We’re not big into “maintenance” research at Hedgeye but, at the same time, contextualizing marginal macro changes (i.e. the ones that matter) requires continually grinding through the incremental big picture data points.

This morning’s Consumer Spending and Income data and Tuesday’s 2Q13 Flow of Funds data from the Fed aren’t particularly actionable from an investment perspective, but they are worth a quick highlight.

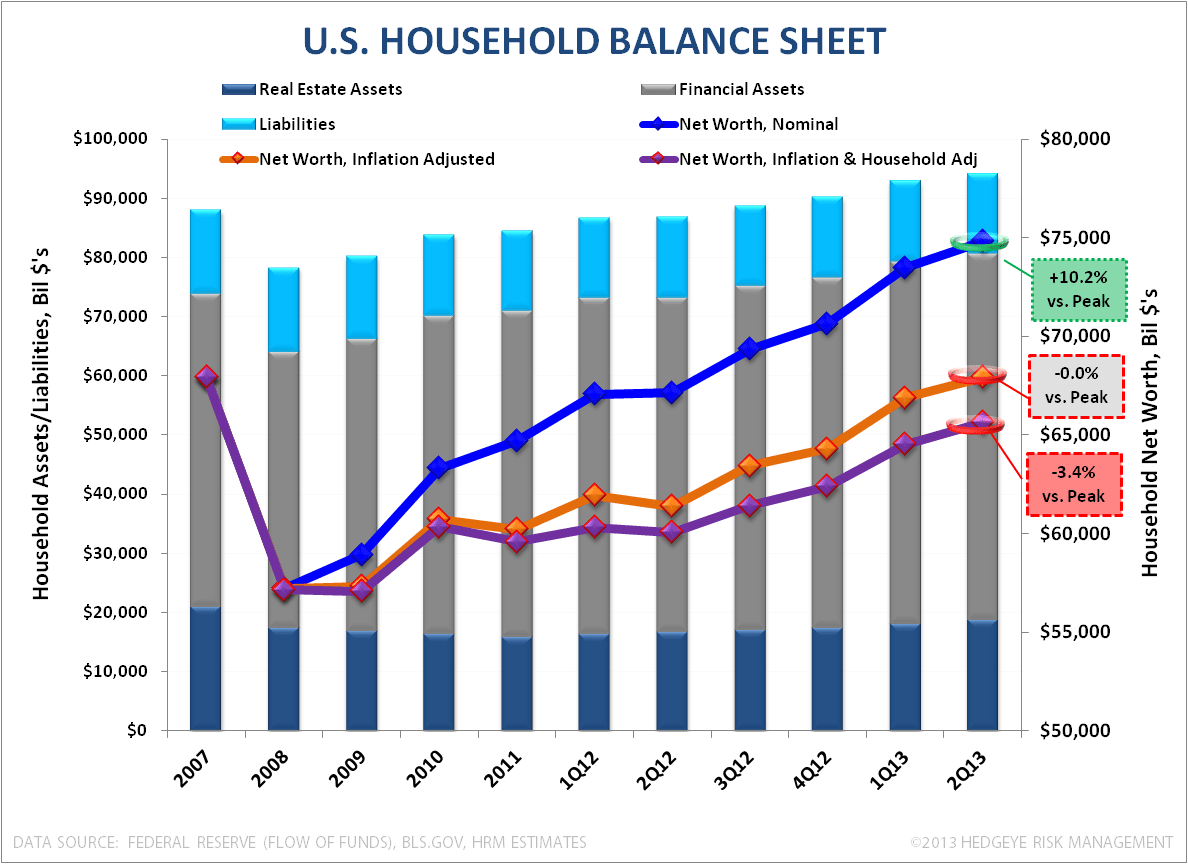

Below is an updated snapshot of the U.S. Household Balance Sheet from the latest Flow of Funds report from the Federal Reserve. The continued improvement in Household Net wealth shouldn’t come as a surprise given the lack of aggregate household credit growth and the ongoing re-flation in real estate and financial asset prices.

As of the end of 2Q13, Household Net Wealth is well above the prior 2007 peak on a nominal basis, flat on an inflation adjusted basis and -3.4% vs prior highs after adjusting for both inflation and the number of households (ie. inflation adjusted net worth per household).

Household real estate values, currently at $18.6T (21% of total assets), grew at a rate of +11.9% YoY and remained a primary driver of net wealth gains in 2Q13. We continue to expect positive growth in property values, albeit a slower rate of improvement than we’ve observed over the TTM, to support further balance sheet improvement over the intermediate and longer-term.

Putting aside the disproportionate benefit and wealth equality implications stemming from financial asset price inflation, ongoing strengthening in the aggregate household balance sheet remains an obvious positive as we continue to emerge on the other side of a long-term, domestic credit cycle.

Consumer Income & Spending: Upside Still Constrained

Today’s preliminary estimates from the BEA showed Personal Income grew 0.4% MoM in August while Consumer Spending advanced +0.3% alongside a tick higher in the Savings Rate to 4.6% from 4.5% in July.

On the income side, personal and disposable income growth accelerated on both a MoM and YoY basis while Government sourced income (~17% of the Workforce) remained a discrete drag on DPI growth.

On the spending side, consumption of Non-durables decelerated on both a MoM and YoY basis (after accelerating last month) while spending on Services and Durables both accelerated sequentially (after decelerating last month).

From a multi-month Trend perspective, accelerating spending on goods has helped offset a modest deceleration in consumption of services. (see table below for a detailed breakdown).

Inflation remained muted with core PCE – the key measure for the Fed – mired at 1.2% growth.

Summarily, Personal Income accelerated sequentially but with the savings rate rising and compensation of government employees still growing negatively (due to ongoing job loss and the negative income effects from furloughs – see Here for a fuller discussion) consumer spending growth remained middling.

The confluence of smallish credit growth, a static savings rate and a fiscal policy related drag on (already muted) income growth should serve to constrain the upside in consumption growth nearer term.

Enjoy the weekend.

Christian B. Drake

Senior Analyst