This note was originally published September 09, 2013 at 11:36 in Restaurants

We’ve been bearish on the casual dining sector since early June and, on Friday, Black Box gave us a look at August sales trends which showed little improvement from an ugly July.

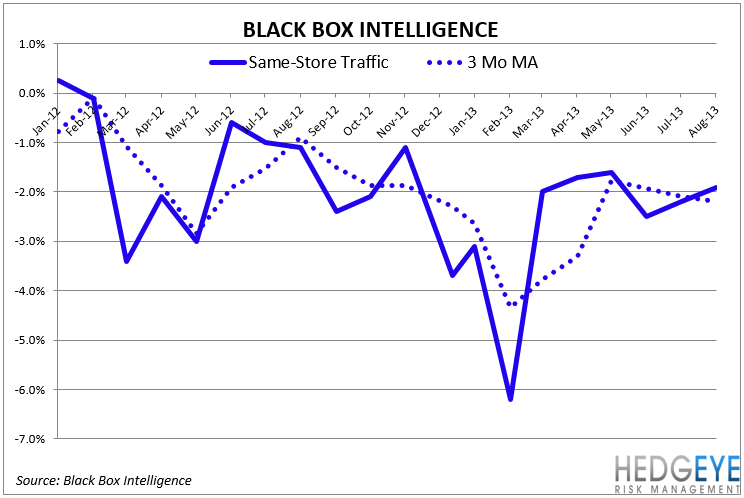

Black Box reported that August 2013 same-restaurant sales declined -0.2%, while comparable traffic trends declined -1.9%—both metrics accelerated 70 bps and 30 bps on a sequential basis, respectively. These estimates come against August 2012 comps of +1.0% and -1.1%, respectively.

Malcolm Knapp also released his August 4-week estimates this weekend. Knapp-Track casual dining same-restaurant sales declined -1.7%, while comparable guest counts declined -3.1%. These results come against full 5-week August 2012 comps of +1.0% and -1.2%, respectively. Knapp will release his 5-week August estimates later this week.

Currently, consensus estimates for the 24 casual dining chains we track in the space are for 3Q13 same-store sales growth of +1.2% (excluding the DRI brands) versus +1.7% in 2Q13. For the first two months of 3Q13, Black Box has reported same-store sales of -0.6%.

With September traditionally being a difficult sales month given the back-to-school trends, it is unlikely we will see a significant uptick in same-store sales.

The following companies saw SSS revised down over the past month: BWLD, CBRL, DRI, EAT, RT.

The following companies saw SSS remain unchanged over the past: BJRI, CAKE, DIN, RRGB, KONA, RUTH, TXRH.