Summary

Kinder Morgan’s 9/18/2013 investor webcast did not refute our key arguments. With respect to O&M expenses on the El Paso assets, the 1H13 FERC data does not show any relative increase from 2011 to make up for the significant ($222MM) drop in maintenance CapEx on these assets. On the E&P CapEx issue, we continue to believe that Kinder Morgan is defending the indefensible. Investors should consider the massive wealth transfer from KMP to KMI that this CapEx policy creates…~$200MM per year is a big number, despite Kinder Morgan’s attempts to downplay it. We discuss these issues, and more, below.

But First, A Correction

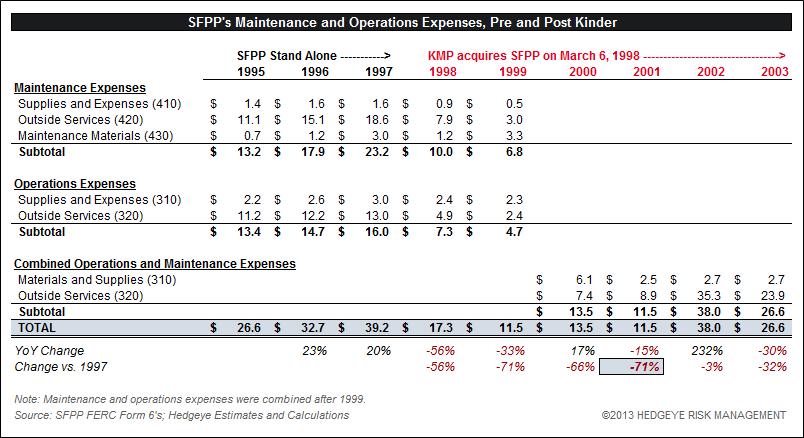

In our 9/10/2013 report we incorrectly stated that, “By 2002, [SFPP’s maintenance expense] was down 99% from 1997 to $0.4MM.” This line item was actually $38.0MM. So, by 2001, SFPP’s maintenance expense was down 71% from 1997 to $11.5MM, before increasing to $38.0MM in 2002.

With respect to CALNEV, we incorrectly stated that, “In 2002, two years after Kinder Morgan acquired the system, [maintenance expense] was down 90% to $0.4MM.” The correction reads down 47% to $2.3MM.

The point, however, remains the same. Kinder Morgan immediately cut maintenance expenses significantly on SFPP and CALNEV after acquiring them. As we detailed in our 9/10/2013 report, the systems had "a rise in pipeline incidents" in the early 2000’s. Likely in response to these incidents, Kinder Morgan increased maintenance spending at SFPP in 2002, and then replaced SFPP’s major lines with three “expansions,” totaling ~$450MM in CapEx. All of that CapEx was allocated to expansion CapEx, despite the fact that the majority of the projects’ scopes were replacing existing capacity. We consider this to be a major example of a cut, defer, replace and expand maintenance strategy, which Kinder Morgan could be in the early stages of on the 2012-acquired El Paso assets.

The corrected table with the relevant SFPP data is below. We regret the errors, and thank Kinder Morgan for bringing them to our attention.

Where is the Increase in O&M Expenses?

“…most costs of real pipeline integrity are not in sustaining CapEx at all, they're in the expense category, and these for example include all of the running of ILI tools like smart pigs, and most of the repairs on anomalies that are made as a result of running those tools. Those are all expense items or almost all of them are expense items.”

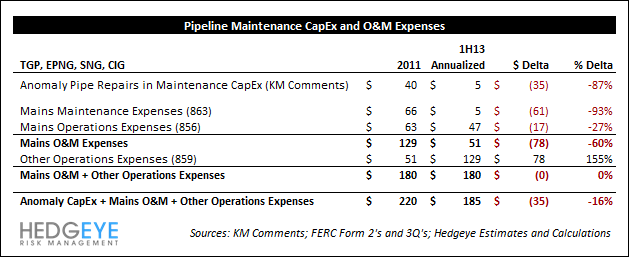

“We will spend this year $5.3 million on anomaly repairs [in sustaining CapEx]. So you say, "Oh, my goodness, that's a huge difference, they must not be repairing their pipeline." But let's look at the whole story. In 2011, as I said, most of this is expensed, not sustaining CapEx. When you do these digs and do these repairs, unless they are truly major repairs, FERC accounting requires you to put them over in the expense category. With that in mind, in 2011 El Paso spent $40 million on anomaly repairs in sustaining CapEx and $33.9 million on anomaly repairs in expense. So the total that they spent on anomaly repairs was $73.9 million. In 2013 at Kinder Morgan, as I said, we're spending $5.3 million in anomaly repairs in sustaining CapEx, and we're spending $96.8 million in O&M [operations and maintenance] expense for anomaly repairs. So the total in 2013 on these assets being spent on anomaly repairs, and that's where the rubber meets the road, is $102.1 million this year versus $73.9 million in 2011. We're spending $28 million more, but the net reduction in sustaining CapEx is $35 million…”

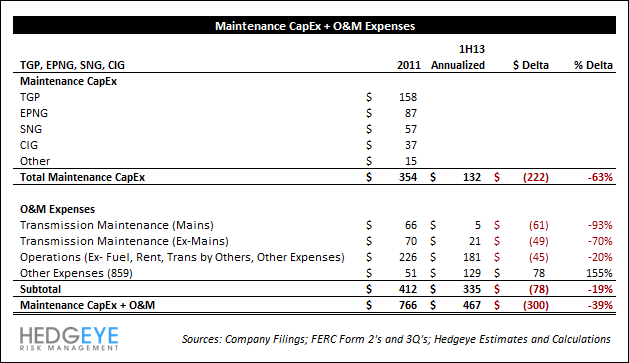

First, Kinder Morgan reconciled one year (2011) of El Paso's maintenance CapEx to Kinder Morgan’s level in 2013. We presented 10 years of data, and over those 10 years, El Paso’s maintenance CapEx on its four big systemes (TGP, EPNG, SNG, and CIG) was, on average, $351MM per year.

The crux of Kinder Morgan’s pipeline maintenance argument is that it is expensing a large amount of maintenance spending – “anomaly repairs” – that El Paso previously capitalized. Kinder Morgan stated on the call that in 2011 El Paso spent $74MM on anomaly pipeline repairs with $40MM in maintenance CapEx and $34MM in O&M expense, and that Kinder Morgan, in 2013, will spend $102MM on anomaly repairs with only $5MM in maintenance CapEx but $97MM in O&M expense. So, we are looking for a ~$63MM increase in O&M expense in 2013 from 2011 to more than offset the $35MM decline in maintenance CapEx.

However, we do not see it in the 1H13 numbers. Annualizing the 1H13 numbers and comparing them to what El Paso spent in 2011, mains maintenance expense is down $61MM (93%), and mains operations expense is down $17MM (27%).

Perhaps these “anomaly repairs” are in “Other Expenses (859),” as that category is up $78MM (155%) in 2013 from 2011. We are not sure why pipeline repairs would fall into this “Other Expenses” category (or if they even do), which the Natural Gas Act defines as, “This account shall include the cost of labor, material used and expenses incurred in operating transmission system equipment and other transmission system expenses not includible in any of the foregoing accounts, including research, development, and demonstration expenses.”

However, even if we assume that this is where all the pipeline anomaly repairs are, then there has been no net increase in pipeline O&M expenses from 2011. The increase in “Other Expenses” equals the decrease in mains maintenance and operations expenses. Further, taking together anomaly repairs in maintenance CapEx, mains O&M, and other expenses, that is down $35MM (16%) from 2011.

“Maintenance CapEx, as I said, gets attracted to things like compressor stations, maybe meter stations, delivery points, receive points, things like that, that are kind of the moving parts. There is very little that's attracted to the pipe because the pipe, if it's properly protected and coated and periodically inspected and repaired, really can last indefinitely.”

“The next category is mechanical and equipment [sustaining CapEx]. And the number there, savings, is $30 million. And let me explain what that is. It has nothing to do with pipeline integrity. It embraces matters like compressor overhauls, automation projects, vehicles across all of our thousands of employees, and equipment used by field employees. Again, it has nothing to do with pipeline safety or integrity.”

Not only has Kinder Morgan cut mechanical and equipment CapEx by $30MM, it has also reduced non-pipeline (compressor stations, meter stations, other equipment, etc.) maintenance expenses by an additional $49MM. Non-mainline maintenance expenses on TGP, EPNG, SNG, and CIG fell from $70MM in 2011 to $21MM in 2013 (annualizing the 1H13 numbers), or down 70%.

We recognize that Kinder Morgan was speaking to full-year 2013 numbers on the call, and of course, we are limited to only the 1H13 actual numbers. So perhaps there are significant maintenance expenses coming in 2H13, though we will believe it when we see it. The 1H13 numbers do not corroborate Kinder Morgan’s suggestion of a material increase in maintenance expenses relative to what El Paso spent in 2011 – in fact, they suggest the opposite.

Kinder Morgan Can’t Justify its E&P CapEx Policy

“That's expansion capital. That's expansion capital in our book. It's expansion capital in the partnership agreement and I think it's an investment under anybody's use of the term. That's how we've been doing this for years. It's well-known. It's discussed. It's the right way to do it. I think the focus on whether or not the base business is growing or not is an inapt focus. This is expansion capital.”

Kinder Morgan was adamant that its philosophy on assigning zero maintenance CapEx to its E&P operations, regardless of production and reserve levels, is “the right way to do it.”

Right for KMI, wrong for KMP?

The partnership agreement is often cited as a defense for Kinder Morgan’s treatment of E&P CapEx by management and Kinder Morgan supporters, but we point out that the partnership agreement is not at all explicit on E&P assets, they are just conveniently omitted from the definition:

"“MAINTENANCE CAPITAL EXPENDITURES" means cash capital expenditures made to maintain, up to the level thereof that existed on the Closing Date, the throughput, deliverable capacity, terminaling capacity, or fractionation capacity (assuming normal operating conditions, including, without limitation, down-time and maintenance) of the assets of the Partnership and the Operating Partnership, taken as a whole, as such assets existed on the Closing Date and shall, therefore, not include cash capital expenditures made in respect of Capital Additions and Improvements. Where cash capital expenditures are made in part to effectuate the capacity maintenance level referred to in the immediately preceding sentence and in part for other purposes, the General Partner's good faith allocation thereof between the portion used to maintain such capacity level and the portion used for other purposes shall be conclusive.”

When asked this important question on the call, “…your partnership agreement says growth capital is anything that increases the capacity of the asset or the system. What do you define as the asset or the system? Is it the well, is it the field, is it the entire E&P business? What is it?” Kinder Morgan responded with, “Yeah, what we're doing is we're looking at that specific project and it's just typically not that hard. I mean, if you look at the vast majority of our expansion capital projects, we're putting new pump stations, new compression, new pipeline looping, new tanks, new wells, you name it. I mean, we're putting in identifiable new facilities and equipment. And for that investment, we're doing an economic analysis and it's usually not that hard to do that.”

We don’t know what this answer means – we don’t believe that the question was even answered.

We fundamentally disagree with Kinder Morgan on its E&P CapEx policy. In our view, it is misleading to call CapEx incurred just to keep production and reserves flat (or even declining volumes) “expansion CapEx” – because what, exactly, is this CapEx expanding?

More importantly, this policy creates an enormous wealth transfer from KMP to KMI that should not be taking place. For instance, with KMI in the 50/50 IDR split, KMP will pay ~$200MM in additional fees to KMI in 2013 alone (and, going forward, at least that amount on an annual basis) due to what is, in our opinion, a misclassification of CapEx. Over the last 10 years, KMP has incurred ~$3.2B of E&P development costs (excluding acquisitions) – all of which have been considered expansion CapEx, resulting in ~$1.5B of additional IDR fees to KMI and dilution to KMP’s cap structure.

We don’t care what KMP’s partnership agreement says or doesn’t say. And we don’t care how long Kinder Morgan has done it this way… The fact that this is the way Kinder Morgan has done it for over a decade makes the situation worse, not better. This policy is materially misleading, and results in KMI taking hundreds of millions of dollars from KMP every year that it should not be.

On “Gold-Plating”

“Now let me make it very clear that we don't gold plate our sustaining CapEx or anything else that we do at Kinder Morgan. For those of you who followed me for 16 and half years, you know that's just not our style. So we do not believe in spending sustaining CapEx, just to spend money and put it in a rate base and then earn on it. We don't believe – that was appropriate, let me say, maybe when I started out 33 years ago in this business, but that's not appropriate today, because everything that you do eventually gets into the rates you charge for your transportation services.”

In 1996, El Paso Natural Gas (EPNG) entered into a settlement with its shippers that established the rates, terms, and conditions of service that would apply for 10 years (until January 1, 2006). The settlement “shielded” EPNG’s customers from a rate increase from 1996 – 2006. Thus, in our view, it is highly unlikely that El Paso would “gold-plate” EPNG during these years. In fact, if there were ever a time to cut maintenance spending, it would be after a lengthy rate settlement like this one. But in each year from 2002 – 2005, EPNG spent $123MM, $103MM, $107MM, and $106MM of maintenance CapEx (+200% of depreciation), respectively. And when the settlement period ended, there was no drastic change in EPNG’s maintenance CapEx. We see no evidence of “gold-plating” at EPNG, or the other major El Paso assets. In 2005, Southern Natural Gas (SNG) entered into a rate settlement that established a rate moratorium until March 1, 2009. SNG’s maintenance CapEx data from 2002 – 2011 does not suggest any material change in spending before, during, or after this settlement.

“…everything that you do eventually gets into the rates you charge for your transportation services.”

Indeed. So when Kinder Morgan reduces the rate base by spending maintenance CapEx below depreciation, and increases earnings by reducing O&M expenses, it is subjecting itself to future rate reductions if and when the FERC initiates a section 5 rate case. And the FERC has been more aggressive in recent years in calling section 5 natural gas line rate investigations – EPB has already had adverse rate rulings at WIC and SNG in 2013 (see EPB’s 2Q13 10-Q). And rate cases can be a significant risk to a major system like EPNG, TPG, SNG, or CIG. For instance, Kinder Morgan’s Natural Gas Pipeline Company of America (NGPCA, 20% owned by KMI) had an adverse FERC section 5 rate case in 2010, resulting in phased-in rate reductions (FERC Docket RP10-147-000). In 2009, NGPCA generated ~$644MM of operating EBITDA; in 1H13, operating EBITDA was down to just $148MM ($296MM annualized). Since that 2010 rate case, NGPCA’s EBITDA has been more than cut in half. If Kinder Morgan is “over-earning” on these El Paso assets today, that could mean future rate (and DCF) reductions.

Other Key Quotes & Points

“…what PwC signs off on is our GAAP financial statements and that's what they deliver an opinion on.”

Kinder Morgan’s auditor does not deliver an opinion on its non-GAAP financial measures, including sustaining CapEx and DCF, which is what (almost) everyone values the equity on.

---

“Something that's been mentioned out there is environmental and legal reserves. If you look at our environmental and legal reserves, on the legal reserves, what we treat as a certain item is the legal reserve that relates to prior years. And if you go back and you listen to the second quarter call, what I said was any amount of that legal reserve that relates to the current year operations, we deduct in determining our DCF. So what we're saying is take out the prior years because that does not relate to the entity's ability to generate cash on ongoing basis.”

We addressed this issue in original report, but to make the point again… Kinder Morgan considers settlement payments for past overcharges “Certain Items” and adds them back to DCF. In our view, it is fine to call a settlement payment a “Certain Item,” but it should not be excluded from DCF.

To understand this point, consider a scenario where Kinder Morgan overcharges shippers by $100MM per year for 5 years, and then loses a rate case such that annual revenues are reduced by $100MM going forward and Kinder Morgan is ordered to pay the shippers a cash settlement of $500MM for the past overcharges. In Years 1 – 5, DCF is increased by $100MM per year, and that is split 50/50 between KMI and KMP ($250MM to KMI and $250MM to KMP), however, the cash settlement paid to remedy the overcharges ($500MM) is borne 100% by KMP because it is excluded from DCF. Thus, in this situation, KMI actually gains $250MM while KMP loses $250MM.

The questions we ask are: Why should this settlement payment not be included in DCF, such that it is funded 50% by KMI and 50% by KMP? And what incentives does this way of accounting for legal and environment reserves and settlements create for KMI?

In 2010, Kinder Morgan paid $206MM to 11 shippers for past overcharges on the SFPP system. This settlement was split 50/50 between the KMI/KMP. However, in 2011, KMP made $154MM of additional settlement payments (to SFPP and CALNEV shippers), which were funded entirely by KMP.

---

“So let me say, again, our philosophy is not, is not, to skimp on maintenance CapEx and replace it with expansion CapEx. And the real test is, if we were doing that our return on invested capital would go down, but it hasn't.”

“If you look at the numbers that we present every January at our analyst conference, you see that our return on invested capital for the past several years has been between 13% and 14%. If we were loading up the denominator in that equation with lots of unwarranted expansion CapEx, you would see that go down and yet it is not. Also, if we were doing this nefarious action you would see our debt to EBTIDA change precipitously and it is not. It has remained relatively constant over the years.”

1) As discussed in our prior report, we do not believe that the returns that Kinder Morgan is referring to are an accurate representation of “returns on invested capital,” as they are really DCF returns that rely largely upon management’s sustaining CapEx numbers, which we take issue with.

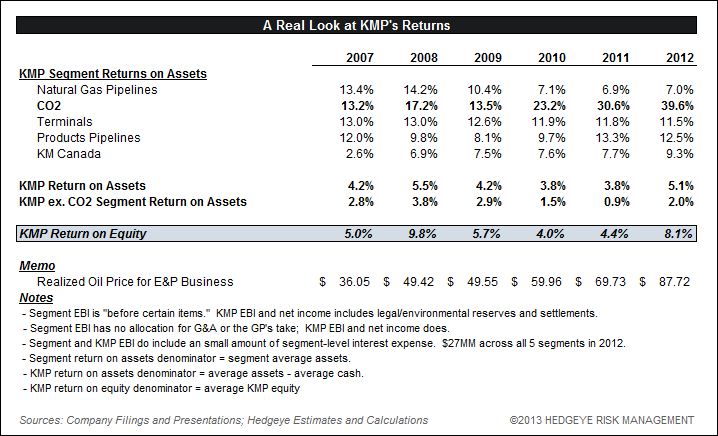

2) On segment-level basis, Kinder Morgan’s CO2 business has dramatically outperformed since 2009 due to strong oil prices. We calculate that KMP’s CO2 segment return on assets in 2012 was ~40%, up from 13.5% in 2009. This has masked some underperforming segments such as Natural Gas Pipelines and Terminals, as we show in the table below.

3) Kinder Morgan states that its debt/EBITDA ratio has “remained relatively constant over the years.” This is a line that the management team uses often – at the Barclays conference on 9/12/2013 management stated that, “So we have maintained the same basic debt to EBITDA ratio over this whole period of distribution growth.” What management does here is it excludes the IDR payment from KMP to KMI. In our view, it is misleading to exclude this significant (~$2B in 2013), recurring fee to the GP from the calculation of KMP’s debt-to-EBITDA ratio.

You can see from the chart below that when taking into account the distributions paid to the GP, KMP’s debt/EBITDA ratio has increased over the years; further, KMP was not 3.7x levered at YE12, it was 5.9x (including the market value of its interest rate swaps).

---

“Now, let me say that it's hard to make industry comparisons about sustaining CapEx versus EBITDA or other categories. But last week, on September 9, some of you may have read Goldman Sachs came out with a piece in which they attempted to compare sustaining CapEx as a percentage of EBITDA spent by all the various large MLPs. Kinder Morgan in 2012, under this categorization spent 11.1% of EBITDA on sustaining CapEx. The industry average was 9.8%. For 2013, based on estimates, 9.8% for Kinder Morgan versus 8.9% for the industry average. Now, let me caveat very quickly that we don't believe that these comparisons are overly meaningful, because pipelines differ dramatically in the size of their pipe, in the age of their pipe, in where those pipes run and there are too many variables to reduce to a metric in our opinion. But I think – and we have not independently verified what Goldman or the other analysts put out, but I think it does show that we are not an industry outlier in this way.”

This analysis from Goldman deducts the IDR fee from the LP to the GP. In our view, this is not an appropriate adjustment to make in such a comparison analysis, as MLPs are in different stages of the IDR “splits,” and some don’t have IDRs at all. KMP has the highest IDR burden (as a % of total distributions) of all MLPs In 2012, KMP’s EBITDA before Certain Items was $4,144MM and sustaining CapEx $285MM, putting sustaining CapEx-to-EBITDA at 6.9%, not the 11.1% referenced by Goldman and Kinder Morgan. For 2013, KMP has guided EBITDA to $4,980MM and sustaining CapEx to $339MM (pre-CPNO), putting sustaining CapEx-to-EBITDA again at 6.9%, not 9.8%.

---

“We think the key indicator is how the assets perform in various environmental health and safety metrics, for example, spills per mile or number of pipeline incidents in a given period. Now, we have – we are not naïve. We have 82,000 miles of pipeline and 180 terminals, and there will be incidents, no matter how hard we try, but we measure ourselves, our performance, on EH&S categories against 31 categories across all of our five business segments and in all of those, we are better than industry average.”

Kinder Morgan’s safety record from 2006 – 2012 is of little importance to us. It’s acquisition of El Paso – then the largest natural gas pipeline company in the US – closed in May 2012, and Kinder Morgan sharply reduced maintenance spending on those assets in 3Q12. So, we are only one year into this lower maintenance run-rate on these assets. In our view, the safety and reliability record that matters here is the one we have yet to see. This is the risk that Kinder Morgan investors should consider today.

With respect to Kinder Morgan’s legacy assets, we are more concerned with the Company possibly misclassifying what should be maintenance CapEx as expansion CapEx, as opposed to KM just not spending the capital outright. In our view, proper maintenance CapEx would be CapEx needed to maintain unit volumes – such as production or throughput; asset capacity does not generate cash flows, and when maintenance CapEx is linked to asset capacity (as it is for Kinder Morgan), there is considerable wiggle room for what the Company can and will call maintenance/sustaining vs. expansion/growth CapEx. We believe that Kinder Morgan uses this discretion to KMI’s advantage, and KMP’s detriment. The three SFPP “expansions” are a good example.

It is also obvious in the E&P segment. But also consider the Product Pipelines segment where Kinder Morgan’s annual expansion CapEx has average $170MM per year since 2008, while throughput volumes were down 2% per annum. Further, Kinder Morgan appears to have a similar problem in its bulk terminals business. 58% of KMP’s Terminals Segment facilities are bulk terminals. Kinder Morgan’s bulk tonnage in 2012 was 8% below what it was in 2008. The volume growth in Kinder Morgan’s Terminals Segment has been only on the liquids side.

Conclusion

Kinder Morgan’s webcast last week did not refute our key concerns. With respect to O&M expenses on the El Paso assets, the 1H13 FERC data does not show any relative increase from 2011 to make up for the significant ($222MM) drop in maintenance CapEx. On the E&P CapEx issue, we continue to believe that Kinder Morgan is defending the indefensible. Investors should consider the massive wealth transfer from KMP to KMI that this CapEx policy creates…~$200MM per year is a serious issue, despite Kinder Morgan’s effort to downplay it.

Kevin Kaiser

Senior Analyst