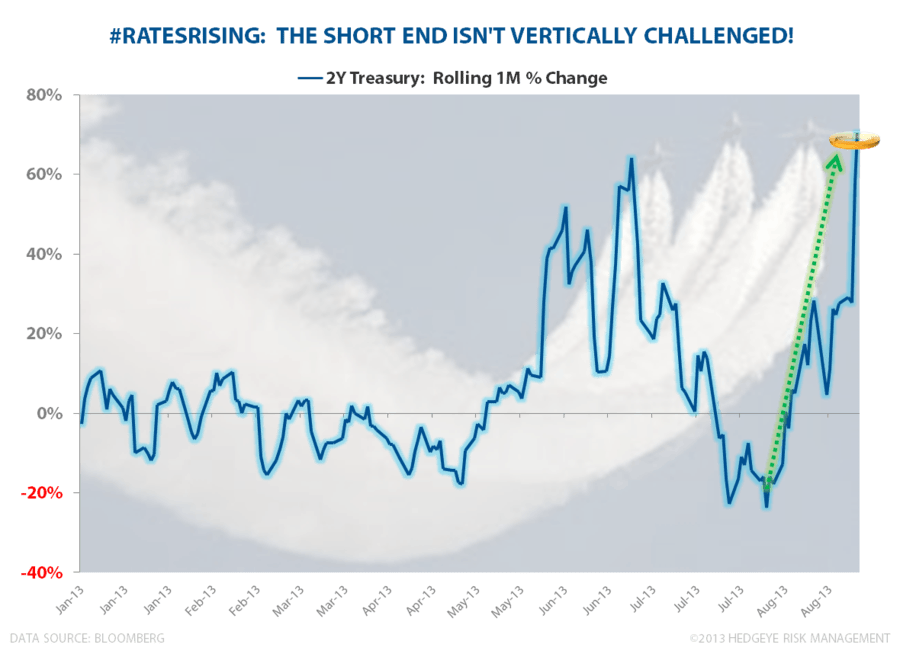

As you may have already guessed, I spend more time worrying about the long-end of the yield curve (Ben Bernanke marks the short end to model). But that hasn't stopped the 2-year yield from putting on a monster rip show in the last few weeks to 0.48%.

What exactly constitutes a big rip? How about a 60% surge in a month.

Look, lots of (most?) people don’t model entropy risk on a percentage basis. We do here at Hedgeye. It works.

Got #RatesRising yet?