CAKE remains on the Hedgeye Best Ideas list as a LONG.

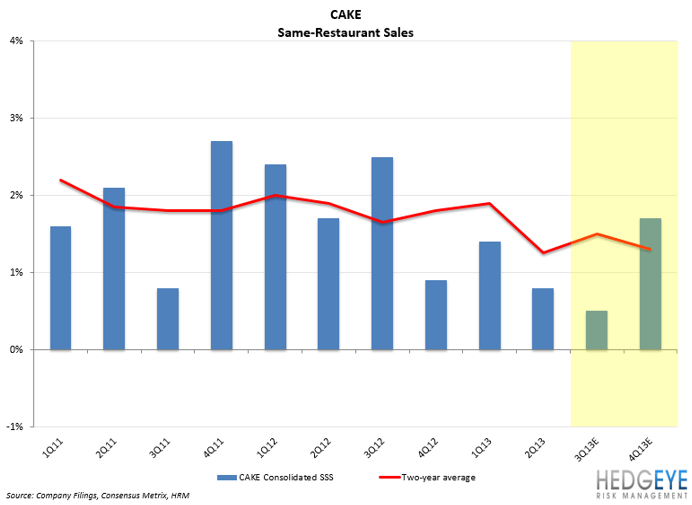

Same-Restaurant Sales Are Strong

Sales trends remain strong at CAKE, as the company continues to outperform the industry. In fact, CAKE has outpaced industry sales for at least the last 18 months. That said, the casual dining industry is currently in secular decline and CAKE is not completely immune to any near-term weakness. This, in addition to a difficult comp in 3Q, could incite some short-term pressure, but we believe the strong likelihood of a rebound in 4Q will allay these fears.

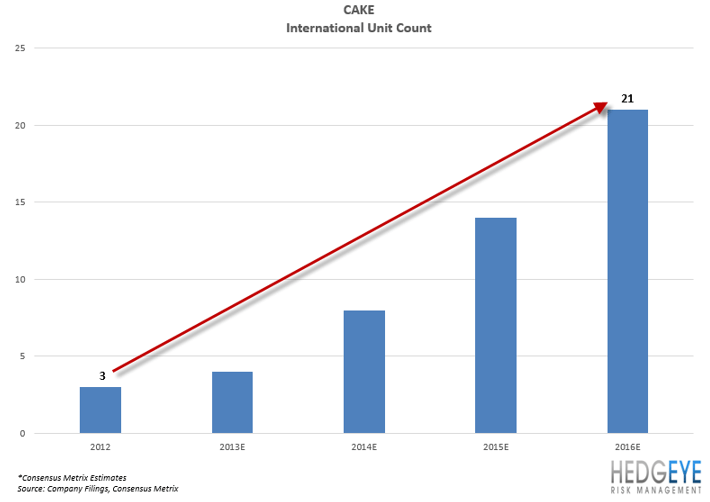

International Expansion

We believe CAKE’s long-term international expansion growth strategy is underappreciated by the street. This is an attractive opportunity for the company and, to date, performance abroad has been stronger than management originally anticipated, leaving the door open for a potential increase in their current expansion plans. Management expects to open one new restaurant in the Middle East this year, driving the total unit count in the region up to four. They have also identified other international sites to add to their pipeline, including site in Mexico City and Latin America. We’ll be looking for a little more color on 2014 international growth plans when the company reports 3Q13 earnings.

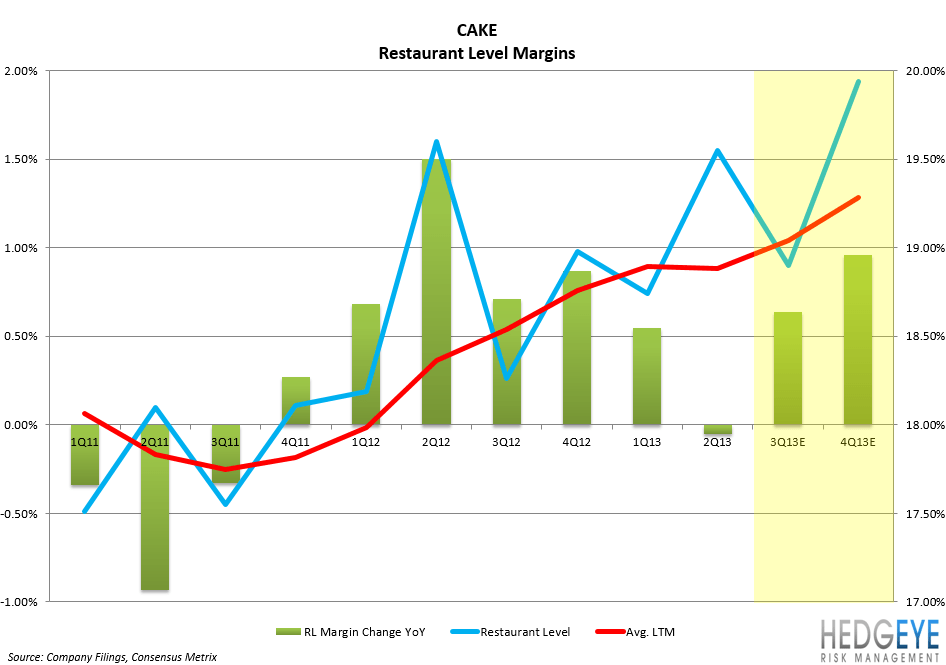

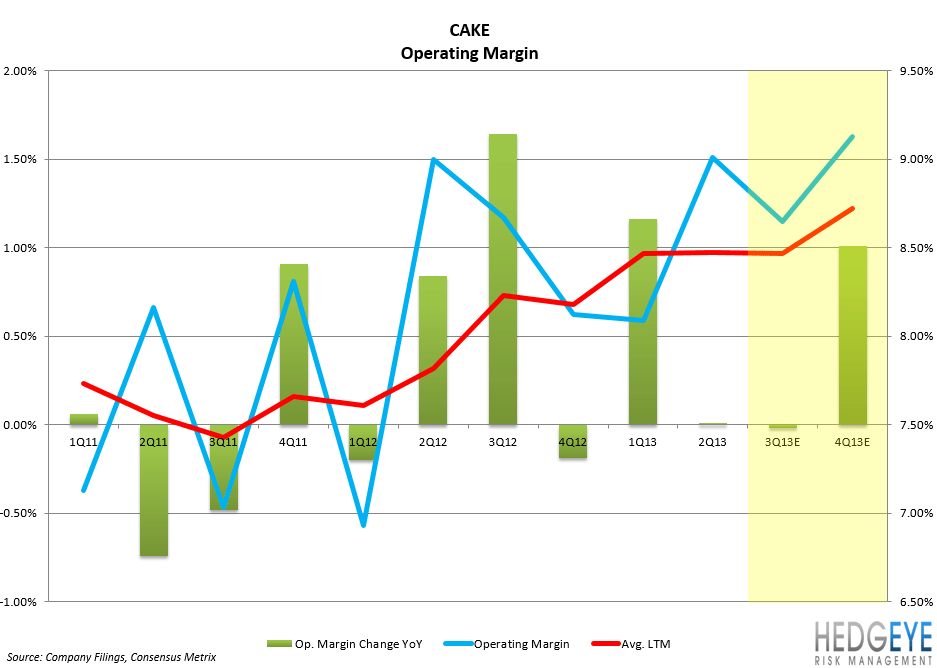

Margins Continue to Improve

Restaurant level and operating margins continue to be points of strength for CAKE. Restaurant level margins, despite ticking down 5 bps in 2Q13, are expected to improve by 64 bps in 3Q13 and another 96 bps in 4Q13. On top of that, operating margins, which ticked up 1 bps in 2Q13, are expected to fall by 2 bps in 3Q13, before improving by 101 bps in 4Q13.

Overall, the company expects operating margins to improve 50 bps over the prior year. Strong restaurant level and operating margins can be mostly attributed to the following:

- Lower expenses – every line item, aside from G&A, is expected to be better than last year

- International expansion – the three Middle East locations have exceeded management’s expectations and continue to deliver impressive volumes

Favorable Food Costs

CAKE should continue to benefit from lower cost of sales due to moderate commodity cost inflation and favorable dairy costs over the prior year.

Financially Robust

CAKE is expected to generate more than $100 million in free cash flow this fiscal year and, despite ongoing international expansion efforts, management continues to reward shareholders. Not only does the company boast a 1.28% dividend yield, but the Board of Directors recently authorized up to $125 million to repurchase shares in the latter half of the year. In aggregate, CAKE is expected to return as much as $200 million to shareholders in fiscal 2013.

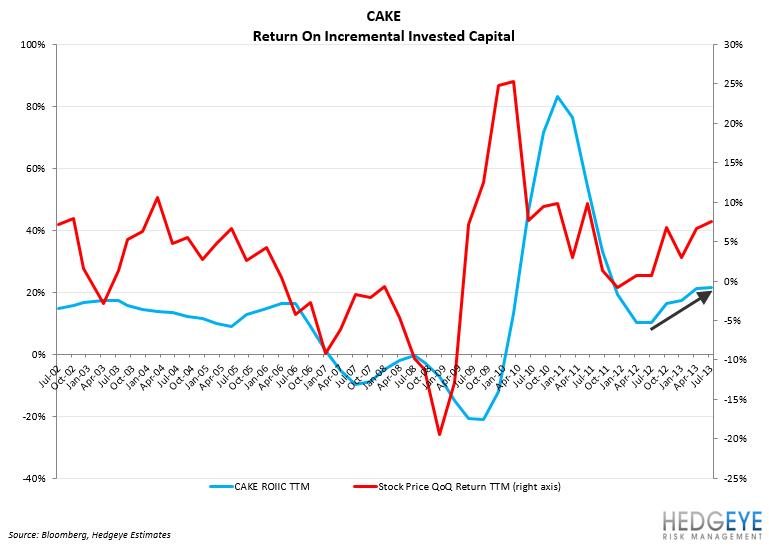

ROIIC Treading Upward

While the majority of metrics analysts look at fall in and out of favor over time, one metric that has outlasted the test of time for every company is also, to no surprise, one of our favorites – Return On Incremental Invest Capital (ROIIC). After an impressive stretch in 2010, CAKE’s ROIIC TTM fell rapidly over the course of 2011, before bottoming out in the middle of 2012. From that point, we have been seeing, and believe we will continue to see, gradual and steady improvement in this trend.

Sentiment

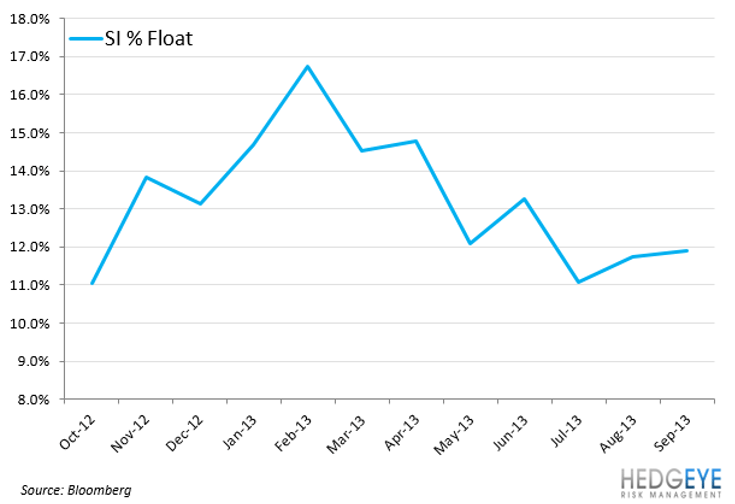

Sentiment on CAKE is very low – yet another reason we continue to like this call. Illustrated in the chart below, 33.3% of analysts rate CAKE a Buy, 63.0% rate CAKE a Hold, and 3.7% rate CAKE a Sell. Furthermore, short interest in the stock is currently 11.90% of the float.

Valuation

At 8.8x EV/EBITDA, CAKE is trading in line with its Casual Dining peer group. We believe this valuation is fair and justified by the company’s international expansion plans, improving ROIIC, and robust financial profile.

Howard Penney

Managing Director