PNRA remains on the Hedgeye Best Ideas list as a short.

The street currently expects the trends and issues Panera faced in 2Q13 to disappear by 4Q13, but we view this as highly unlikely. There is no quick-fix to these issues and we believe they will persist for a while. We address these issues below and highlight where our views differ from consensus.

SECULAR ISSUES

More Fast Casual Options – NPD recently reported in its CREST industry tracking service that, for the 12 months ended in May, visits to fast casual restaurants grew +9% year-over-year and the number of fast casual units grew +7%. While it is unlikely that all the new units are those of direct competitors, this increase will hurt traffic trends on the margin as consumers have more options.

Not The Only Healthy Competition – Not only is Panera seeing more competition in the fast casual space, but also from QSR chains that are upgrading their menus. This, on the margin, is negative for Panera. These menu upgrades include items that are being competitively marketed as healthy eating options and are cheaper than PNRA’s core offerings, making them very attractive to consumers.

No Pricing Power – With an average check in the $9-$10 range, PNRA has created a pricing umbrella for non-traditional competitors to take advantage of in order to capture incremental market share. We have seen this begin to play out, as a number of casual dining chains are now offering lower price points at lunch, typically in the $6-$7 range.

SELF-INFLICTED ISSUES

Operational – The company has publicly admitted to having a number of widespread operational issues, ranging from a lack of kitchen equipment to a lack of seating. Capacity issues have dampened lunch time transactions and management has struggled to drive peak hour throughput. Therefore, we believe the labor line favorability the company has seen lately will wane, as PNRA will have to invest increased labor in some of its cafes in 2H13. Our view, in this regard, is not widely shared. The consensus expectation is for labor costs to be flat as a percentage of sales in 4Q13, a feat that we view as very unlikely.

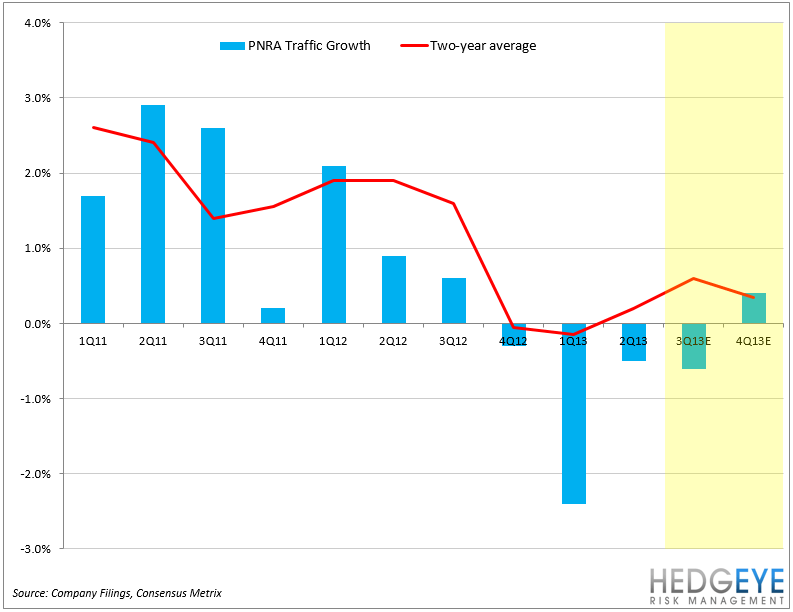

Panera’s Traffic Problem – We believe PNRA has been too aggressive in its pricing over the past five to six years. Panera’s pricing umbrella we referred to earlier has resulted in traffic declines for the past three quarters. While consensus is looking for a conservative -0.6% decline in 3Q13, a rebound to a +0.4% gain in 4Q13 is aggressive.

Still Loved By The Street – The aforementioned issues are manifesting themselves in the components of comparable sales growth, as PNRA traffic trends have been a point of weakness lately. At 9.8x EV/EBITDA, the stock currently trades at a discount to its QSR peer group trading at 14.x EV/EBITDA. We believe this discount is justified and expect PNRA to have another rough outing in 3Q13.

Howard Penney

Managing Director