As part of our morning routine, we scour the tape and trade rags for stories that we think might be relevant to our investment process.

EVENTS TO WATCH OVER THE NEXT 24 HOURS

DKS - Wednesday 9/18/2013, 8:00am. At DKS HQ in Pittsburgh.

ECONOMIC DATA

The ICSC index, a compilation of 80 chain store retailers, came in weaker than expected this morning. While still relatively healthy at +3.2% ahead of last year, it turned down sequentially (as evidenced by the red line in the chart below).

COMPANY NEWS

RH: Released its 10Q after the close last night. The biggest callout...

"Selling, general and administrative expenses for the three months ended August 3, 2013 included: (i) a $33.7 million non-cash compensation charge related to the one-time, fully vested option to Mr. Friedman upon his reappointment as Chairman and Co-Chief Executive Officer, (ii) a $26.1 million non-cash compensation charge related to the performance-based vesting of certain shares granted to Mr. Friedman in connection with the Reorganization and initial public offering, and (iii) $2.1 million of costs incurred in connection with our follow-on offerings in May 2013 and July 2013."

Translation = Good day for Gary Friedman

The Hut - The Hut prepares for IPO in early 201

The Hut Group, an online retailer selling apparel, beauty products and gifts, is considering an April or May 2014 IPO. The company is expected to be valued at 350m Pounds, about 25x EBITDA. First half 2013 profits reached 77m pounds a 30% increase YY.

JNY - More Bidders Emerge for The Jones Group

"The head of Sun Capital has joined the fray as a host of private-equity firms prepare bids for the New York-based shoe-and-apparel company, The Post has learned."

"It’s unclear which assets Sun is eyeing, but sources speculate the firm is interested in department-store staples such as Jones New York and Gloria Vanderbilt."

"As second-round bids for The Jones Group Inc. are expected to be forthcoming at the end of this month, more names of possible bidders have surfaced. According to dealReporter, Leonard Green & Partners and Golden Gate Capital are also interested in the assets of Jones Group."

"Last week, sources close to the process confirmed to WWD that KKR & Co. and Sycamore Partners are working together and had already submitted a first-round bid for Jones over the summer."

GPS - Gap's TV Return

Gap Inc. returned to TV after a four year hiatus on Monday. The ad featured Billy Joel's daughter, Alexa Ray Joel, signing "Just the Way You Are," and George Harrison's son, Dhani Harrison, signing "For You Blue."

"Last year, Gap spent $653 million on advertising, a figure that should go up with television back in the retailer’s ad mix, although Gap has stressed its careful approach to the medium."

http://www.youtube.com/watch?v=KAPnSRqgpZE

http://www.youtube.com/watch?v=9kjC0N0P_v4

M - Bloomingdale’s Black Tags End Party for Next-Day Returns

"Instead of just tagging merchandise before it’s purchased to prevent theft, the Bloomingdale’s department-store chain is keeping some garments tagged after they’re sold, too. The three-inch black plastic devices are in visible places, like the front bottom hemline, so they’re hard to hide when the garment is worn. Once shoppers remove the tags, which can’t be reattached, they can’t return the item."

"Bloomingdale’s, owned by Macy’s Inc. (M), is using the tactic to combat a practice known as 'wardrobing' -- buying clothes and using them once -- a form of return fraud, which the National Retail Federation estimates cost the industry $8.8 billion last year."

"Nordstrom doesn’t use such tags, Colin Johnson, a spokesman for the Seattle-based company, said in an e-mail.

DKS - Dick's Revamps Jersey Report

"Dick's Sporting Goods announced an updated and upgraded 'Jersey Report,' with new advanced features to provide fans unparalleled insights into pro football jersey sales at Dick's Sporting Goods nationwide and online. Updated daily, the Jersey Report is the only destination offering fans a comprehensive breakdown of how the sales of their favorite players' jerseys are rising, falling and stacking up against the competition."

"In addition to football, this year's Jersey Report will also provide the same stats and analysis for hockey jersey popularity beginning in October."

GIL - Gildan Named to Dow Jones Sustainability World Index

Gildan Activewear Inc. has become one of only two North American companies to be included in the Dow Jones Sustainability World Index in the Textiles, Apparel and Luxury Goods sector, with effect from Sept. 23, 2013.

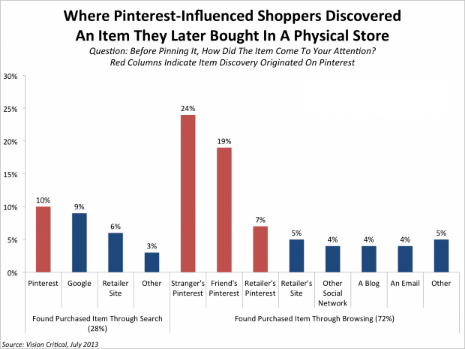

Pinterest Drives The 'Reverse Showrooming' Phenomenon, Where Shoppers Browse Online But Buy In-Store

"Recent data distributed by Vision Critical and highlighted in the Harvard Business Review found that 21% of Pinterest users had bought an item in a store after pinning, repinning, or liking the item on the site."

"Vision Critical describes this as part of a wider phenomenon it calls 'reverse showrooming,' in which consumers search or browse products online and then enter the physical shop to make a final purchase."

INDUSTRY NEWS

US Government Looks to Boost Textile, Apparel Exports

"President Obama launched the National Export Initiative in 2010—the first government initiative of its kind—with the goal of doing more to support US companies by creating export opportunities, working to remove trade barriers and settling new trade agreements...As part of the initiative, the President plans to double US exports by the end of 2014. In the first half of 2013, US exports totaled a record-high $1.12 trillion while imports decreased by $13.1 billion over the same time, reducing the trade deficit by $36.1 billion over the last half year."

The Commerce Department’s Office of Textiles and Apparel (OTEXA) has also been working to increase domestic production and imports. 'The focus of our office has been two-pronged this year — the Made in USA database, as well as our [Trans-Pacific Partnership] and now European Union trade negotiations to help facilitate opening those markets,' Kim Glas, deputy assistant secretary for textiles and apparel at the Commerce Department told WWD."

Calendar Complicates Holiday Selling

"In its preliminary forecast for the season, Chicago-based retail traffic counter ShopperTrak projected that sales during November and December would increase 2.4 percent over 2012 levels, lower than the 3 percent increase registered during holiday 2012."

"Apparel and accessories sales are expected to come in slightly stronger for the season, rising 2.8 percent."

"ShopperTrak expects traffic to dip 1.4 percent from 2012 levels, which rose 2.5 percent from the prior year. For apparel and accessories, the traffic decrease is expected to come in at 1 percent. "

"Much of the pressure on retailers will come from an unforgiving calendar. Last year, the window between Black Friday and Christmas Day was a full 32 days, the maximum possible, and this year will swing in the opposite direction, shrinking to 25."

Turkish Industry Out to Boost U.S. Profile

The Istanbul Textile and Apparel Exporters Association, or ITKIB, is to hold its first trade mission to the U.S. on Sept. 24 and 25 at New York City’s Gotham Hall with the aim of bringing together Turkish apparel and textile manufacturers with U.S. sourcing and distribution executives.

Turkish ready-to-wear companies now operate some 3,000 stores internationally, compared with just 300 five years ago. By 2023, the goal is to have 20,000 — and the U.S. is a new priority.

Clothing and textiles are among Turkey’s biggest businesses, accounting for 6.8 percent of gross domestic product and $24 billion in exports last year. It is the world’s sixth largest apparel supplier and the second largest to the European Union after China.

According to the ITKIB chairman, the New York trade mission is but a first step. The goal is to enable Turkish firms to meet with top-tier executives in production and global sourcing of all major American brands, licensing groups and department stores.