TODAY’S S&P 500 SET-UP – September 13, 2013

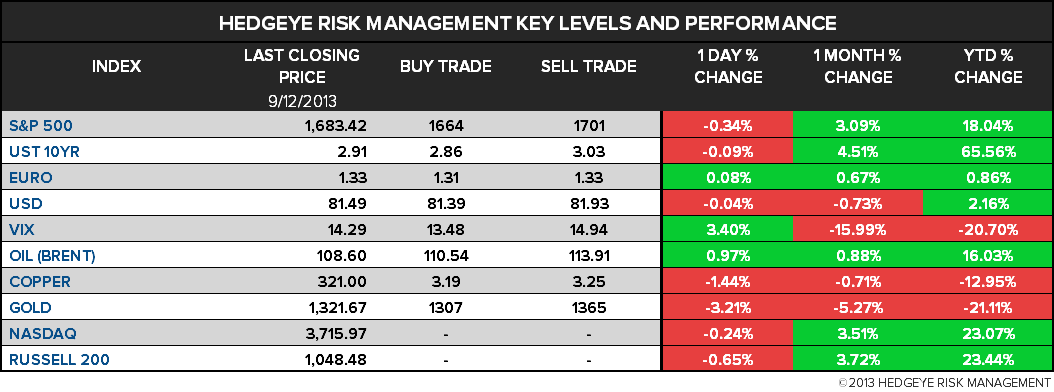

As we look at today's setup for the S&P 500, the range is 37 points or 1.15% downside to 1664 and 1.04% upside to 1701.

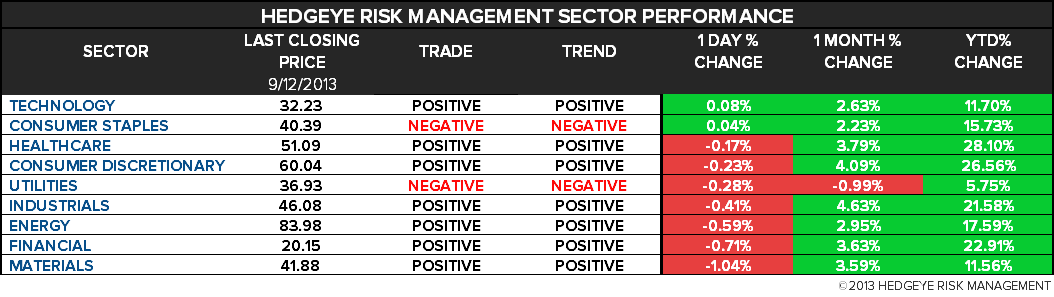

SECTOR PERFORMANCE

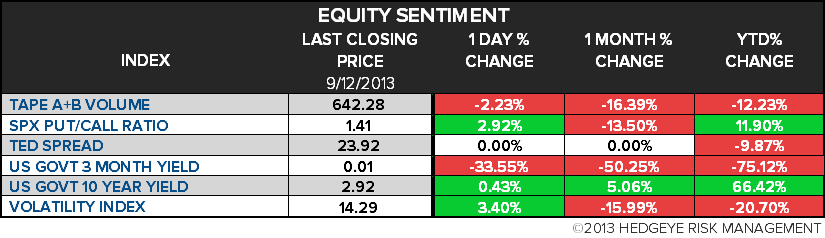

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.47 from 2.47

- VIX VIX closed at 14.29 1 day percent change of 3.40%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: PPI M/m, Aug., est. 0.2% (prior 0.0%)

- 8:30am: PPI Ex Food and Energy M/m, Aug., est. 0.1%

- 8:30am: Retail Sales Advance M/m, Aug., est. 0.5%

- 8:30am: Retail Sales Ex Auto and Gas, Aug., est. 0.3%

- 9:55am: UMich Confidence, Sept. prelim, est. 82 (prior 82.1)

- 10am: Business Inventories, July, est. 0.2% (prior 0.0%)

- 11am: Fed to purchase $3b-$4b in 2019-2020 sector

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Medicare Payment Advisory Commission meets, 9:30am

- CFTC holds closed meeting on enforcement matters, 10am

- President Obama holds talks with Emir of Kuwait Sheikh Sabah al-Ahmad al-Jaber Al Sabah; topics to include defense, energy

WHAT TO WATCH:

- Twitter files IPO w/ SEC; Goldman said to be lead manager

- Derivatives would face transition fees under Obama proposal

- Goldman sees risk of gold below $1,000 as U.S. economy gains

- Vodafone’s $10.2b Kabel Deutschland bid wins shareholder support

- U.S. House Republicans lack fiscal plan as Oct. 1 deadline nears

- Dimon boosted JPMorgan compliance as examiners lost trust: WSJ

- Japan to consider corporate tax cut in stimulus package

- Obama to name Summers as next Fed chief, Nikkei says, citing unnamed people

- Europe’s biggest phone cos. brace for AT&T entry into mkt

- Hoyer says Obama could strike Syria without Congress vote

EARNINGS:

- No S&P 500 cos. expected to report today

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Goldman Sees Risk of Gold Below $1,000 as U.S. Economy Gains

- Gold Traders Most Bearish Since June as Syria Eases: Commodities

- Goldman Lifts Soybean Price Outlook as USDA Downgrades U.S. Crop

- Soybeans, Corn Steady After USDA Releases U.S. Harvest Outlook

- Pemex Holds Emergency Response Meeting on Gulf of Mexico Storm

- Spot Gold Reverses Gain, Slumps to Five-Week Low as Silver Drops

- Copper Set for Weekly Loss as Investors Prepare for Fed Meeting

- Indonesia Commodity Exchange Fails to Sell Tin for Second Day

- Commodity Outlook Is ‘Quite Benign,’ Goldman’s Jeff Currie Says

- Blythe Masters Shows Resilience as Dimon Lauds ‘Impressive Job’

- Natural Gas Rises a Second Day on Lower U.S. Stockpile Increase

- Glencore Agrees to Progress Study of $3 Billion Congo Iron Mine

- Tropical Depression to Bring ‘Threatening’ Floods to Mexico

- Record Soybean Crop to Boost India Meal Sales to 6-Year High

CURRENCIES

GLOBAL PERFORMANCE

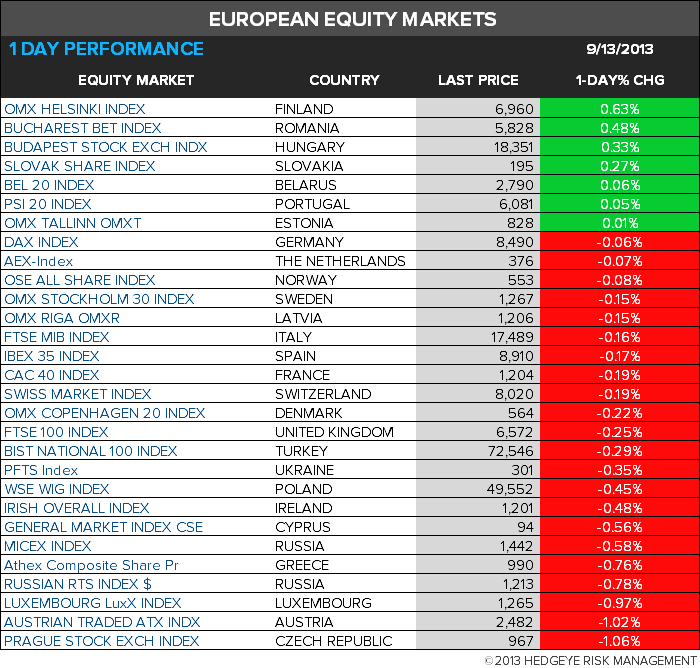

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team