#RatesRising has been one of the most important 2013 themes our macro team has written on at Hedgeye. The implications for the Consumer Staples sector are significant as the evidence suggests that yield-starved investors may have sought refuge in the ample yield offered by consumer staples stocks during the 2009-2012 period. Here we detail our thoughts on the space following last week’s surprise announcement and our view on individual names.

Summary: We continue to favor stocks with strong fundamentals, organic sales growth and strong cash flow, over slower-growth, high yielding stocks. Despite the “no taper” decision from the Fed last week, we believe 2009-2012 yield-chasing capital will continue to flow out of staples with poor fundamental outlooks, even if “attractive” yields perpetuate favorable sell-side sentiment.

- Highest inverse correlation between the 10-year yield and staples price action over the last 6 months:PM, KO, KMB

- Food processors are more strongly driven by corn, #RatesRising a good thing (strong $)

- We like LO, BNNY, SAM, EL, CL on the long side

- We are bearish on KO, DPS, ENR and KMB

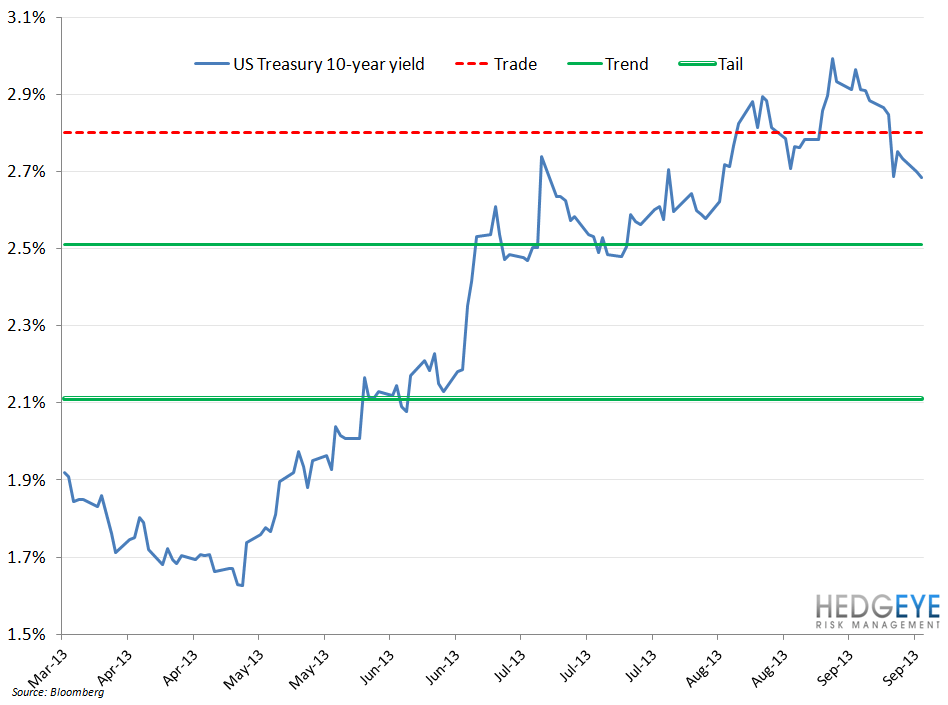

A Topic du Jour: As the chart below illustrates, the prospect of the Federal Reserve lightening the pressure on the accelerator has garnered increasing levels of attention from the markets since the second quarter. Last week’s surprise move by the Federal Reserve to delay a tapering of its bond purchases certainly registered with investors in the consumer staples sector. The “no taper” announcement spurred a significant one-day move in all equities, particularly those that had underperformed as the expectation of rates rising grew.

While we recognize the change in the Federal Reserve’s tone, the shadow of “tapering” could continue to weigh on certain names within the sector, particularly if the economic (employment) data continues to support a tightening of the QE spigot.

The Intermediate-Term TREND Has Been Dominated by “Rates Rising”: We’ve shown the chart below in earlier notes, but it is worth highlighting again. During 2009-2012, the data suggested that many investors sought out staples and other dividend-yielding, stable, sectors for a reliable yield. This would suggest that much of the capital flowing into staples may have been more focused on yield than fundamentals, which then resulted in some capital exiting the group as expectations increased that the Fed would taper. Indeed, on a stock-by-stock basis, it seems that some performance has been inversely related to dividend yield over the past six months, with the exception of sentiment-driven groups like the Food Processors where, with a strengthening of the dollar pushing corn prices lower, the result can coincide with stronger profit margins.

Below, we highlight the sectors of the S&P 500 and their performance relative to each other. We also break out the subsectors of the Consumer Staples sector and highlight their respective price actions relative to the average S&P 500 sector.

Food, Food Processing, & Tobacco: The correlation between Food Processing stocks and the 10-year yield, overall, has been positive over the last six months as the corresponding strength in the U.S. dollar offered respite from the margin pressure associated with high corn prices that had weighed on SAFM, TSN, and several others in the space. Within the food space, BNNY remains a favorite on the long side. We expect investors to continue to pay up for the outperformance of the organic players. BNNY is showing strong penetration into the mainstream aisle and we believe its new product roll-outs in frozen meals (as frozen pizza gets back on track), alongside continued strength of mac & cheese, and crackers and fruit snacks should allow the company to meet its FY sales guidance of 18-20% and EPS range of $0.97 to $1.01. Its skew to a higher income client should maintain these results despite any swings in the macroeconomic landscape that could come into year-end.

Tobacco stocks' performance has largely reflected weakening volume trends that have only been partially offset by pricing. We continue to like Lorillard’s (LO) portfolio of full-flavored offerings and dominate share in menthol, yet a concern remains around any update the FDA may give on menthols. There’s been much excitement around the e-cigarette category. LO’s Blu e-cig remains the market share leader and, while its sales are around 1% of the portfolio, we see strong category excitement outweighing the contribution that e-cigs are adding to earnings.

Beverages & Alcohol: Beverage consumption of carbonated soft drinks continues to suffer due to shifting health and wellness trends, with KO and DPS two names on our short list. The category has been hit by volume pressure and “unfavorable weather” in recent quarters. We largely remain on the sidelines, given the lack of excitement. Alcohol has held up better than most of its peer categories over the last 6 months and on the beer side our theme remains the outperformance of the craft segment. SAM’s price performance has been an absolute rocket ship and we expect its decision last quarter to invest in its growth to be effective.

Home Products: The stocks that performed the worst under the “tapering” scenario of the last 6 months were those with the highest yield and the weakest fundamentals. KMB is the standout, in this regard, as the bull case became increasingly dependent on cost savings and share repurchase-driven earnings growth in an environment where investors were less willing to pay a premium multiple for yield with little organic growth. Other names within the space, like CL, that are posting strong organic growth numbers and face a relatively benign cost environment, are more attractive than KMB on the long side.

We remain bearish on KMB as, despite the extension of QE as we know it, we believe it is unlikely that the Staples investing environment will revert to that which typified the 2009-2012 period, when it seems fundamentals were of lesser importance than the stability of the respective yields of consumer staples stocks relative to the concurrent decline in treasury yields. The fundamental outlook for KMB suggests further downside to earnings expectations.

Personal Care: Our view of stocks within this sector is less sensitive to interest rates, as companies like EL are growing earnings at a high-double digit rate with investors holding the stock for growth and not yield. Companies like EL, with ample opportunity in developed and emerging markets, with exposure to the high-end consumer, are attractive to us on the long side.

We remain bearish on ENR as the company continues to struggle versus larger players in the promotion-driven men’s razors category. As with KMB, the ENR bull case hinges on cost savings and potential upside in the earnings multiple; while we expect the company to meet earnings expectations this year, we believe a continuing preference of growth over yield makes a meaningful multiple expansion from here unlikely over the intermediate-term TREND (3-6 months).

Matthew Hedrick

Senior Analyst

Rory Green

Senior Analyst