YUM continues to be our favorite LONG in the big cap QSR landscape and, despite facing significant volatility since December 2012, it’s long-term growth story remains intact.

The company will report 3Q13 earnings after the close tomorrow while simultaneously releasing same-store sales for the month of September.

As a reminder, Yum! Brands reported a -10% decline in same-store sales, versus an estimate of -7.7%, in August for the China Division. The August same-store sales results included a decline of -12% at KFC and an increase of +5% at Pizza Hut. Looking ahead to September, consensus expects a -5.7% decline in China same-store sales. Importantly, we believe the company will report positive same-store sales for both brands in the month of October and expect this trend to continue throughout the remainder of 4Q13 and into 2014.

As the reality of an improving top-line becomes common knowledge, we believe the stock will outperform its peer group. As sales begin to improve, the next real driver of sentiment moving forward will be the slope of the line in the margins of the China Division. All told, China margins actually held up better than expected in 1H13, as significant declines in traffic and mix were partially offset by lower food costs and improved labor productivity.

We expect to see margins in the remainder of 2H13 and 2014 to improve concurrently with an improvement in same-store sales. Management has previously acknowledged that they need mid-single digit same-store sales growth in China in order to fully offset inflation, and we believe a continued internal focus on margin management will likely lead to better than expected earnings in 4Q13 and 2014.

Since peaking at 22.6% in 1Q10 on a TTM basis, restaurant level margins in China are estimated to have declined by 770 bps in 3Q13. In our view, YUM will have one more ugly quarter. The trends in the China division may again, be difficult for some investors to swallow – restaurant level margins are expected to be down 310 bps in 3Q13 versus a decline of 500 bps in 2Q13. But, there is a light at the end of the tunnel. By 4Q13, restaurant level margins and operating margins will begin to improve on a year-over-year basis in China. Essentially, once we get past 3Q13 results, we expect YUM’s China Division will begin to improve significantly.

For 3Q13, we expect YUM to report numbers in the YRI and U.S. Divisions in-line with expectations, with the possibility that they could be slightly better.

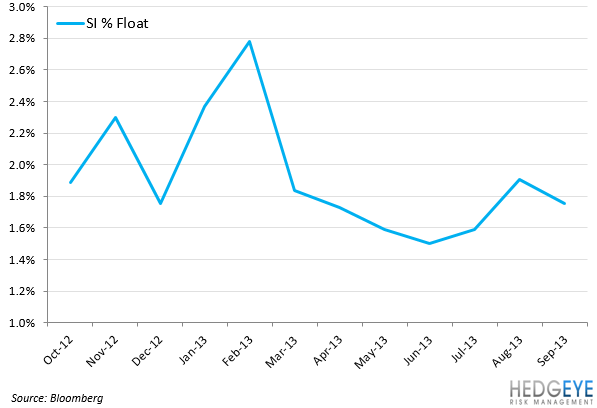

Sentiment on YUM is still fairly negative. Illustrated in the chart below, 39.3% of analysts rate YUM a Buy, 57.1% rate YUM a Hold, and 3.6% rate YUM a Sell. Short interest in the stock is rather muted at 1.75% of the float.

At a 10.9x EV/EBITDA, YUM is trading at a significant discount to its QSR peer group at 12x EV/EBITDA. We believe this valuation is reasonable – for now.

Howard Penney

Managing Director