we would launch global negotiations with foreign holders which would result in us making them whole on their current holdings, in return for them buying more at the new levels. The way we figure it, higher interest rates end up being a draw for global investment. Put another way, even if the US were to do something so brazen, once the dust clears, are you really going to take your money and invest it in Brazil? In Italy? In China?

This idea is so freakin’ insane we predict it will be put forward by someone in Washington before this shootin’ match is over.

#TimeStamp, baby!

- Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street