Ahead of this morning’s Employment Report, Keith tweeted “All that matters in the BLS # is the market reaction to it”. That seems especially fitting for the August employment data. There was something for everyone.

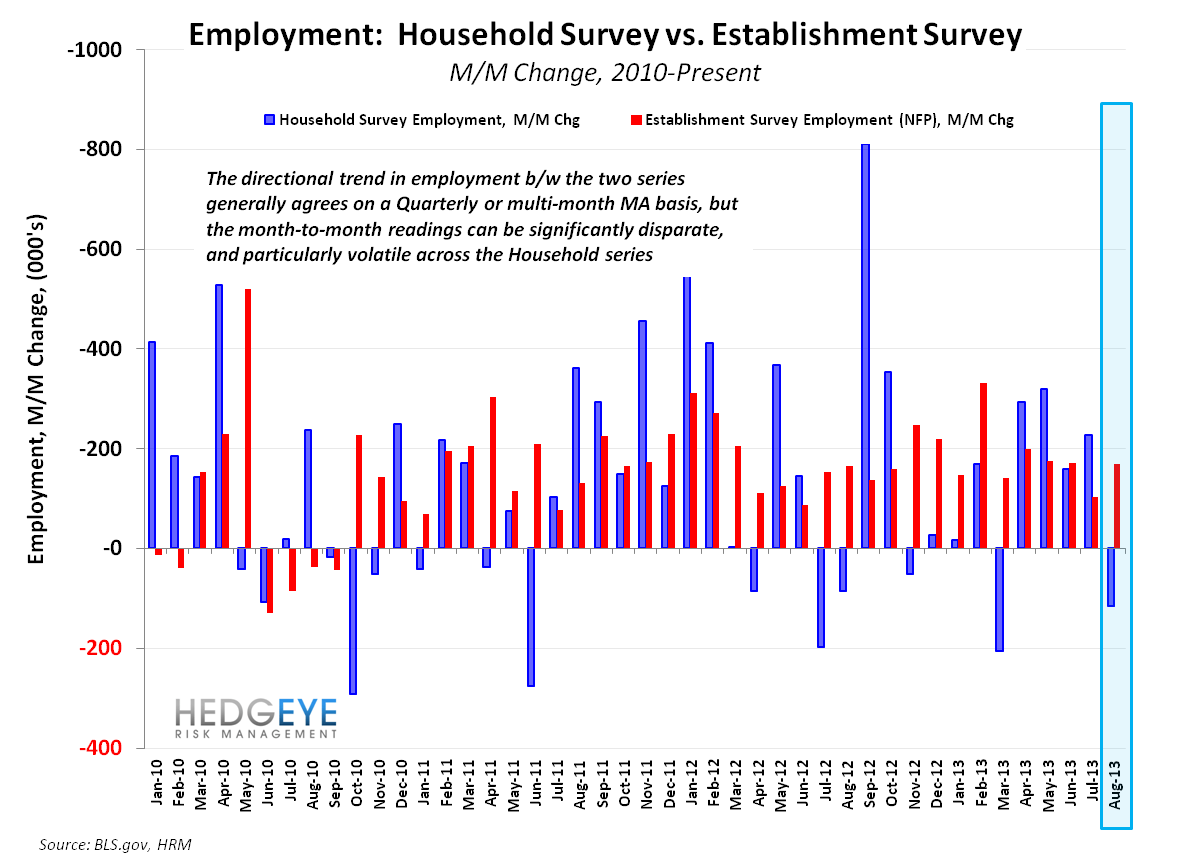

Consider the following: The unemployment rate dropped to 7.3%, but did so on the back of a lower participation rate and negative household employment gains. Private Payrolls declined sequentially and NFP missed estimates, but on a YoY & 2Y growth basis both measures were actually flat to slightly better sequentially. The two month revision was negative at -74K, but PT employment for economic reasons declined, U-6 unemployment fell below 14%, weekly hours ticked higher and hourly earnings accelerated sequentially. The Business Survey (which drives the NFP figure) showed a net gain of +165 but the Household Survey (which drives the Unemployment Rate) showed employment declining by -115K.

What do we do with that equivocality? From a positioning or allocation perspective, not much unless the price signal changes.

The Quantitative Risk Management setup remains positive for equities here and, on balance, today’s data doesn’t materially impact our Trend view of fundamentals – particularly with the initial claims data continuing to show accelerating improvement, the preponderance of domestic macro data in July/Aug strengthening, the seasonal headwind (which impacts the NFP data also) beginning to reverse in September, and a diminishing fiscal drag moving tangibly closer on the timeline.

Maybe there’s a case that today’s data adds some incremental uncertainty to Taper prospects, maybe Putin vs. Obama escalates, maybe Congress delivers a negative policy surprise. Maybe not.

All in, similar to last month, we wouldn’t view today’s employment data in isolation as a real catalyst in either direction.

We provided a more detailed analysis of the Labor Force Participation Rate in today’s Early Look. You can link to that here >> Early Look: Cyclical vs. Secular

A summary review of the August Employment data below:

NFP: Net Non-Farm payrolls gained sequentially coming in at +169K - holding flat on a YoY growth basis at +1.65% and accelerating marginally to 1.67% on a 2Y basis

NFP Revision: The net two month revision was -74K with June revised from +188K to 172K and July revised from +162K to +104K.

Household Survey: The net employment gain as measured by the Household Survey was negative at -115K vs. +227K in July

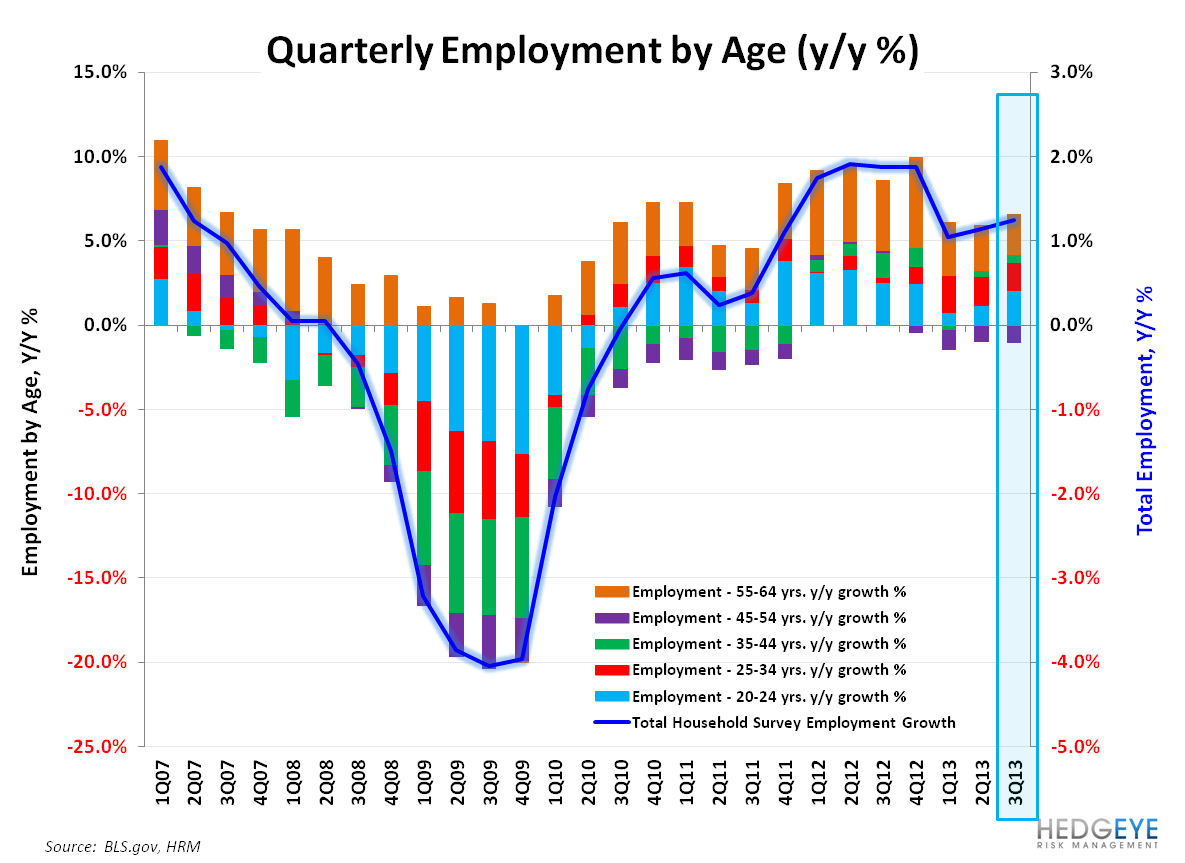

Employment by Age: Employment growth accelerated for 20-24 yr. olds and 65+ yr olds, decelerated for 55-64 year olds, and held flat for the balance of age cohorts

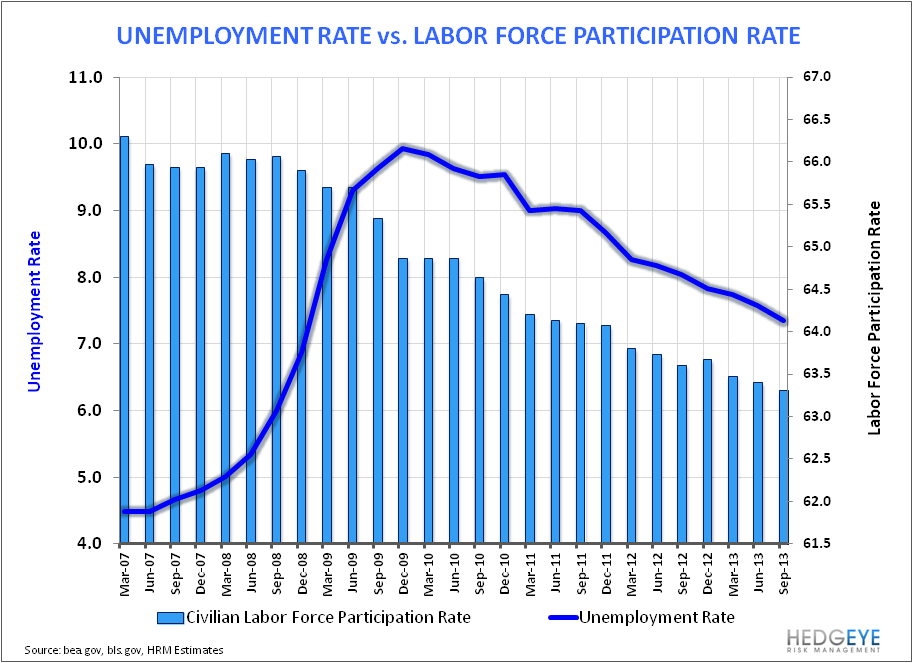

Unemployment Rate: The Unemployment Rate dropped to 7.3% from 7.4% as the total labor force declined -312K alongside a -198K decline in Total Unemployed and -115K decline in Total Employed.

Labor Force Participation: A positive +203K change in the working age population alongside a net decline in the labor force pushed the Labor Force Participation Rate down to 63.22% from 63.40%.

Part-time/Temp Employment: Part-time employment declined by -234K while Temp employment gained +13K, registering its 11th consecutive month of net gains.

Industry Employment: Information and Finance were the only losers with employment declining 18K and 5K, respectively in August. Manufacturing gained +14K on the month, reversing a 5 month run of net job loss.

Ave Weekly Hours for Private Employees: Hours increased to 34.5 from 34.4 MoM and were up 0.1 vs year ago levels.

Christian B. Drake

Senior Analyst