This note was originally published at 8am on September 17, 2013 for Hedgeye subscribers.

“The great thing about fact based decision is that they over rule the hierarchy.”

-Jeff Bezos

Jeff Bezos knows a thing or two about making decisions. In 1994 after making a cross country drive from New York to Seattle, he made the decision to write up a business plan. To undertake this cross country drive, he made a decision to leave a “well-paying” job. The little company that Bezos was developing a business plan for was Amazon.com and the rest, as they say, is history.

At the time, Bezos combined two facts that helped him overcome the establishment. The first was that the internet was growing in leaps and bounds. The second fact was that the U.S. Supreme Court had ruled (in Quill Corp V. North Dakota) that online retailers would not have to collect sales taxes in states where they lacked a physical presence.

This series of decisions paid off handsomely for Bezos as he is now worth an estimated $25.2 billion. Meanwhile his company Amazon.com has a market capitalization of more than $135 billion and generates more than $65 billion in annual revenues. Frankly, it kind of makes me want to quit my job and go for a drive!

Former Harvard President Larry Summers made a big decision late Sunday to withdraw his name from consideration to replace current Federal Reserve Chairman Ben Bernanke. Now technically speaking, the fact that five Democrats intended to vote against him in committee kind of forced his hand, but nonetheless a decision was made.

In the short run, Mr. Market viewed this development as somewhat positive as stocks were up broadly with the SP500 up 0.57%. (Strangely, the bell weather master limited partnership, Kinder Morgan Partner (KMP), underperformed and was down -1.50%.) President Obama then chose to come out and spoil the Wall Street party as Obama indicated he will not negotiate an extension of the U.S. debt ceiling as part of the budget fight.

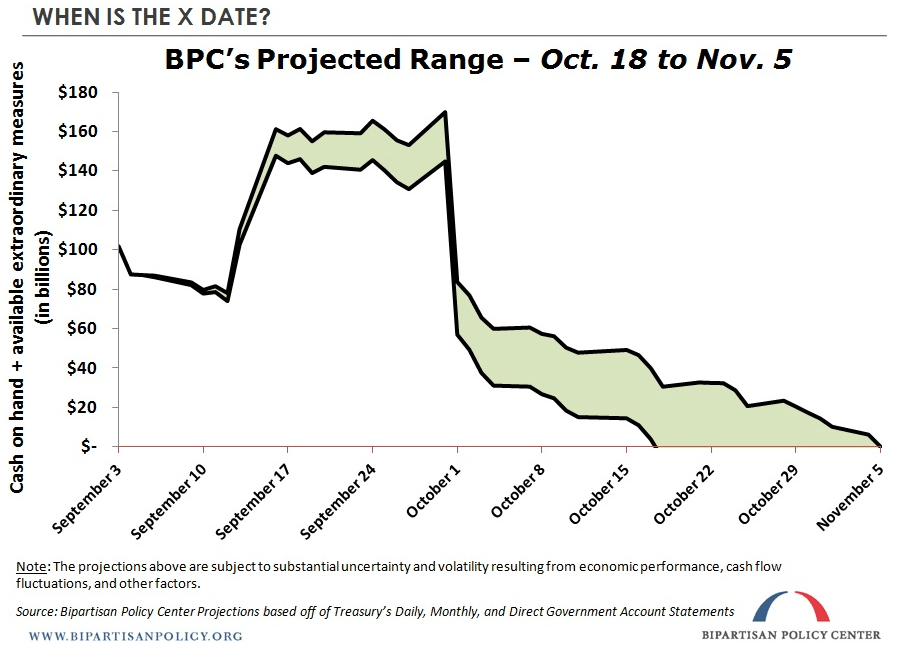

Slight digression, yes the debt ceiling debate is looming again. As Yogi Berra said, this is déjà vu all over again. You may recall, in 2011 Congress raised the debt ceiling to $16.7 trillion, an increase of over $2 trillion. Currently, based on projections from the Treasury department, the federal government could hit the debt ceiling as soon as mid-October.

In the chart of the day, we highlight a chart from the Bipartisan Policy Center that shows that the debt ceiling is likely to be breached to between October 18th to November 5th. Technically speaking, the United States hit its debt limit on May 19th, but as my colleague Christian Drake has written about, via a number of extraordinary measures, the ceiling has been extended, but these measures will run out at some point in the time frame noted above at which point the federal government will only have enough tax revenue to cover about 68% of its bills.

Incidentally, and for those that don’t have their calendars in front of them, the “X-date” is just over a month away. And just think, most investors are worried about who is going to be the next Chairman / Chairperson of the Federal Reserve! Given the uncertainty around the direction of policy, a looming fiscal crisis, and the fact that U.S. equities have performed quite well in the year-to-date, it should be no surprise that some savvy investors like Stan Druckenmiller are indicating they are largely underinvested.

We certainly get the risks, but one point that has and will continue to benefit equities, is bond outflows. Since May we have seen $116 billion fixed income fund outflows, which is the largest absolute bond outflow in history.

Interestingly though, as our Financials team pointed out yesterday, as a percentage of beginning fixed income assets-under-management, the current 2013 draw down is the smallest in history on a percentage basis. The 2013 running outflow has been just 2.9% of outstanding bond funds, well below the past outflows in 2003-2004 where 5.0% of outstanding bond funds were redeemed and the 14% of bond funds that were drawn down in the 1994-1995 outflow. So while there are certainly risks looking for equities, the continuation of bond outflows will be a meaningful tailwind.

Nonetheless, many of the large investors we speak with remain focused, and rightfully so, on the direction of leadership at the Fed. Given this focus, I thought I’d highlight a few fun facts about the Fed:

1) The greatest long term period of economic growth in the United States was between the Civil War and 1913 when there was no Fed.

2) Prior to the creation of the Federal Reserve, the estimated rate of inflation in the United States was 0.5% and it is estimated to be at 3.5% in the ensuing century.

3) The permanent income tax was introduced in the same year as the Federal Reserve.

4) In 1913, Congress promised that if the Federal Reserve Act was passed it would eliminate the business cycle.

5) The value of the U.S. dollar has declined, by some estimates by more than 95% since the Fed was created.

6) There have been 10 recessions since 1950 (arguably many Fed induced).

I borrowed some of these points above from a blog called End of the American dream and, as we touched up on in the past, it kind of begs the question, as Bezos would say, as to whether the best fact based decision is to overrule the Federal Reserve hierarchy in its entirety. Based on the points above, ending the Fed wouldn’t be the worst decision the Federal Government ever made.

Our immediate-term Macro Risk Ranges are now as follows:

UST 10yr Yield 2.80-2.98%

SPX 1675-1709

VIX 13.33-14.98

USD 80.89-81.75

Euro 1.32-1.34

Gold 1301-1361

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research