Our base framework for looking at countries from a macro perspective is our GIP (Growth/Inflation/Policy) model.

It allows us to analyze a country as we would a company and provides a tractable framework for contextualizing how marginal macro data and policy decisions are likely to impact the slope of the revenue and margin lines (Ie. Growth/GDP and Inflation) at the sovereign level.

Our bull case on U.S. growth in 2013, in terms of our most basic US dollar based economic flow model, looked something like this:

$USD Higher --> Energy/Commodities/Inflation lower --> Real Growth Higher --> Pro-Growth Equities Exposure Outperformance

Left to itself, we think this flow sets the stage for positive macro reflexivity and some sustainable economic & market mojo. Of course, policy is the other dynamic variable and, depending on its flavor, can work to catalyze, amplify, or reverse the trajectories of growth and inflation (and equity, bond and currency values by extension).

The Fed and congress were largely non-existent in the first 8 months of the year and all was mostly quiet on the policy front – that was a good thing for the markets, organic macro trends, and main street confidence.

With Bernanke back to perpetuating uncertainty/volatility yesterday and Congress back from recess and promising to save us from their next self-created crisis, the threat is that the above cycle – and the reason we’ve remained positive on the domestic growth outlook – reverses. We’ve obviously seen this movie before as the aforementioned cycle and its converse have played out recurrently over the last four years.

As it stands currently, the strength the of economic data continues to belie the Fed’s wimpish policy stance. Labor Market and Consumer Confidence trends remain strong, ISM figures hit multi-year highs in the latest report, and Existing Home Sales and the Phili Fed trounced expectation this morning.

What does that mean within the context of the emergent policy (monetary and fiscal) dynamics. Right here, we don’t have a convicted call.

Maybe Bernanke doomed us to another compressed economic cycle yesterday, maybe congress will amplify market volatility again over the next month, maybe positive organic macro trends are healthy enough to persist in the face of a policy headwind, maybe Grand Theft Auto sales will take GDP & real final sales to +5% in 3Q. The Risk Management business may be confounding at times, but it’s not boring……

Below is the breakdown of this morning's claims data, along with an analysis of the historical relationship between Claims and Fed Purchases, from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact .

- Hedgeye Macro

------------------------------------------------------------------------------------

Will This Time be Different?

In light of yesterday's announcement by the Federal Reserve that they will not begin tapering QE asset purchases, we thought it would be helpful to evaluate the historical relationship of QE and initial jobless claims. The chart below looks at the Fed's holdings of Treasury and Agency securities on the x-axis and compares those against corresponding levels of initial jobless claims (SA, rolling) on a zero lag basis. The time period is 2009-Present and the data points are weekly. We're using a second order polynomial (i.e. parabolic) regression here to reflect the fact that the level of jobless claims begins to reach frictional resistance below 300k. The equation of the line is shown in the chart for anyone who wants to run their own assessment. Assuming the Fed remains unchanged in its purchases for a further 6 months, which is what we would argue the market likely now assumes, the relationship suggests that we could expect to see claims running in the 275k range by March/April of next year. We're assuming $85bn/mo for 6 months would bring total Fed holdings to just under $4 Trillion.

Assuming their is a causal relationship here and assuming that it persists going forward, this would be very good news for lenders from a credit standpoint. One of our central tenets on COF has been that the labor market is getting better at a faster rate than people realize. This would certainly be consistent with that viewpoint.

While we're personally disappointed in the Fed's decision, the game is what it is, and this has been the historical relationship between claims and Fed securities holdings, i.e. QE. Rather than fight the logic of the decision, we'll look to profit from understanding its implications.

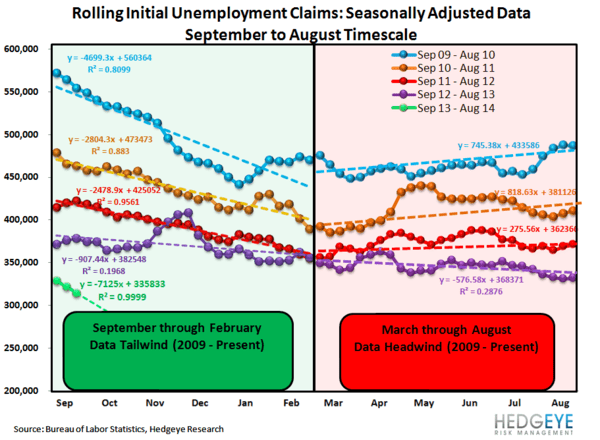

The Data

Prior to revision, initial jobless claims rose 17k to 309k from 292k WoW, as the prior week's number was revised up by 2k to 294k.

The headline (unrevised) number shows claims were higher by 15k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -7k WoW to 314.5k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -16.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -14.3%.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT