Investment Company Institute Mutual Fund Data and ETF Money Flow:

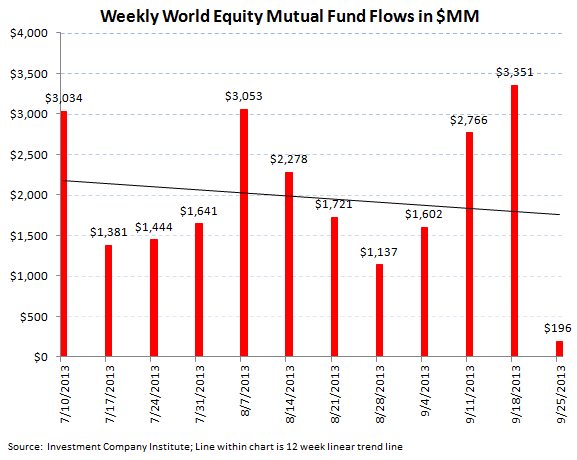

Equity mutual funds booked an outflow of $3.5 billion for the 5 day period ending September 25th, a reversal from the $3.3 billion inflow the week prior

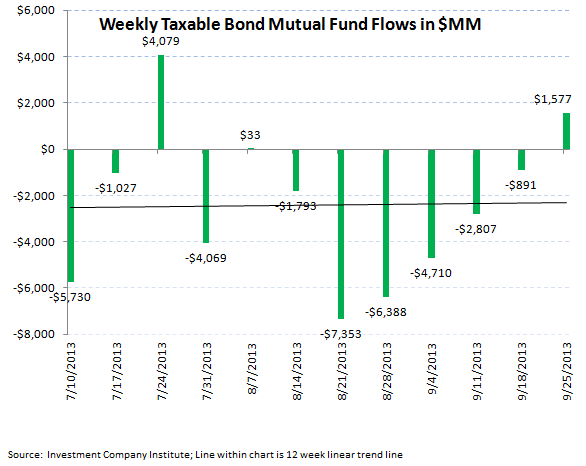

Fixed income mutual funds flow improved sequentially W-o-W and resulted in a $1.2 billion inflow, a reversal from the $2.6 billion outflow last week

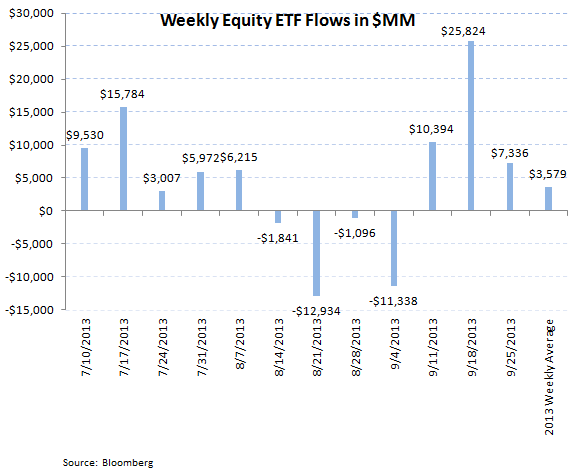

Within ETFs, passive equity products experienced another large inflow with $7.3 billion coming into the equity category. Bond ETFs also had positive trends, with a $1.3 billion inflow in the most recent weekly period

Within our Hedgeye Asset Management Thought of the Week below, we highlight that despite the short term weekly rebound in bond fund flows in the most recent 5 day period that 2013's year-to-date trends reflect a substantial asset allocation shift from bonds and into equities

For the week ending September 25th, the Investment Company Institute reported the first weekly outflow in combined domestic and world stock funds in 4 weeks and the first inflow for combined taxable and tax free bond funds in 9 weeks. Total equity fund flow totaled a $3.5 billion outflow which broke out to a $196 million inflow into international equity products and a $3.7 billion outflow in domestic stock funds. These trends decelerated from the prior week's total equity fund inflow of $3.3 billion and the outflow in domestic stock funds was the largest since the first week in May. Despite this weak 5 day period for stock fund flows, the year-to-date weekly average for 2013 now sits at a $2.5 billion inflow for total equity mutual funds, a substantial improvement from the $3.0 billion outflow averaged per week in 2012.

On the fixed income side, bond funds showed some fighting spirit for the week ending September 25th with the aggregate of taxable and tax-free bond funds booking a $1.2 billion subscription, the first combined inflow in 9 weeks. The taxable bond category lead the charge with a $1.5 billion inflow, which washed over the $289 million outflow for tax-free or municipal bonds. While the slight inflow in the most recent period is encouraging for the bond market, the 2013 weekly average for fixed income fund flow has still drastically declined from 2012, now averaging a $474 million weekly outflow this year, a far cry from the $5.8 billion weekly inflow averaged last year.

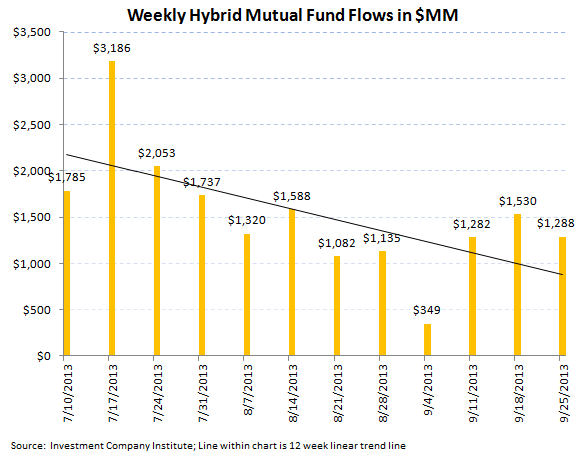

Hybrid funds, or products that combine both fixed income and equity allocation, continue to be the most stable category bringing in another $1.2 billion in the most recent weekly period, an slight decline from the $1.5 billion inflow the week prior. The year-to-date weekly average inflow for hybrid products is now $1.6 billion for '13, almost a 100% increase from 2012's $911 million weekly average.

Passive Products:

Exchange traded funds experienced positive trends in both equities and fixed income for the week ending September 25th. Equity ETFs gathered up $7.3 billion in investor funds, another strong week off of the back of the $25 billion inflow last week. Including this week's production, 2013 weekly average equity ETF trends are averaging a $3.6 billion weekly inflow, an improvement from last year's $2.2 billion weekly inflow average.

Bond ETFs also had a positive week with a $1.3 billion inflow, which was an improvement from last week's $850 million subscription. Including this improved weekly flow within passive bond products, the 2013 weekly bond ETF average is flagging at just a $413 million inflow for bond ETFs, much lower than the $1.0 billion average weekly inflow from 2012.

HEDGEYE Asset Management Thought of the Week - Year-to-Date Trends Reflect Rotation from Bonds and into Stocks:

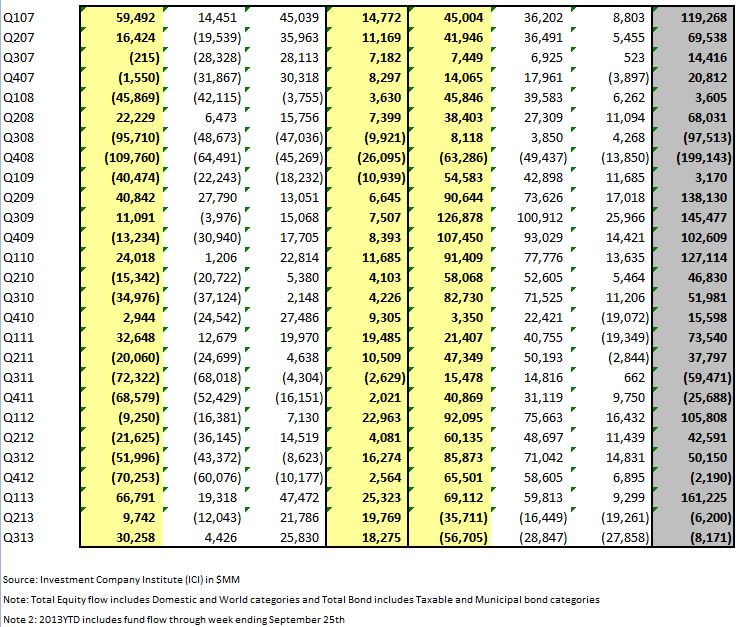

With the third quarter of 2013 essentially in the books (although the ICI fund flow data is only through September 25th of this year), a longer term perspective of mutual fund flow and also ETF subscriptions relays an investable shift from fixed income and into stocks. First looking at the ICI mutual fund data, shows the first combined total equity inflow (combining both domestic and world funds) since 2007 of $106 billion and the current running $11 billion inflow into domestic stock funds is the first positive year in U.S. stock fund flow since 2006. World equity fund flow of $95 billion thus far in 2013 is also the best year since '07 but it is unlikely with just 1 quarter left this year that the appetite for foreign stock funds will surpass the $139 billion record from '07. Hybrid mutual fund products however have already well surpassed last year's record production of $45 billion in inflow and thus 2013 has been a break out year for products with both stock and bond allocations. On the fixed income side, the combination of a slight $14 billion inflow in taxable products is being overwhelmed by the $37 billion outflow in tax-free or municipal products. Thus the combined net outflow of $23 billion is well off of the $303 billion net inflow from 2012 and a far cry from the all time record year of $379 billion in net inflow from 2009. This year's running bond outflow is the first annual withdrawal from the asset class since 2004 according to the ICI.

From a quarterly perspective, the net inflow for 3Q13 into equities is continuing the good start to the year experienced in 1Q for both domestic and world stock fund products. The net outflow of $56 billion in bonds (a combination of $28 billion in taxable funds and the $27 billion which came out of municipal bonds) was the worst quarterly outflow since the Financial Crisis in 4Q 2008. While the prospective outlook for bond fund flows will in large part be driven by the communication from the U.S. central bank on ongoing quantitative easing, we note that in our recent launch of the asset management sector we outlined a potential $1 trillion shift between the stock and bond asset classes if the outstanding capital stock percentages within equities and fixed income normalizes. Our research on this topic can be found here. Within passive ETF products, the 2013 year-to-date perspective is showing another record year for equity ETFs with a $129 billion inflow brewing currently. This is on top of the prior record of $117 billion from last year in 2012. The weakness in fixed income is also being picked up in passive fixed income products with just a $15 billion inflow thus far in the first 3 quarters of '13, a substantial decline from the record bond ETF inflow last year which produced over $56 billion in net investor subscriptions. With the ongoing reallocation out of gold, commodity ETFs namely the GLD have produced sharp outflows for 2013. In the first 3 quarters of this year, commodity ETFs have seen over $20 billion withdrawn from the category, the only negative annual period within Bloomberg ETF data. With this asset allocation shift from fixed income and into equities we continue to relay our best ideas in the asset management sector as T Rowe Price (TROW) on the long side to capture nascent equity fund flow and that we would avoid or short shares of Franklin Resources (BEN) with a large exposure to declining bond fund trends.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA