This note was originally published at 8am on September 20, 2013 for Hedgeye subscribers.

“The Fed is the greatest hedge fund in history.”

-Warren Buffett

That’s what Buffett told students at Georgetown University yesterday. He was trumpeting “how much money” the Fed makes: “it’s generating $80 billion or $90 billion a year probably… and that wasn’t the case a few years back.”

Now isn’t that just fantastic. One of the greatest financial minds in US history is now marketing a political message that is about as anti Benjamin Franklin as it gets. Anti-savings that is. Where in God’s good name do you think these said “profits” come from?

They come out of American savings accounts. Even the Fed itself (St. Louis Fed) reminds us that the “growth rate of real GDP has been higher on average when the personal savings rate is rising than when it is falling (Gilder, pg 72).” The Founding Fathers wanted our children to respect their piggy banks, not some un-elected money printer clipping our hard earned coins.

Back to the Global Macro Grind…

As George Gilder goes on to absolutely nail this topic in his new book, Knowledge and Power, “the entrepreneur is the savior of the system because he capitalizes himself. He is his own most important capital… socialists believe their mission is to seize capital for the masses…” (Gilder, pg 77)

That’s what Mr. Buffett should be marketing. It’s time to get our money out of the Fed’s hands and back into the hands of The People. We know how to generate returns. We’re the ones who are going to be doing the hiring when we make money. All the Fed’s “profits” do at this point is tax the American consumer. It’s called Down Dollar driven inflation. It’s regressive.

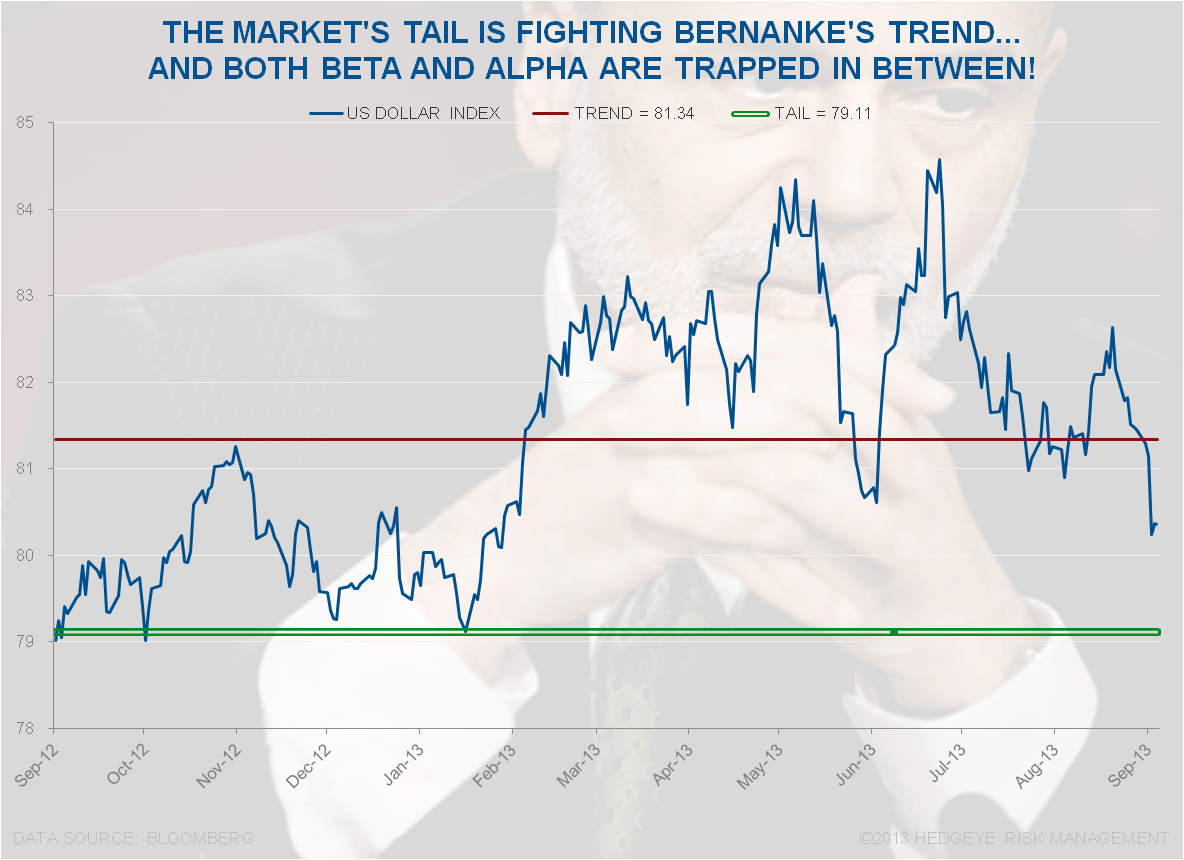

Moving on… where the rubber meets the road here is in terms of the purchasing power of your hard earned currency. While I was disgusted with Bernanke’s decision to debauch the Dollar again this week, that doesn’t mean he’s going to win this war for good. In the last 24 hours, both the data (economic gravity) and Mr. Market are fighting back:

- US Dollar Index is up +0.2% this morning to $80.41 (holding long-term TAIL risk support of $79.11)

- Gold and Silver are down -1% and -2.4%, respectively (both are still bearish TREND and TAIL in our model)

- Oil (Brent) failed to breakout above our immediate-term TRADE resistance line of $110.94/barrel

Economic data? Yes, as in the stuff Bernanke has un-objectively ignored since almost every high-frequency US economic data series we follow started to accelerated in July.

- JOBS: non-seasonally adjusted rolling US Jobless claims hit yet another YTD low (-16.4% y/y) yesterday!

- ORDERS: the Philly Fed’s “New Order” component ripped a +21 SEP vs +5 in AUG

- HOUSING: US Existing Home Sales hit a 6-month high yesterday

Now most Fed apologists (which are mostly those who get paid by A) Government Power and/or B) Down Dollar) will whine about the impact of #RatesRising on the “housing’s recovery” instead of focusing on what really drives housing demand – confidence.

Although US Savings are at generational lows, US Net Worth is currently tracking at an all-time high. We’d argue that’s been largely driven by real (inflation adjusted) #GrowthAccelerating more so than anything else. US Home Prices up +12.4% y/y obviously helps, but the demand for housing won’t be impacted until the 30-yr mortgage rate blows through 6% (it’s at 3.79% today, get over it).

In other words, the greatest threat to US growth recovering is the government intervening in the economic cycle. There has never been a sustained US economic recovery that didn’t coincide with:

1. Strengthening US Dollar

2. Rising US Interest Rates

Why doesn’t every discussion about the Fed start and end with that?

While Buffett might love the impact Bernanke has on his P&L (fat net interest margins are driven by marking the short-end of the curve at 0% - that pays insurance companies (Berkshire) in size), I’d like to remind him that the “greatest hedge fund manager in history” is also the only un-elected central planner in US history to attempt to ban the economic cycle.

What is an economic cycle?

$USD/Interest Rates Higher --> Energy/Commodities/Inflation lower --> Real Consumption Growth Higher --> Pro-Growth Equities Higher

With all due respect Mr. Buffett, why don’t you and your pal, Mr. President, want the rest of us “middle classers” to have that?

Sadly, there are very few leaders in Washington who have my back on this. That’s one of the reasons why I have the highest CASH position in the Hedgeye Asset Allocation Model since July 23rd. I don’t trust this rally to all-time highs anymore.

The biggest thing Bernanke lost this week was whatever was left of the trust I had in someone at the Fed doing the right thing. The timing was perfect. And he chose politics instead. If growth slows from here, Gold help him. Because history won’t.

Our immediate-term Risk Ranges (we have 12 of them in our Daily Risk Range product) are now:

UST 10yr Yield 2.70-2.81%

SPX 1709-1730

VIX 12.91-14.62

USD 80.20-81.25

Brent 107.62-110.94

Gold 1346-1398

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer