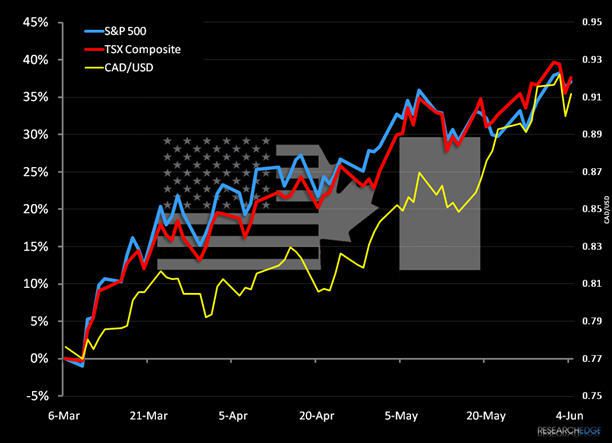

Position: We currently have no position in Canada, though have a bullish bias

We have been consistently bullish of Canada for the last six months. A primary reason actually jumped out at me while watching "X-Men Beginnings: Wolverine" in a theatre earlier this week. (I think I appreciated the movie more than my girlfriend did.) The protagonist, Wolverine, is serving in the U.S. Army in a special platoon and while on a mission in Africa decides to desert. He is confronted by the leader of the platoon who insists that he is serving his country and has taken an oath to do so. Wolverine responds simply, "It doesn't matter, I'm Canadian anyway." In the context of the global investment marketplace, the reason to invest in Canada may be as simple as that, Canada is not the United States (no offense to our American friends!).

While the United States is Canada's largest trading partner, ie Canada will always be dependent on the U.S. economy, Canada is also one of the most resource rich nations in the world. Specifically, based on conventional and non-conventional oil reserves Canada ranks 2nd in the world only to Saudi Arabia. In effect, Canada has what China, "The Client", needs. Further, Canada has a solvent and functioning banking system. The Canadians did not let their underwriting standards slide like the Americans did throughout the 2000s, so the credit system is fully functioning north of the border.

More importantly, Canada plays into our theme of socialism versus capitalism, which is the idea that you want to be long of those countries that are moving towards capitalism and short of those countries that are moving towards socialism. With Conservative Stephen Harper at the helm, the Canada government, despite their socialist roots and tendencies, has been shifting more and more to the economic right. This is, of course, in stark contrast to the United States and its first few months under the tenure of President Obama (and to be fair the last few years under President Bush).

A few points to consider in regards to Canada becoming an appealing nation from an investment perspective are outline below. We've borrowed some of these from a report put together by the Cato Institute and while these facts compare Canada to the United States, the point more broadly is the direction in which Canada is moving from a fiscal policy perspective. These points are as follows:

- Government spending - Canadian government spending as a percentage of GDP peaked at 51% in 1990 and has been steadily declining every since. In 2008, Canadian government spending as a percentage of GDP was 40% versus the United States at 39%. For the first time in modern economic history, the United States government is poised to spend more money as a percentage of GDP in 2009 due to the massive stimulus plan that the American Congress has passed.

- Federal public debt - The Canadians have been steadily bringing down their federal public debt as a percentage of GDP since 1995 when it was at 71%. By the end of 2008, this number was at 32%. In 2008, the U.S.'s ratio of federal public debt as a percentage of GDP was 40% and expected to rise to 61%.

- Balanced budget - Canada has balanced it's budget every year since 1998, and in fact generated a surplus. The American government has run a deficit for that entire period and a time when the Americans will be able to balance their budget again is far, far into the future.

- Social security - Both the Americans and Canadians spend roughly the same on social security, approximately 4.4% of GDP. The Canadians, though, have a plan that is solvent and full funded, while the Americans have massive unfunded obligations.

- Taxes - On the tax front, Canada is and has been lowering taxes, primarily because they have the ability to do so. In 2010, it is expected that the U.S.'s highest personal income taxes rate will be increased to 46%, which is on par with Canada, while Canada has a lower capital gains tax rate. On the corporate front, Canada's tax rate is 15% on the federal level and has been trimmed on the provincial level, which, in aggregate, make Canadian corporate rates lower than the United State's standard 40% rate (a rate that is predicted to go up next year).

Canada has rightfully and always been known as the world's superpower of hockey, but the time seems near when Canada will also be held on a podium for their fiscal prudence and free market policies, especially in contrast to the trend that its southern neighbor is on.

Daryl G. Jones

Managing Director