Our answer: no.

On September 12th, we wrote a note stating that ENR was “Cheap for a Reason”. The crux of our thesis was that the macro and company-specific setup was not suggestive of upside in the stock price. At this level, we remain bearish on the name as the fundamental and quantitative outlook suggest that consensus price targets may need to come down over the near-to-intermediate term.

This stock could be a longer-term winner for investors, given the plethora of positive attributes in the company’s profile but we see material downside in the stock (as far as $80, from a quantitative perspective) over the next three to four quarters.

Summary Bullets:

- ENR’s wet shave business (37% of revenue) is exposed to declining U.S. industry trends

- Organic revenue growth remains anemic at best

- ENR holders may be on the wrong side of a “heads-I-win-tails-you-lose” macro outlook

Fundamental Outlook: We remain bearish on Energizer’s fundamental outlook as competitive pressures and industry declines impact some of the company’s most important businesses. During the most recent earnings call, on July 31st, management argued that the company was maintaining its share of the razors and blade category due to the successful launch of Hydro Disposables.

Whether or not that claim is accurate, the overall razors and blade category has continued to decline into 3Q and we expect negative top-line growth in that segment for ENR once again.

The household products segment remains challenging for Energizer as a combination of historically high promotional activity and a declining category impair the company’s ability to drive sales. The losses of two U.S. retailers will impact numbers by roughly 6% starting in 4Q and continuing for three quarters of FY14 at the same rate.

Despite earnings growth in the mid-single-digit range, we are reluctant to get behind the stock until the company’s organic growth outlook improves, or the stock becomes cheaper.

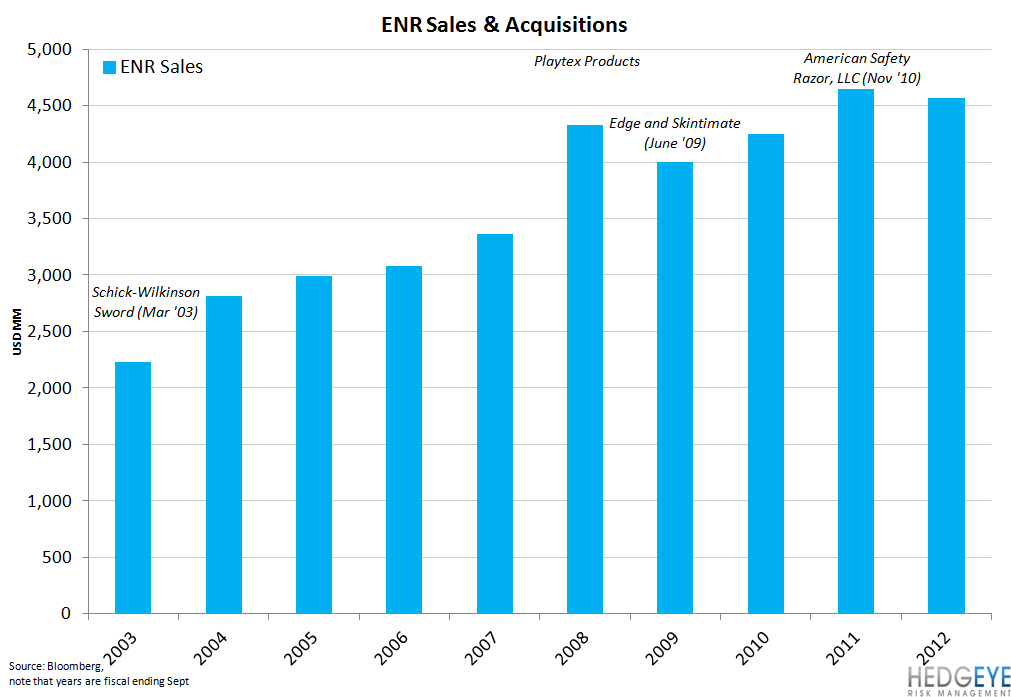

Organic Revenue Growth: Consistent organic growth, or the lack thereof, in Energizer’s business is a primary concern. Over the past 10 years, the company has driven revenue growth primarily through acquisitions. While the company can drive revenue through that strategy, we see organic growth as being central to creating shareholder value as the complexity of the company continues to increase. The most recent acquisition of J&J’s feminine hygiene brands has not been met with enthusiasm by the market with the share price declining -12% since the announcement versus the S&P 500 down 42 bps and HPPC peers average of up 23 bps.

Note that the +3.7% organic sales growth in Household Products was due “primarily to increased shipments versus soft prior year comparisons and higher promotional activities in the U.S., and distribution gains in Asia.” In the fourth quarter, HP global sales will decline by more than 10% due to market share losses, promotional and shipment timing, and storm-related volume in the prior year quarter, according to management.

Macro: This is a difficult point to prove but we think some readers may find it interesting.

- The expectations of interest rates rising makes buying a company (or division of a company) more expensive as buyers rush to complete deals

- The prospect of higher rates is likely to be a negative for ENR as the company’s dividend yield (an increasingly important part of the bull case) becomes less attractive on a relative basis.

- If, contrary to our Macro Team’s view, employment data deteriorates from here and the Federal Reserve maintains low rates on the basis of a weak labor economy, that would also be negative for ENR and consumption more broadly.

Other Factors: We see Energizer as a company that has many risks weighing on the value of its equity. Besides the slow growth of its major divisions, we see some other risks as being noteworthy:

- Sentiment has shot to the upside over the last six months and we see peak or close-to-peak sentiment as bearish. The stock currently has 9 Buy ratings, 6 hold ratings, and 0 sell ratings. As of the most recent data, 4.75% of the float is sold short

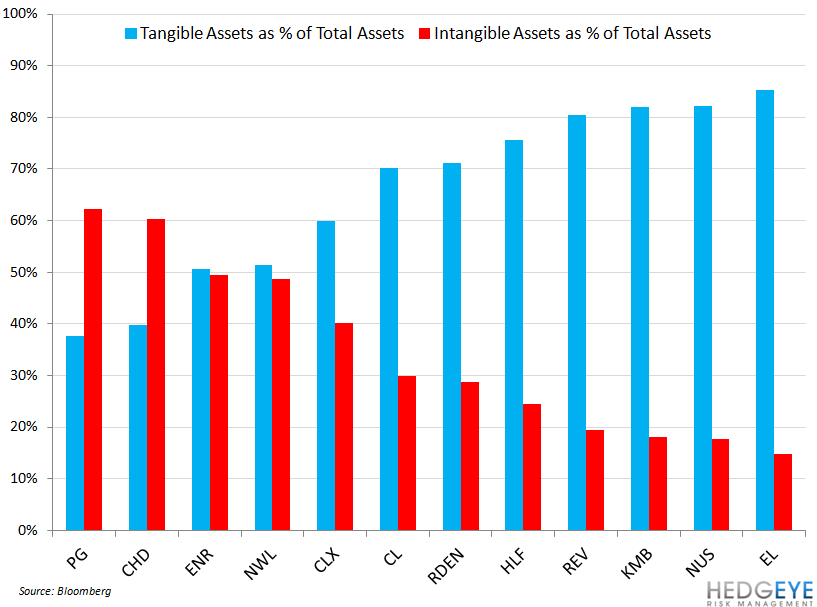

- Intangible Assets being such a high percentage of Total Assets is a latent risk that could be a factor for ENR and, potentially, the broader HPPC sector if impairment charges are incurred going forward

Rory Green

Senior Analyst