Bullish: Germany (EWG) and UK (EWU) equities

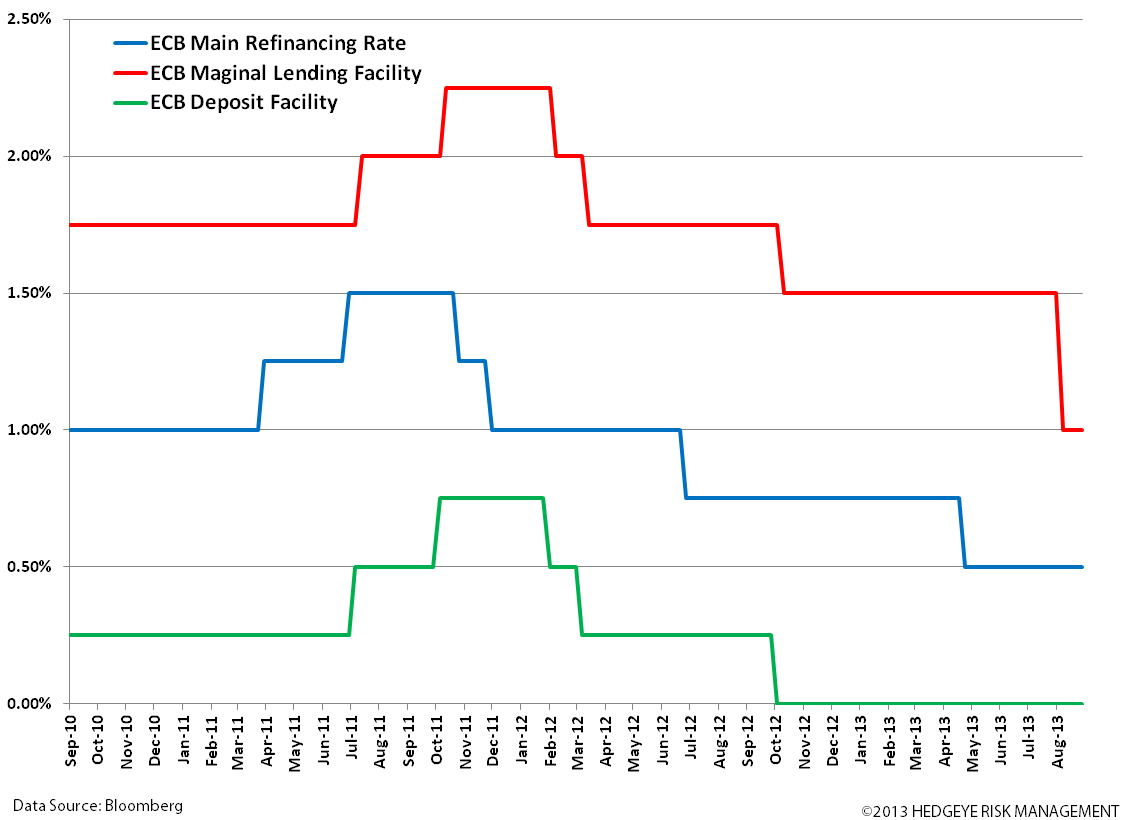

Draghi pivoted substantially in the ECB’s tone on monetary policy expectations in his press conference yesterday in which he kept rates on hold, presenting a dovish tone in which he said that interest rates should remain “at present OR lower levels for an extended period of time.” In his commentary, he referred to the green shoots of economy (terminology he has not used this year) as “very, very green” and that there’s still no indication of domestic demand recovery across the whole of the Eurozone.

In short, Draghi has reset market expectations that were suggesting a hike in rates over the intermediate term, rather than a cut. Our assessments is that Draghi will continue to watch the data roll in and will need a number of months to confirm or change his outlook that could influence his monetary policy stance.

Two pressing areas of concern remain the repayment schedule of LTROs and lack of credit across the region. While the swift repayment of the LTROs has boosted the health of the ECB’s balance sheet, it represents a tightening of liquidity, some of which is reflected in the poor data observed from ECB loans to corporations and households (chart directly below). The larger credit clog across the region should continue to suppress economic expansion and we believe that in the coming months Draghi may issue a facility to better extend loans to small and medium sized enterprises, the lifeblood of the Eurozone economy. [Draghi’s full prepared remarks can be found here.]

UK and Germany Bulls on Gradual Eurozone Improvement

As we’ve noted in previous notes, Eurozone data has improved over recent months, however we’ve tempered expectations that given the still very weak underlying structural state of the Eurozone, in particular the periphery, the data suggests an improvement off the bottom but still at low levels. We see this clearly with PMI results, which we’ve forecast to make mild improvement and hover around the 50 level (dividing contraction and expansion), and outperformance from Germany and the UK given their stronger underlying fundamentals (see the chart below).

We continue to be bullish on German and UK equities. Along with our U.S. call of #RatesRising, we’ve seen a similar trend in many European credit markets, which has solidified our call to stay in equities. Of note, German’s 10yr bund yield reached a high of 2.04% this week (that level was last seen in DEC 2011!) and are up 26bp M/M, while UK 10yr Gilts are up 45bps M/M and France’s 10yr yield is up 30bps M/M. While we expect yields to contract as follow-through to yesterday’s announcement, we do expect rates to remain elevated over the intermediate term as investor push into equities.

EUR/USD

Given Draghi’s shift to a dovish interest rate outlook, we wouldn’t be surprised to see more follow-through selling in the EUR/USD, however we still very much think that Draghi’s OMT firepower has put great support in the common currency and expect the cross to trade in a tight range of $1.29 – $1.33 over the intermediate term.

Below we show CFTC data on the EUR/USD net non-commercial positions outstanding. Regrettably the data is a bit stale (the newest as of 8/27), however the level suggests migration to the neutral level, consistent with an increasingly bullish outlook on the region’s improvement.

An Italian Political Mess on Monday?

As a quick warning as you head into the weekend, we want to make you aware of what may develop on the Italian political front on Monday and the impact it could have on the market. Reuters has suggested that former PM Berlusconi has prepared a video message that could announce a decision (along with his PdL party) to bring down PM Letta’s coalition government (which has been in a tenuous state at best since elections in February) if on Monday the special Senate committee votes to strip Berlusconi of his seat in the chamber.

It’s hard to say just what may be decided on Monday, but certainly the situation creates potentially more downside than upside across Italian capital markets. It’s such political risk that has largely kept us away from taking an investment position in Italy for many months. We’ll sleep deeply this weekend without a position in Italy. We hope you can too.

Enjoy your weekend!

Matthew Hedrick

Senior Analyst