“If making money is a slow process, losing it is quickly done.”

-Saikaku Ihara

That’s a mint quote at the start of chapter 13 (“Wild Money And The Stealth Tax”) in one of my favorite economic history books, Jack Weatherford’s The History of Money (pg 193). I’d love to hear Bernanke and Obama’s version of this history. Devaluing the purchasing power of The People for political gain is as old as politics itself. It’s called inflation – and it’s a stealth tax.

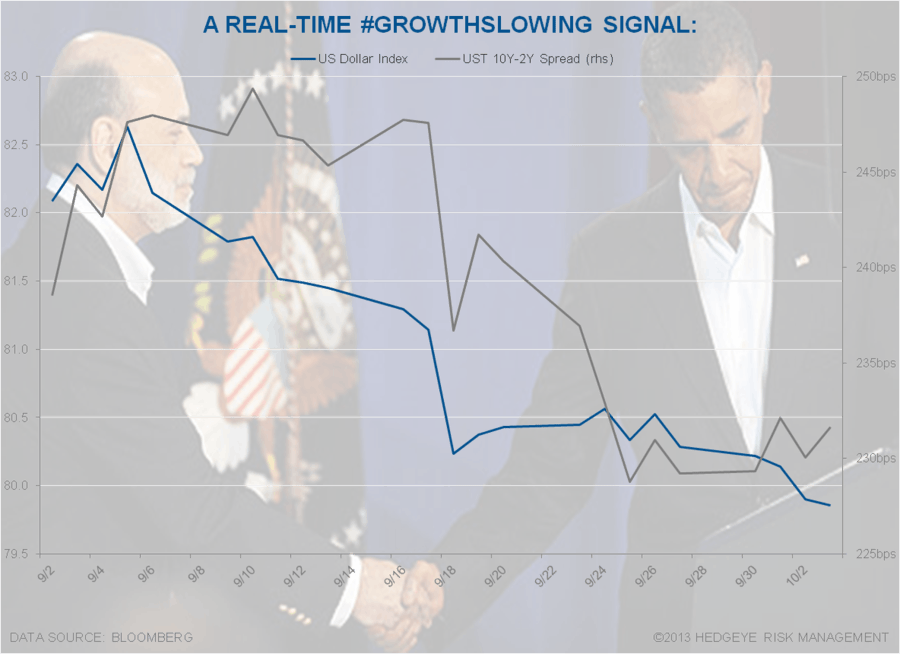

Ex the anti-dog-eat-dog-class-warfare-storytelling, you’ve probably noticed that US politicians are currently burning the credibility of your hard earned currency at the stake (see Chart of The Day). No US President and/or Federal Reserve Chief has overseen A) a lower US Dollar value and/or B) a higher Oil price than Obama and Bernanke. Nice job boys.

No US President has been forced to “shut-down” the government in 17 years either. In order to explain the mechanics of it all, we’ll be hosting a call with the last man to force Big Government’s hand on this, Newt Gingrich, at 11AM EST @Hedgeye today (email if you’d like access – we’ll have a full access client Q&A for Newt too).

Back to the Global Macro Grind…

Simple question: When it comes to the purchasing power (currency) of who Obama labels “ordinary, middle class folks”, doesn’t the buck stop with the President of The United States?

As Obama pointed out yesterday in an interview with raging Republican, John Harwood, the appointment of Bernanke was as important as any he’s made. So, doesn’t that make The President accountable to empowering a Burning Buck policy?

Silly questions, I’m sure. That’s why CNBC didn’t get me to do the interview.

In other news, the US stock market is now down for 9 of 11 days since Ben Bernanke arbitrarily decided to do precisely the opposite of what he was “communicating” to the marketplace (taper).

Counter to consensus thinking, the better part of this recent correction in stocks has come on days when:

- US Dollar is DOWN, and

- US Interest Rates are DOWN

The causal factor in driving Down Dollar has been a two track (monetary and fiscal) political strategy that is starting to look like an idea that came out of a Roman bath club circa 52 BC. Plunder the people for political gain. They won’t understand. #stealth

With the US Dollar having given back all of its YTD gains (it’s down -2.7% in the last month):

- The US Dollar Index now has a 6-week POSITIVE correlation of +0.95 to the 10yr US Treasury Yield

- And the USD has a 6-week POSITIVE correlation of +0.82 to the US Treasury 10Y-2Y Yield Spread

Just because you won’t get things like leading indicators from your President or the US Federal Reserve doesn’t mean they cease to exist:

- Down Dollar and Down Interest Rates are starting to = Down Stock Market

- Down Dollar and Down Interest Rates = a leading indicator for #GrowthSlowing

If this sounds familiar to you, it should – this is basically the inverse of our call for the last 10 months. We were bullish on US GDP #GrowthAccelerating because two of the most obvious leading indicators for growth (#StrongDollar + #RatesRising) had both #OldWall Street and Washington consensus chasing the rising growth expectations.

From a S&P Sector perspective, the easiest way to summarize growth expectations slowing is via the Financials (XLF). The reason why the 10Y minus 2Y Yield Spread matters is because this is how a bank makes money. As the long-end of the curve (interest rates) falls, banks make less of a margin and can then lend less. How’s that for “ordinary folks”?

While almost every said “economics” guru advising Obama will tell him that a “weak Dollar is good for manufacturing and exports”, that’s the biggest crock since Nero started devaluing The People’s currency in the first place. Let’s look at what just happened in a country whose currency was lit on fire earlier this year (and whose stock market was crashing, in kind) – Brazil:

- Brazil finally said enough is enough, and RAISED rates to defend its currency (the Real)

- Brazilian Real is now +7.8% in the last month versus USD; Brazilian Stocks (Bovespa)= +17.9% in the last 3 months

- Brazil’s SEP economic data (both manufacturing PMI and Exports) accelerated as its currency did (Exports +5% y/y SEP)

Yep. Them be the facts, “folks.” And if you want to re-gain the trust of The People, you better start talking #truth. Politically preying on the ignorance of “ordinary” people is un-American. Losing respect like the US Dollar has happens slowly, then all at once.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.58-2.73%

SPX 1

Nikkei 134

VIX 14.86-17.39

USD 79.21-80.42

Euro 1.34-1.36

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer