We Think It Makes Sense to Step Aside For Now

We have been consistently bullish on Nationstar Mortgage since adding it to Hedgeye's Best Ideas list back on February 27, 2013 at a price of $38-39. The stock has had a good run since then, recently trading in the $56-57 range, but today many of the themes and catalysts we thought were misunderstood earlier in the year have either come to pass or are now far better understood and priced in. Consequently, we think most of the good news is now reflected in the valuation. Consider that in just the last few weeks there have been at least two positive initiation reports and one upgrade of the stock from the sell side. In fact, there are currently 8 buy ratings on the stock, more than at any other point in the company's history.

We expect there will likely be near-term positive catalysts in the form of deal announcements. Inside Mortgage Finance has written that sizeable MSR transactions are to be expected in the near-term from Wells Fargo ($40 Bn), JPMorgan ($70 Bn) and, most recently, Citi ($61 Bn). Recall that in their second quarter earnings release, Nationstar bumped up its guided pipeline for bulk deals by $100bn, or roughly in line with the sum of the reported WFC & JPM deals. Clearly, there is high probability, but also high expectations, that NSM will win a large share of those big deals. We wouldn't be surprised to see the stock rally further on such announcements. Historically, deal announcements have been a catalyst for upside as they often led to upward guidance/estimate revisions, not just for NSM but for peer companies OCN and WAC as well.

So, Why the Change?

We have always regarded three dynamics as paramount for NSM shares to move higher: Growing UPB, Improving Servicing Margins and Maintaining GOS. We think the company has delivered on all three fronts to date, and we are not concerned with the progress being made toward the first two dynamics. It's the third one that worries us.

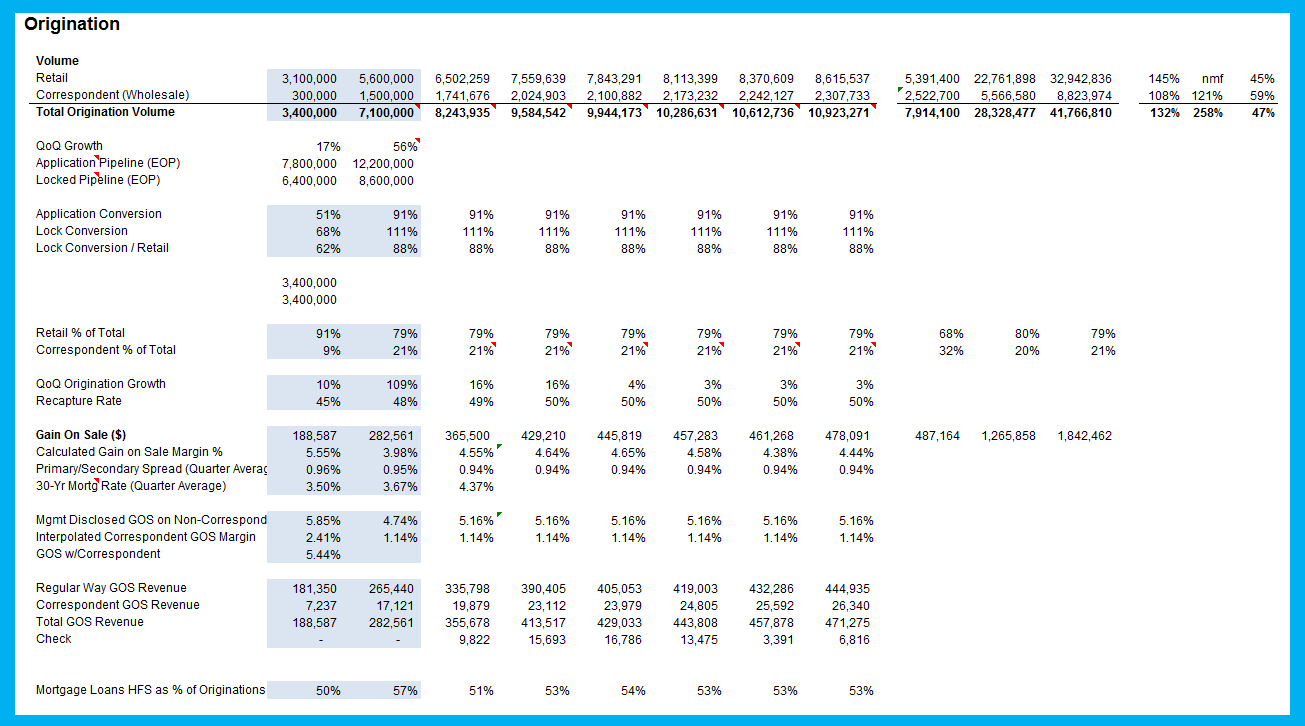

Our primary concern, and the reason for our change in view, is our expectation that Nationstar will struggle to beat estimates going forward due to pressure on both volume and gain-on-sale margins in the mortgage origination business. After spending considerable time working with our model, we are now currently expecting $1.14 in 3Q13 earnings, which is down from our prior expectation of $1.72 and is now below Street expectations for $1.27. Further, we have baked 15 bp sequential quarterly increases into our expectations for long term interest rates throughout 2014 and this has had a profoundly negative effect on our outlook for next year's earnings power. Based on that bump up in rate expectations, we're now expecting NSM to earn $5.37 in 2014, down from our previous expectation for $8.30-9.35. You may find yourself at odds with our assumption of rising rates throughout 2014, particularly in light of the Fed's recent pronouncements and Summers' withdrawal from consideration. Our basis rests upon the strengthening labor market data we track in the initial jobless claims series, which we think will exert growing pressure on prices and, in turn, should pressure the Fed to begin to constrict credit.

HARP & Non-HARP

We've assumed that HARP volumes are relatively unaffected by the rate change. The guidance is for half of 2013's core production target of $23 billion to be HARP, or roughly $11.5 billion. In the first half of the year, we estimate the company originated $4.5 billion in HARP loans, leaving $7 billion in production for the back half of the year. We've split this evenly at $3.5 billion per quarter. However, the remaining non-HARP origination business we have haircut by 40% vs. our prior baseline forecast. Multiple datapoints support the appropriateness of such a haircut. Cardinal Financial recently pre-announced the quarter citing a 40% drop in Q/Q mortgage origination volume (both purchase & refi) coupled with material compression in gain-on-sale margins. MBA volumes 3QTD are down Q/Q by 47% for refi and purchase volumes are down 9% 3QTD vs 2Q13. Given that most of NSM's volume is refi-based, we think a 40% haircut outside of the HARP channel is reasonable.

Gain-On-Sale

We've also assumed gain-on-sale margin pressure. Here's the comment management made on the 2Q13 earnings call, hosted in early August: "With the recent rise in interest rates, we've seen some pressure on market pricing, mainly in the premiums on HARP originations." Generally speaking, HARP loans fetch a 250-500 bps GOS premium to non-HARP loans based on a December 2012 Fed study, which can be found here: Fed Study. Taking the mid-point of the 250-500 bps premium, we estimate that last quarter HARP GOS revenue accounted for roughly 60% of total GOS revenue while only accounting for 38% of volume. The average 30-Year FRM rose to 4.45% thus far in the third quarter, up from the 2Q13 average of 3.67%. That 75-80 bps Q/Q increase in rates is likely to weigh heavily on HARP premiums. Remember, HARP loans fetch a smaller premium in a rising rate environment as traditional loans become more valuable. We've nevertheless been conservative in our treatment and assumed roughly a 25 bps decline in Q/Q total GOS margins.

Based on the combination of these factors, reduced volume vs. prior baseline and lower GOS margins, we've lowered our expectation for GOS revenue to $288mn in 3Q down from our prior thinking of $365mn. While management has indicated that they can and likely will bring some further efficiency to the cost side of this business, we doubt it will be enough to offset the compressed volumes and spreads especially considering the magnitude of efficiency improvement seen in 2Q13. #ToughComps

In short, while we think the long-term opportunity in the servicing business remains attractive, we think expectations are already high on that front without sufficient deference being paid to the pressure on the originations business. We would sell Nationstar at these levels and consider an alternative without heavy origination exposure, like Ocwen.

Ocwen (OCN) as an Alternative

We think it makes sense to roll out of Nationstar and into Ocwen, ticker OCN, where investors can still benefit from the secular trend in servicing but without the significant risk to the GOS business.

Our expectation is that 3Q13 earnings from NSM will disappoint and likely will serve as a catalyst for a rotation out of NSM and into OCN.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT