Quick-hit update: still not much to like about MKC

Today’s Q3 2013 release was very much an extension of last quarter’s call:

- The quarter did arrest the last 5 straight quarters of revenue declines with sales growing at +4%, versus +1.9% last quarter, but 3% of it was driven by its acquisition of Wuhan Asia Pacific Condiments (WAPC) in May 2013

- The company expects to deliver +7% sales and eps next quarter, which we think is a stretch (despite an easier Hurricane Sandy comp)

- We expect the weakness that management cited in quick service restaurants (QSR) and geographically in China and USA, and a lagging industrial business to continue into year-end despite slight offsets as we move into a heavier buying season around the holidays and an increased $10MM marketing spend

- Our macro call is that Bernanke is pulling the confidence cord in issuing his “no taper” call which we expect will translate to subdued confidence into year end. With Europe seeing only slight improvement off of low levels, China still at depressed levels (compared to recent year comps) and slowing, and Latin America (mostly Mexico for MKC) a mixed picture, we’re not comfortable that the macro will be playing at MKC’s back

- Also, spice consumers remain very sensitive to price and typically purchase last minute: the company has not taken up price (or perhaps been willing to) in 2 years. It is planning to implement a 3 cent price increase next quarter – we’ll have to see how the consumer reacts

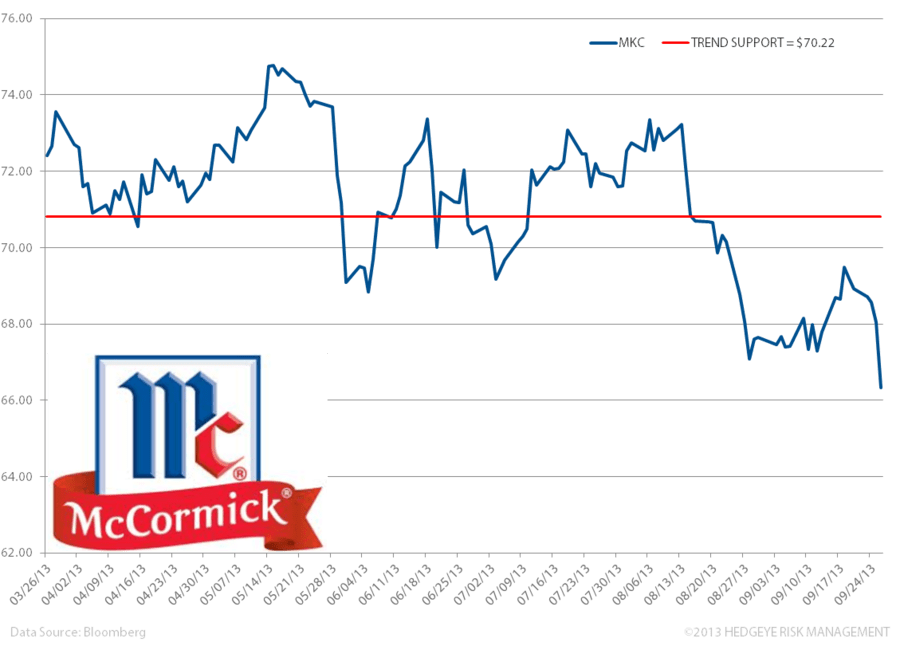

- The stock has underperformed its peer group over recent months, and we don’t expect this trend to inflect. We’ll let the chart below of our levels on MKC do the talking: it is bearish over its immediate term TREND:

Matt Hedrick