“Knowing Is Half The Battle” - G.I. Joe

It’s been more than two years since the Budget Control Act (BCA 2011) was passed as a first step towards reigning in federal fiscal profligacy. Subsequent legislation, principally the American Tax Payer Relief Act (ATRA 2012), modified the original provisions and adjusted the caps on discretionary budget authority.

With the new fiscal year here and congressional cantankery again in crescendo, we thought it worthwhile to provide a cliff note review of the 2014 budget setup, with a focus on the projected impacts of sequestration specifically. Unless you’ve followed the legislation closely, the details are probably fuzzy at this point and a superficial read of the headlines can be misleading in regards to both the magnitude and real economic impact of the legislated cuts.

Garnering a clean read on what a fiscal policy actually proposes, how it’s being measured and scored and the mechanics of its implementation is probably more than half the battle in analyzing fiscal policy measures. Below we offer a summary refresh on the details of sequestration and some clarity on the main points of confusion.

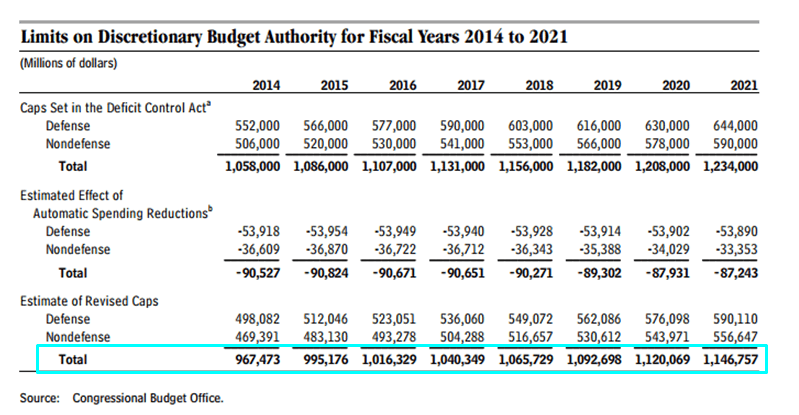

TWO SETS OF CAPS: There are currently two discrete sets of caps on discretionary spending in place that are independent of one another. The Budget Control Act of 2011 placed a first set of caps on discretionary budgetary authority (see top set of numbers in table below). Cuts legislated under sequestration are incremental to the BCA caps and work to further lower the total discretionary budget authority in each year through 2021 (middle set of numbers in CBO table below).

THE BUDGET CONTROL ACT: The Budget Control Act (BCA), enacted in August 2011, put a cap on total federal discretionary spending with separate sub-caps on Defense and Non-Defense discretionary programs. The caps were put in place for the fiscal years 2013-2021 with the goal of reducing projected deficit spending by $1.5T over that period (more on that in “Scoring Sequestration” below).

SEQUESTRATION: The BCA created and charged the Joint Select Committee on Deficit Reduction (i.e. the “Supercommittee”) with finding deficit savings incremental to those achieved under the discretionary caps set forth in the BCA. Specifically, it called for $984B in additional budget cuts, divided equally over the nine years spanning 2013-2021 ($109.4B per year, divided equally between Defense and Non-defense Discretionary). Sequestration was the fall-back provision that automatically cut funding should the Supercommittee fail to reach agreement on an alternative source of deficit reduction. The committee failed to reach an accord, thus triggering the Sequestration provision.

BUDGET AUTHORITY vs. OUTLAYS: The statutory caps on discretionary spending target Budget Authority. Budget Authority represents the allocation of funds in a given year that an agency can use to make financial commitments. Budget Authority, however, does not necessarily equal spending. If an agency has excess funds or appropriations from prior years it can still spend those dollars – the effect being that total outlays could exceed total budget authority in a given year.

SCORING THE SEQUESTRATION CUTS: This point is simple but a key one to remember when evaluating the real economic impact of the “cuts”. The often cited “Cuts” for a given year do not refer to incremental, year-over-year reductions in spending. The cuts, as they are quantified and quoted, are relative to total projected spending under the 2010 funding path.

To clarify, when congress was debating the Budget Control Act and the Simpson-Bowles deficit reduction committee was actively evaluating deficit reduction options, the latest available data was the official discretionary funding level for 2010 and the CBO’s forecast for discretionary spending over the 2012-2022 period. In their baseline scenario, the CBO’s took the 2010 funding level for discretionary spending and inflation adjusted it to arrive at projected spending over the subsequent decade.

To illustrate using 2014 as an example - the scheduled cut (as scored by the CBO/OMB and quoted in the press) for fiscal year 2014 is $109B. This does not mean that discretionay outlays will be $109B less than last year – it means budget authority for 2014 will be $109B less than the CBO projected it would be back in 2010 based on the 2010 inflation adjusted spending path.

EXTRA APPROPRIATIONS: Overseas Contingency Operations (i.e. war funding), Disaster relief, Emergency Designations and Program Integrity Funding all, despite being discretionary in nature, fall outside of the purview of the caps legislated under BCA. Spending for these programs totaled $152.6B in fiscal 2013 according to the CBO (Here). Total spending on these ‘adjustment’ items represents the chief means by which total spending could deviate from that legislated under the tight controls in place under the discretionary spending caps. In fact, adjustments in 2013 increased total discretionary budget authority over the 2012 level.

SEQUESTRATION MODIFICATIONS: The American Tax Payer Relief Act (ATRA 2012), which served as the resolution to the fiscal cliff issue, modified the sequestration cuts for fiscal 2013 and 2014 legislated by BCA. Specifically, it lowered the legislated cut for 2013 by $24B from $109B to $85B. As an offset, ATRA lowered the 2014 cap by $8B (split evenly between defense and nondefense).

It's worth noting that while the total cut was reduced for 2013, the final decision came in March, 5 months into the fiscal year - which, on an annualized basis, equates to ~$140B in cuts. For any agency that hadn't already adjusted budget expectations, any adjustments had to be concentrated in order to stay below sequestration defined levels over the balance of the year.

ABSOLUTE FUNDING WILL DECLINE IN 2014 BUT RISE THEREAFTER: Total Discretionary Budget Authority is scheduled to decline $76B to $967B in fiscal 2014 from $1043B in FY2014. From FY2015 to 2021, funding is scheduled to grow approx +2.5% per year.

So, unless congress reaches an accord on an alternate path to deficit reduction, total discretionary budget authority will decline by ~$76B in absolute term in 2014. However, depending on the level of extra appropriations and the difference between actual outlays vs authorized funding, that negative difference could narrow or even turn positive.

All-in, the real economic impact of sequestration in 2014 will probably be equivocal. For the second half of the decade, discretionary budget authority (and presumably actual spending by extension) will resume positive growth.

Christian B. Drake

Senior Analyst

Resources/References:

OMB Sequestration Preview Report for FY 2014 >> HERE

CBO Sequestration update Report (Aug 2013) >> HERE

CBPP – Sequestration, Clearing Up misunderstandings >> HERE

(BCA 2011) Budget Control Act of 2011 >> HERE

(ATRA 2012) America Taxpayer Relief Act of 2012 >> HERE