Darden is being mismanaged, plain and simple.

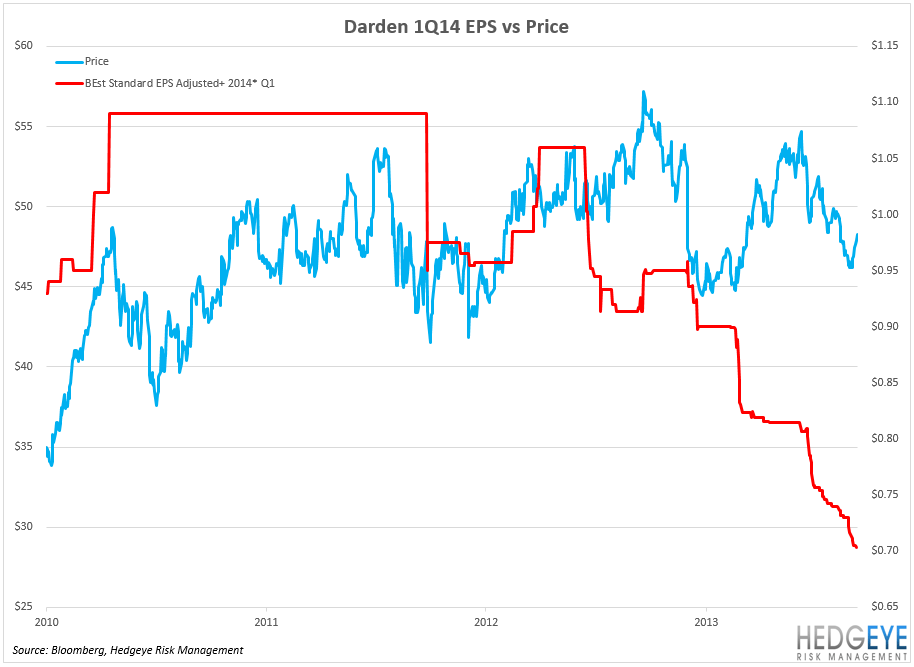

DRI is scheduled to report 1QFY14 earnings on 9/20 and expectations across the board have been reduced significantly for the quarter. The only question that remains is: how bad is bad? The current FY14 EPS consensus estimate is $2.99 on Bloomberg. We could easily get our model down to $2.50. And, unfortunately, the company needs to pay a $2.25 dividend, which makes earning anywhere near $2.50 a real problem.

We continue to believe the sum of the parts is greater than the whole, at Darden, and we believe there is a striking opportunity for an activist to enter the fray, unlock value, and benefit holders of the company’s stock.

There have been four times in my career when I have seen a company in desperate need of a major overhaul. In all four cases, I wrote extensively about the issues, much to the ire of management. Darden and its problems are no different!

The following companies have undergone major corporate overhauls that have led to significant improvements in shareholder value:

- McDonald’s (2002): MCD formulated the “Plan to Win” in 2002, which later became a template for success at Brinker.

- Wendy’s (2004): The sum-of-the-parts were greater than the whole!

- Starbuck’s (2008): With Schultz back at the helm, SBUX focused on attacking the middle of the P&L and improving the guest experience.

- Brinker (2010): Facing an industry in the midst of a secular decline, senior management formulated a plan to win, which entailed attacking the middle of the P&L and driving traffic.

- Darden (2013): Will the current management team recognize the need for a major restructuring?

We are of the view that DRI is in a secular decline and, until management makes significant changes, we will continue to see erosion in the earnings power of the company. We believe it is best to wait for these significant changes to occur before we get more aggressive on the LONG side.

Low-Hanging, Bountiful, Fruit

Looking at the four prior examples of past significant corporate action, it is clear that these companies had similar traits. Specifically, each company had low-hanging fruit and the potential to create significant value for shareholders. Many of these are similar to the opportunities we currently see in Darden:

- Tremendous cash flow potential

- Huge real estate value

- Non-core, under-utilized assets that can be sold at rich valuation

- Core assets represent a classic reorganization opportunity

- Market’s valuation of the whole is far below what we believe the sum-of-the-parts would represent in a reorganization or breakup

- G&A rationalization opportunities

DRI’s Biggest Problem – It’s Too Big, Too Complex, To Perform

- This company has over 2,000 restaurants spread out among 8 separate concepts

- Olive Garden and Red Lobster account for roughly 75% of total revenues

The Complexity Has Led To A Bloated Cost Structure

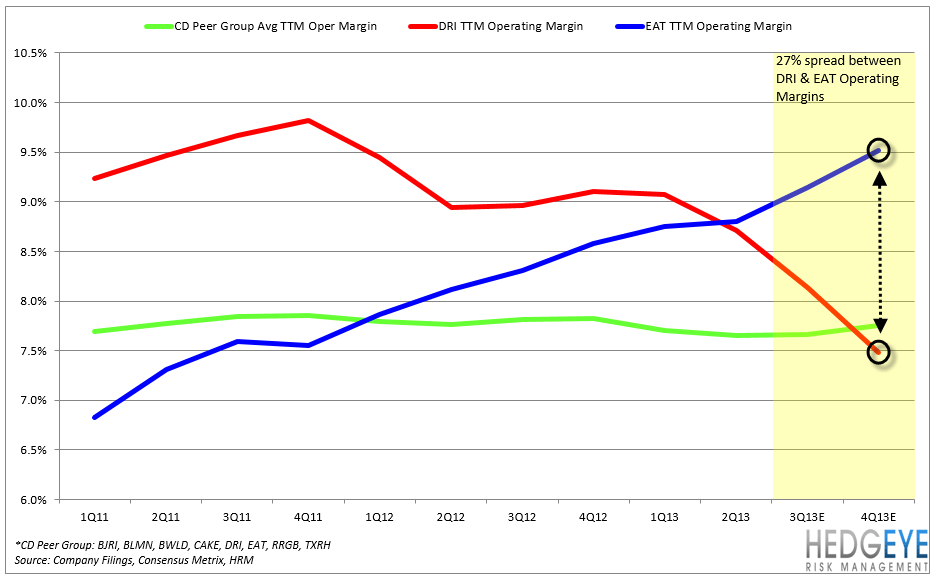

DRI management has contended for years that its multi-concept structure creates operational efficiencies. But, a closer look at the numbers suggests the exact opposite. The average unit volume of DRI’s big three brands is $3.68, which is 23% larger than the average unit volume of EAT’s core brand, Chili’s.

- Restaurant level margins for DRI are 32% larger than EAT’s and 17% larger than the average of its casual dining peers

The math is quite simple. If DRI generates more revenues per store and has higher margins per store than its competitors, then it should generate higher operating profit margins as well. But, this isn’t the case. The only real explanation we can find for DRI’s lower operating margins is a bloated G&A cost structure.

- DRI’s operating margins over the TTM are 7.5%, which is 27.2% below EAT’s and 3.7% below the average of its casual dining peers

- If DRI were to cut G&A by 200 bps, and achieve 9.5% in operating margins, the company would generate an additional $1.10 in earnings per share

Our Vision Of The New DRI

Below we offer our view of what the new Darden should look like. We believe the company should be broken up into three segments – Seafood, Steak and Italian. Yard House should be spun off and taken public and Bahama Breeze should be sold. This would leave each of DRI’s three operating segments with a large brand, in addition to a smaller one in order to help, over time, improve the growth profile of the company. Additionally, each company would finally be able to focus and zero in on their operations, which, we believe, would allow for a more streamlined operating structure.

It’s Only A Matter Of Time – Restaurants Are An Attractive Sector For Activists

- McDonald’s (2006): Real estate was the fulcrum of Bill Ackman’s thesis, but better operating performance, including new management, and capital allocations decisions were the real drivers of returns. The company sold off non-core assets.

- Wendy’s (2008): Real estate was, once again, the anchor of the thesis here, but the business was also undervalued. The company, under the influence of Trian Fund Management’s Nelson Peltz, sold off non-core assets.

- Applebee’s (2006): Breeden Capital Management threatened a proxy contest at the 2007 Annual Meeting of Stockholders, which ultimately was settled with two board seats being opened up for the activist entity. The company was sold following a period of lackluster returns.

- Cracker Barrel (2005): Nelson Peltz, again, held real estate central in his thinking on taking the company private. In 1Q06, the company’s board authorized the use of proceeds from a sale of Logan’s Roadhouse to fund a modified “Dutch Auction” tender offer for $250mm of the company’s common stock (roughly 35% of common shares outstanding).

- Cracker Barrel (2011): Biglari Holdings contested two proxy battles, but has failed to secure any board seats. Pressure from Sardar Biglari led to the replacement of CBRL’s CEO and the stock price has appreciated significantly since BH first took a stake in October 2011, rising from $45 to over $100 a share today.

- DineEquity (2012): Marcato Capital Management suggested a dividend payment in order to maximize its equity value. The company announced a $0.75 quarterly dividend and a $100mm share repurchase, which amounted to 8% of equity value. Richard “Mick” McGuire of Marcato was previously an analyst at Bill Ackman’s Pershing Square Capital Management.

Piecing It All Together

- The current outlook for DRI is dire and we suspect that 1Q14 results will be a disaster

- There is no cohesive plan to fix the asset base and address significant inefficiencies

- As we have seen many times before, continuing deterioration will lead ultimately lead to intervention, in one form or the other

- Given the current trends, the dividend, which was once an asset, could become a liability

- We know how this is going to end, the only question is when?

Howard Penney

Managing Director