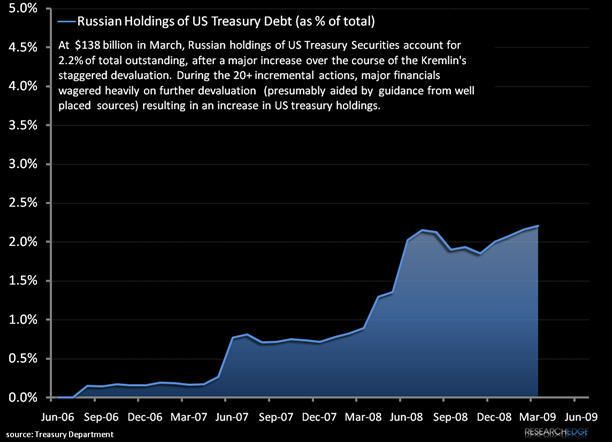

We had been in the midst of writing the note below that summarizes Russia's increased criticism of the U.S. Dollar as the global reserve currency when we picked up on newswires that Russia may actually start swapping U.S. Treasuries for IMF Debt. As the dollar continues to fall holders of US debt are rightfully seeking alternative vehicles. Russia has aggressively floated the idea of a supranational currency in the last ten days and countries from China to Brazil have voiced reducing their dependence on the dollar. While we very much believe "The Burning of the Buck" will have serious implications for global markets, Russia's recent bark (rhetoric) may be larger than its bite. The first chart below is an important call-out, showing the diminutive Russian Holding of US Treasury Debt as a percentage of total US debt.

The broader note below gives more context on this situation.

Muscle Flexing

Russia calls for a new global currency to replace the Greenback. Could rhetoric turn into action? (Yes, per above!)

Over the last week Russian President Dmitry Medvedev has openly questioned the future of the US dollar as the global currency, proposing both a "supranational" currency and the possibility of Ruble-Yuan swaps, a position he broached to western media and as host to an international economic forum in St. Petersburg over the weekend. And the debate has moved beyond the Kremlin in recent days with IMF First Deputy Managing Director John Lipsky saying that it's possible to take such a "revolutionary" step over time and World Bank President Robert Zoellick saying that China may diversify its holdings.

Here it's important to note that both Lipsky and Zoellick take mild stances, yet the possibility of a replacement currency to the USD is a real one. Yet if we stick with Medvedev's proposition it's clear that even if he doesn't have a firm idea of what a supranational currency would consist of, he does understand the value of using explicit soft power to heighten existing tensions between the US and China over the value of China's US debt holdings, especially following Geithner's failed trip to win over The Client, China.

But who is Russia hoping will benefit?

Ironically it's Russia who stands to benefit from the current devaluation of the USD, but not by issuing a new currency it can exchange in. Commodity-rich Russia is a major producer of world's oil supply, much of which is sold and traded in US dollars. As any commodity trader would tell you: when the base currency devalues, more dollars chase the commodity, lifting the price. While we don't discount other factors that play into the price of oil, including supply and geo-political risk factors, at a very basic level, it appears antithetical for Russia to want to replace the USD in the immediate term, as Russia benefits from the Reflation trade!

The chart below comparing the US dollar index versus the price of front month contracts of light sweet crude over ten years demonstrates a pretty accurate picture of the reflation trade. The correlation coefficient (R squared) is -0.8, signifying a high negative correlation between the USD and oil. Interestingly the more that Medvedev continues to talk down the dollar, the more likely it will continue to plunge = advantage Russia.

Matthew Hedrick

Analyst