If I had a nickel for every time I've heard that BYD is not cheap and the locals LV market is horrible, I'd own a lot more BYD stock. Of course, I'm restricted from buying stocks I write about but you get my point. I honestly don't know where BYD is going over the near term. Research Edge is a bit negative on the US market, gaming has a high beta, and I'm increasingly cautious on gaming operators overall. However, from a long-term perspective, the stock is actually dirt cheap, and the Las Vegas locals market is a growth market. The company's incredibly valuable credit facility rounds out the positive thesis. It is this final thesis point that I will focus on this note.

As a refresher, BYD's credit facility does not mature until May 2012 and its 2% spread above LIBOR is unmatched in the industry. The effective interest rate is under 3%. BYD currently has $2 billion of borrowing capacity remaining on the facility. The other operators (MGM, WYNN, LVS, ASCA, PNK, PENN) have all refinanced at significantly higher rates or will do so soon.

So what is this valuable asset worth? We see value in two ways. First, in terms of straight interest savings, the differential between BYD's interest rate and the "going rate" is approximately 6%. This differential multiplied by BYD's outstanding borrowings on the line is about $67 million per year. On a present value, tax-effected basis over the remaining 3 year life of the facility we estimate there is $114 million, or $1.30 per share in value.

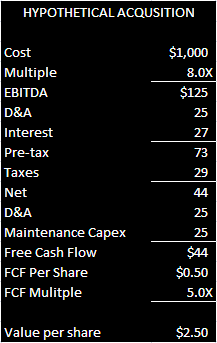

Second, the additional liquidity gives BYD an incredibly cheap cash source to make an acquisition at near trough EBITDA and a low multiple. The assets of Station Casinos come to mind. Assuming a $1 billion acquisition at 8x EBITDA, above current public trading multiples, we estimate BYD could generate $2.50 per share in equity value, as shown in the following table. Please note that these are not wild assumptions. We are only assuming the market gives BYD a 5x multiple of the free cash flow accretion generated by the hypothetical acquisition.

BYD's free cash flow yield is currently north of 20% (highest in the sector), which is not sustainable in our opinion. The valuation doesn't appear to reflect the appropriate value ($3.80) of the credit facility nor does it reflect the 87 acres of Strip acreage. We value the land at $3.50 per share so potentially $7.30 of real value is not being reflected in a $9.30 stock that is already supporting a huge free cash flow yield on current operations alone.