TODAY’S S&P 500 SET-UP – September 18, 2013

As we look at today's setup for the S&P 500, the range is 34 points or 1.45% downside to 1680 and 0.54% upside to 1714.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.47 from 2.48

- VIX closed at 14.53 1 day percent change of 1.04%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Sept. 13 (prior -13.5%)

- 8:30am: Housing Starts, Aug., est. 920k (prior 896k)

- 10:30am: DOE Energy Inventories

- 2pm: FOMC Rate Decision, Sept., est. 0%-0.25% (pr 0%-0.25%)

- 2:30pm: Fed’s Bernanke holds news conference on FOMC meeting

- 9:30pm: BoJ’s Kiuchi speech and press conference

- BoJ’s Kuroda speaks in Tokyo

GOVERNMENT:

- President Barack Obama speaks to Business Roundtable on economic proposals aimed at job creation

- Financial Accounting Standards Board, Intl Accounting Standards Board joint public roundtable meeting in London

- 10am: House Armed Svcs Cmte hears from military heads on 2014 defense budget

- 10:15am: Energy Sec. Ernest Moniz, EPA Admin. Gina McCarthy testify before House Energy and Commerce Cmte on combatting global warming

- 2pm: House Ways and Means panel hearing on IRS’s exempt organizations division

- 2pm: Cary Sherman, CEO of Recording Industry Assn of America; Randall Rothenberg, CEO of Interactive Advertising Bureau, testify before House Judiciary hearing on voluntary agreements in intellectual property

WHAT TO WATCH:

- JPMorgan said to agree to pay $200m to SEC over London Whale

- Drop in home loans keeps Fed from tapering MBS purchases

- Starwood property said to plan deal for Waypoint Management

- Dow Chemical suspends sale of plastics additives on low bids

- Sega said to win auction to buy bankrupt game co. Index

- Electronic Arts elevates sports video unit head to CEO: WSJ

- Boeing’s larger 787 completes test flight

- Auto-parts co. Visteon may move to Hong Kong listing: CEO

- Sharp to raise as much as JPY166b through share sale

- Apache to sell $112m in Canadian assets in 2 separate deals

- Dollar Tree takes up $2b share buyback; enters JPM agreements

- Volkswagen may build small SUV in Tennessee

- Tesla CEO Musk sees driverless cars road-ready in 3 years: FT

- Walgreen moves workers to private health care exchange

- AT&T to expand in Latin America with America Movil: Reuters

- Pandora wins licensing dispute against songwriters, publishers

- Blackberry introduces new Z30 handset with 5-inch screen

EARNINGS:

- Apogee Enterprises (APOG) 4:30pm, $0.25

- Clarcor (CLC) 6:26pm, $0.66

- Cracker Barrel Old Country Store (CBRL) 7am, $1.35

- FedEx (FDX) 7:30am, $1.50 - Preview

- General Mills (GIS) 6:56am, $0.70 - Preview

- Herman Miller (MLHR) 4pm, $0.38

- Manchester United (MANU) 6am, $(0.03)

- Oracle (ORCL) 4:01pm, $0.56 - Preview

- Steelcase (SCS) 4:01pm, $0.26

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Declines a Third Day to Six-Week Low Before Fed Statement

- China’s Choking Cities Means Job Cuts at Steel Town: Commodities

- WTI Crude Rises for First Time in Four Days Before Fed Decision

- Copper Climbs Before Federal Reserve Concludes Policy Meeting

- Corn Rebounds From One-Month Low as U.S. Insurance Claims Rise

- Coffee Rebounds in London Before Vietnam Crop; Sugar Declines

- Aluminum Cuts Seen by Wood Mackenzie Too Small to Reduce Glut

- German Power Premium Most Since ’98 Tests Voters: Energy Markets

- Rebar Falls to Seven-Week Low as Purchases Slow, Iron Ore Drops

- U.K. Millers Poised to Buy British as Sun Boosts Wheat Quality

- Australia Sugar Cane Crop Seen Curbed in 2014 If Drought Spreads

- Goldman Sees Commodity Consumption Signs of Life Outside China

- Coffee Supply Gains Spur Bearish Price Outlook: Chart of the Day

- Iron Ore Seen Extending Slump by UBS as Global Supplies Increase

CURRENCIES

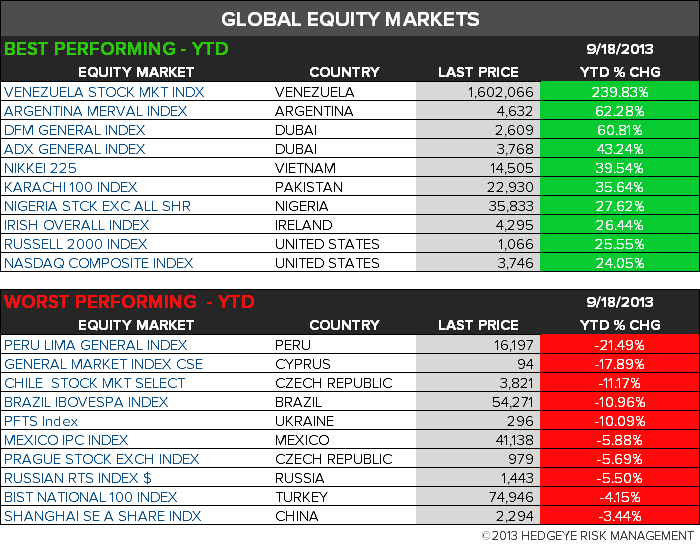

GLOBAL PERFORMANCE

EUROPEAN MARKETS

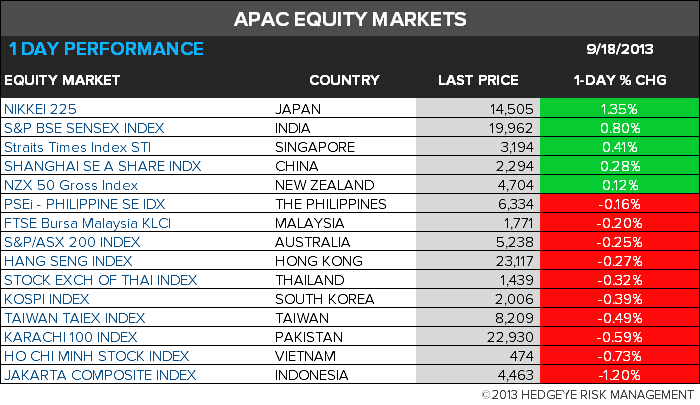

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team