We continue to warm up to Williams-Sonoma (WSM) as a way to play two themes in the retail space.

- First, we are comfortable with the gradual, but increasing momentum in the home furnishing sector. We know that big-ticket items remain under pressure but we are seeing encouraging signs in soft-home, cookware, and accessories. Importantly, any pick up in non-furniture will be positive to WSM on the gross margin line as these categories tend to carry higher IMU's. Consumers are spending more time in their existing homes which results in higher home-related capex.

- Second, in the wake of the severe downturn in the commercial/retail real estate market, we are becoming bigger fans of companies with large, scalable e-commerce businesses. This is not only because it gives these companies a competitive edge vs. others who are levered to real estate values and dysfunctional/bankrupt landlords. More importantly, we think that companies with superior dot.com, e-commerce, and consumer-direct businesses will command a higher premium as we emerge from this cycle as strong companies without such platforms realize that they either need to build them (costly and risky) or buy 'em.

Despite recent sales woes and an expectation embedded in Street estimates that revenues will continue to be challenged for 2009, WSM derives 40% of its revenues from its online/catalog operation. WSM's heritage as a direct marketer makes it a rare brand that actually understands the direct relationship with its customers and has profitably built a business around it. Today WSM is the 20th largest ecommerce business in the U.S.

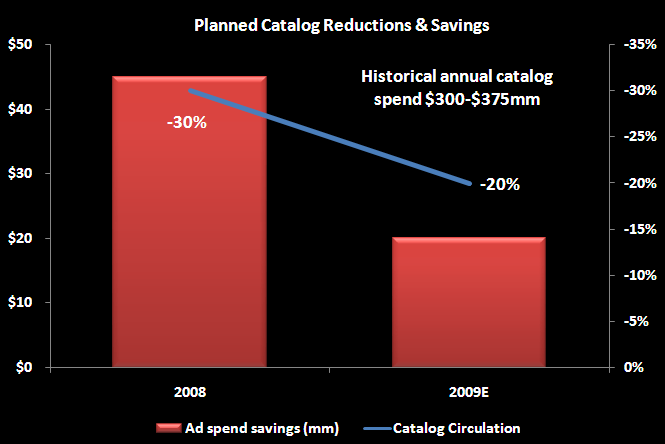

Importantly, the company continues to de-emphasize its catalog mailings (down 30% in '08; down 17% in 1Q09) in favor of more cost-effective brand and targeted online advertising. The benefit from a shift away from paper to a virtual world will not entirely accrue overnight, but there are few retailers with as a great an opportunity to cut costs and improve margins in this area. Currently, the e-commerce business is the most profitable of all the WSM channels, and has the opportunity to produce an even higher ROI driven by shifts away from the catalog to the internet. WSM has relied almost exclusively on the catalog (85-90% of total marketing spend) as its main advertising vehicle which has historically cost 10% of sales.

We have heard for years about how catalogs are going away, consumers prefer to shop online, and call centers are a way of the past. However, the reality of the market has been that most direct marketers were a bit wary to embrace these changes and were even reluctant to dial back catalog circulation for fear that sales would plummet. Currently, WSM direct and retail sales trends are both tracking down in low to mid twenty percent range and within expectations. Now is the time for companies such as WSM to become more aggressive as they seek to cut capex, cut costs, and to preserve and even grow cash flow in the wake of a topline that remains more sensitive to the overall environment. We are seeing this same process unfold at J Crew where catalog circulation has also been cut dramatically as the company shifts it investment towards ecommerce.

We're the first to admit that a company is never going to cut its way to prosperity. It's gotta grow to ultimately have any kind of earnings stability and sustain a reasonable multiple. But we think that the inefficiencies in the existing operation combined with the underlying strength in the brands and the consumer-direct platform should allow the company to pull away costs without meaningfully impacting either the brands or the top line - a rarity in this business.

While this pronounced shift in the direct business is occurring, it's also important to look at WSM's retail business in the wake of planned square footage growth slowing in '09 to only 1%. Importantly, future lease obligations are properly aligned. Near-term obligations outweigh future obligations by a healthy margin - and they have improved in each of the past three years. We view this as a positive sign in terms of the company NOT trading future margin for near-term benefits.

Combining the .com opportunity with a clean balance sheet ($100mm cash and no debt), substantial capex and inventory cuts planned for '09, and weak financial performance expectations, and high short interest at 14% of the float, we like how this story sets itself up..

Eric Levine

Director