TODAY’S S&P 500 SET-UP – October 11, 2013

As we look at today's setup for the S&P 500, the range is 26 points or 0.62% downside to 1682 and 0.91% upside to 1708.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.34 from 2.34

- VIX closed at 16.48 1 day percent change of -15.92%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:55am: U Mich. Confidence, Oct. prelim, est. 75.9 (pr 77.5)

- 11am: Fed’s Powell speaks on monetary policy in Washington

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 1pm: Fed’s Rosengren at Council of Foreign Relations in N.Y.

- 1pm: Baker Hughes rig count

GOVERNMENT:

- 9am: Natural Resources Defense Council, Sierra Club, Canadian scientists and activists briefing on Canadian govt, climate policies, tar sands expansion, Keystone XL

- 10am: Joint Economic Cmte hearing on fiscal sustainability, economic growth

- 1:30pm: G-20 members hold IMF/World Bank press conferences

WHAT TO WATCH:

- House Republicans enter talks with Obama on debt-ceiling deal

- Default doubters repudiated by Republican economists citing harm

- Energy Future said near bankruptcy loan exceeding $3b

- Pimco said to raise $3.5b for Bravo II credit fund

- Del Monte Pacific to buy U.S. food brands for $1.68b

- Twitter said to pay 3.25% bankers’ fee in IPO topping $1b

- Potash Corp. cuts profit forecast amid market uncertainty

- Device sales delays possible as shutdown halts FCC reviews

- Brevan Howard said to start fund run by ex-Deutsche Bank team

- China Greenland to invest in $5b New York property deal

- Google moved EU8.8b in royalty payments to Bermuda in 2012: FT

- ESM’s Regling says Greece widely expected to need new bailout

- Royal Mail surges on opening following oversubscribed IPO

- U.S. Debt Deadline, China GDP, Google, GE: Wk Ahead Oct. 12-19

EARNINGS:

- JPMorgan Chase (JPM) 7am, $1.29 - Preview

- Webster Financial (WBS) 8am, $0.49

- Wells Fargo (WFC) 8am, $0.97 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Corn Tumbles to Three-Year Low on U.S. Harvest, Ethanol Mandate

- Gold Analysts Bearish on Signs of U.S. Compromise: Commodities

- IEA Sees Oil Output From Outside OPEC Rising Most Since 1970s

- Cocoa Jumps to Highest in Almost Two Years as Supply Falls Short

- Copper Rises for Second Day on Strengthening Chinese Car Sales

- WTI Crude Set for Weekly Decline; IEA Sees Non-OPEC Supply Boom

- Gold Heads for Second Weekly Loss as U.S. Impasse Seen Ending

- Rebar Gains for Second Week on China Restocking, Iron Ore Prices

- Falling Copper Grades Show Super Cycle Intact: Chart of the Day

- Coal 4-Year Low Lures Utilities Ignoring Climate: Energy Markets

- U.S. Oil Boom Races Against Red Queen as Shale Wells Fade Fast

- Shale Ascendancy in Europe Displaces Pipeline Gas: Bear Case

- Lukashenko Calls for Potash ‘Cartel’ Revival to Boost Price

- Sugar Climbs in New York as Brazil May Slow Sales for Now

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

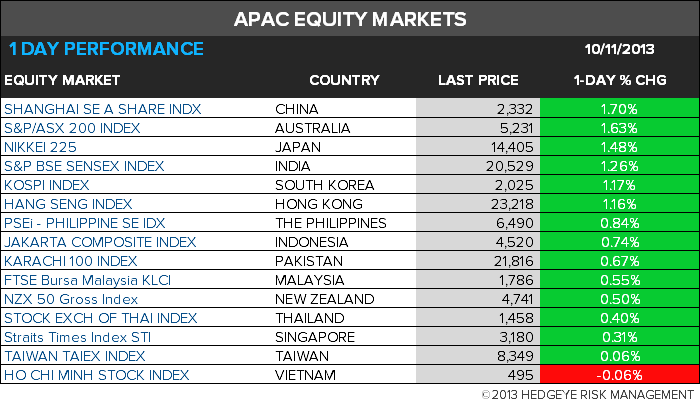

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team