The Data Remains Impressive

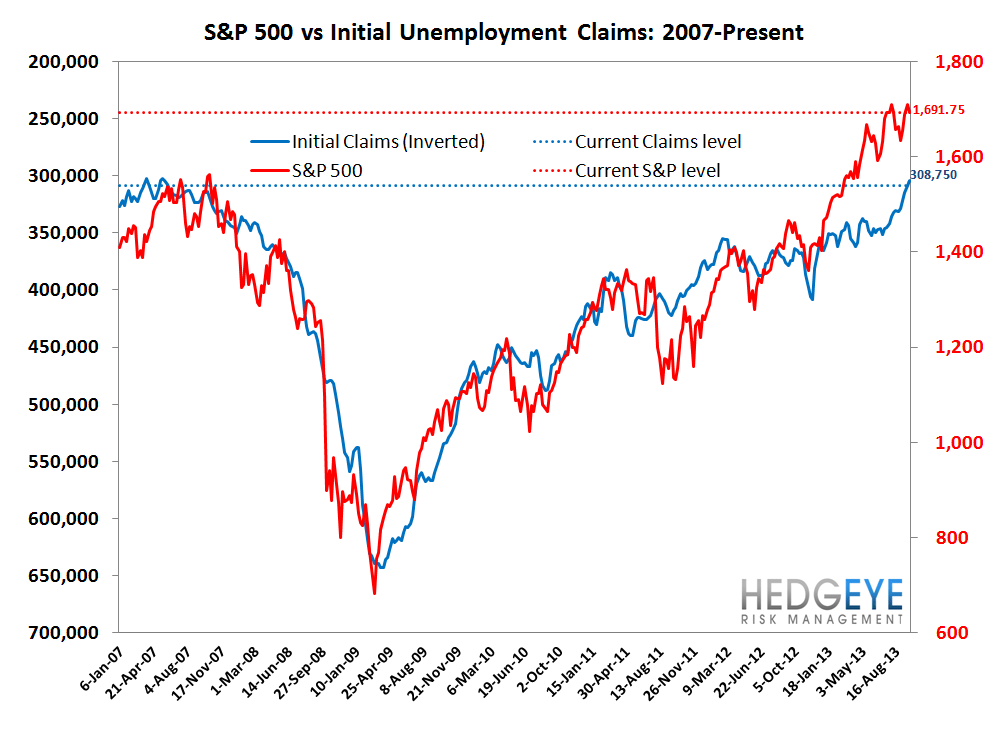

Initial jobless claims are the primary determinant of future delinquencies for unsecured lenders, i.e credit card companies. Typically, job loss accounts for the bulk of net credit losses (~60%) while bankruptcies, driven principally by divorce and unexpected medical bills, account for the balance. Claims also predict delinquencies well in advance, which is why we care. It's notable that rolling YoY NSA claims are now 18.3% lower than at the same point last year, which is the fastest rate of improvement seen YTD and is actually the fastest rate of improvement seen since the first half of 2010. In light of the recent weakness in the XLF we'd be looking at credit card operators on the long side as they are relatively immune from compression in the curve and are major beneficiaries of the enormous improvement in the credit environment.

One thing to note: Federal workers are eligible to collect unemployment while furloughed, so we would expect to see next week's claims print rise. That said, we would expect the uplift to be temporary.

We expect Capital One to print another solid result when they post 3Q earnings, predicated largely on the strength in the labor market. Remember that reserve release is being modeled on these claims numbers.

The Data

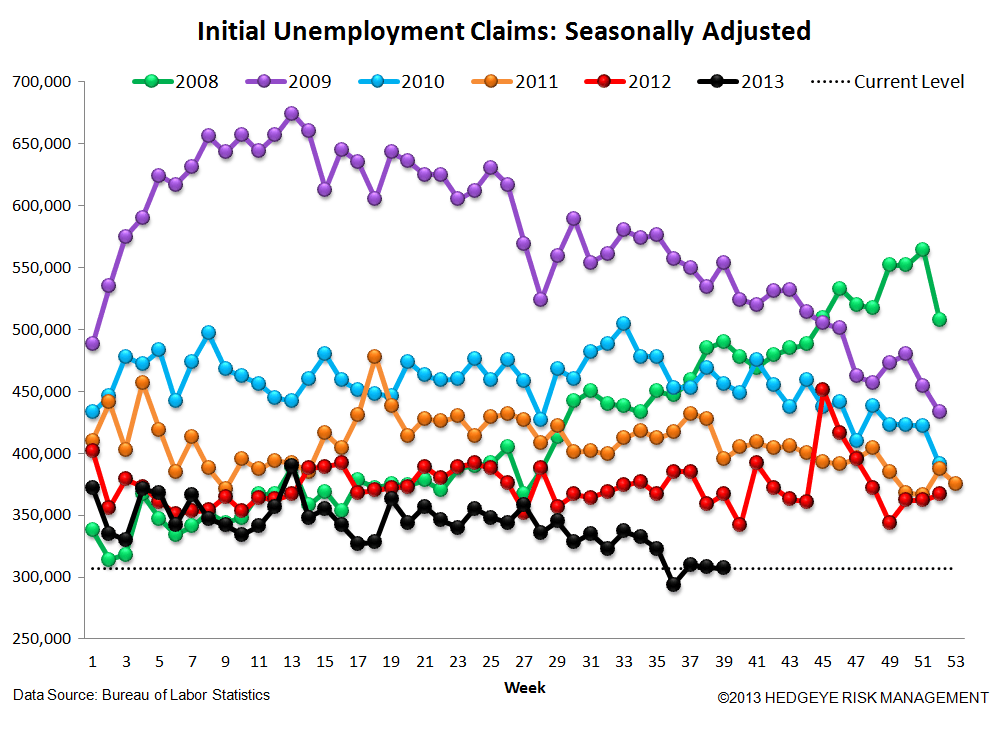

Prior to revision, initial jobless claims fell 2k to 308k from 305k WoW, as the prior week's number was revised up by 2k to 307k.

The headline (unrevised) number shows claims were lower by 1k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -4k WoW to 304.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -18.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -17.5%

Yield Spreads

The 2-10 spread compressed 2 basis points WoW to 229 bps from 231 bps. The third quarter shook out at 230 bps, a major sequential increase (+63 bps) vs 2Q's average of 171 bps. Thus far in the fourth quarter, the yield spread is roughly flat, tracking down 4 bps vs the 3Q average.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT