Investment Company Institute Mutual Fund Data and ETF Money Flow:

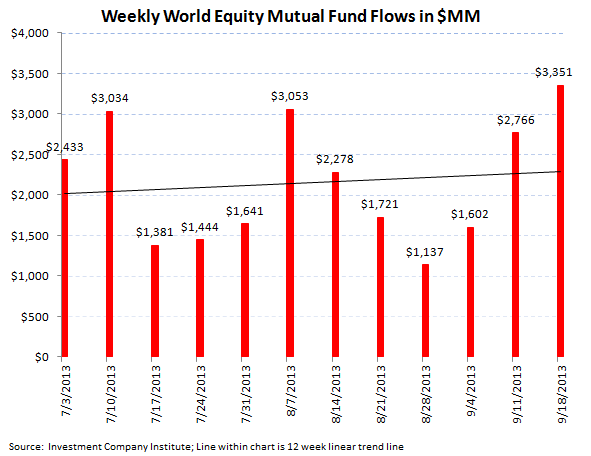

Equity mutual fund inflow decelerated week-to-week to $3.4 billion for the 5 day period ending September 18th, down from the $5.2 billion inflow the week prior but remained well above last year's weekly average

Fixed income mutual fund outflows improved sequentially W-o-W but still resulted in a $2.6 billion withdrawal by investors, an improvement from the $6.7 billion draw down last week

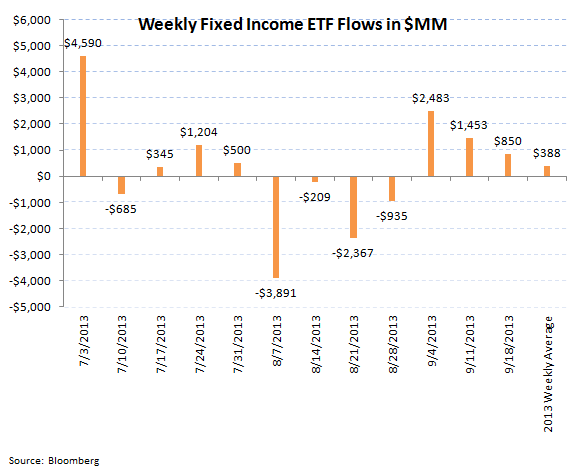

Within ETFs, passive equity products experienced the largest weekly inflow in at least 2 years, with $25.8 billion coming into the equity category. Bond ETFs also had positive trends, although on a much smaller scale, with an $850 million inflow in the most recent weekly period

For the week ending September 18th, the Investment Company Institute reported a deceleration in equity fund flow trends although with fund flow still positive for stocks and an improvement in fixed income mutual fund flows, however with bond trends simply booking a smaller outflow. Total equity fund flow totaled a $3.4 billion inflow which broke out to a $3.3 billion inflow into international equity products and a $44 million inflow in domestic stock funds. These trends decelerated from the prior week's total equity fund inflow of $5.2 billion. Despite this slow down in stock fund flows, the year-to-date weekly average for 2013 now sits at a $2.6 billion inflow for total equity mutual funds, a substantial improvement from the $3.0 billion outflow averaged per week in 2012.

On the fixed income side, outflow trends continued for the week ending September 18th with the aggregate of taxable and tax-free bond funds combining to lose $2.6 billion in fund flow. The taxable bond category specifically shed nearly $900 million, the smallest weekly outflow in 6 weeks and a vast improvement from the $2.8 billion loss last week. Tax-free or municipal bonds continued their sharp outflow trends losing another $1.7 billion in the week ending September 18th, an improvement from last week's $2.7 billion outflow but none-the-less the 11th consecutive week over the $1.5 billion outflow mark. Franklin Resources (BEN) continues to have the most exposure in our coverage group to declining Municipal bond trends with over 10% of its assets-under-management in the tax-free category. The 2013 weekly average for fixed income fund flow has now drastically declined from 2012, now averaging a $521 million weekly outflow this year, a far cry from the $5.8 billion weekly inflow averaged last year.

Hybrid funds, or products that combine both fixed income and equity allocation, continue to be the most stable category bringing in another $1.5 billion in the most recent weekly period, an improvement from the $1.2 billion inflow the week prior. The year-to-date weekly average inflow for hybrid products is now $1.6 billion for '13, almost a 100% increase from 2012's $911 million weekly average.

Passive Products - Largest Weekly Equity ETF Inflow In Our Dataset:

Exchange traded funds experienced wildly positive trends on the equity side and mildly positive trends in fixed income for the week ending September 18th. Equity ETFs gained $25.8 billion, the biggest weekly inflow in our data set with balanced inflow into international, sector focused, and large-cap products. Including this week's inflow, 2013 weekly average equity ETF trends are averaging a $3.4 billion weekly inflow, an improvement from last year's $2.2 billion weekly inflow average.

Bond ETFs also had a mildly positive week with an $850 million inflow, which was a slight decline from last week's $1.4 billion subscription. Including this sequential drop in the most recent period, the 2013 weekly bond ETF average is now just a $388 million inflow for bond ETFs, much lower than the $1.0 billion average weekly inflow from 2012.

HEDGEYE Asset Management Thought of the Week: The Market is Tapering the Long End Itself:

While the U.S. central bank continues to peg its bond buying programs to backward looking forecasts, the bond market continues to taper the long end of the curve itself and has pushed the 10 year Treasury yield up from a low of 1.6% in May to its current level of 2.6% this week. Hedgeye's Macro Team has introduced the thought that the continued accelerating improvement in year-over-year weekly jobless claims will eventually be reflected in the monthly Non Farm Payroll (NFP) numbers (despite different bias' in these data-sets) and that next week's NFP print for September on Friday, October 4th may finally prove out a closer relationship between these two employment variables. Thus, the 10 year Treasury yield may again spike up to recent highs on renewed Fed tapering expectations. In the event of a back up in 10 year rates again, we continue to observe the correlation between 10 year Treasury yields and Franklin Resources (BEN) stock which has strengthened over recent weeks. This investment manager with a large exposure to Municipal bond trends and Global Bond flows has been trading on the trajectory of long term yields under the thought that as bonds sell off, the fixed income and retail nature of BEN's assets-under-management levels will be negatively impacted. When we first spotted this developing correlation, the R-squared between BEN and the US10YR was 0.32. The R-squared currently is 0.50 and continues to bear watching especially if U.S. macro economic data continues to improve.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA