Taking a Quick Win

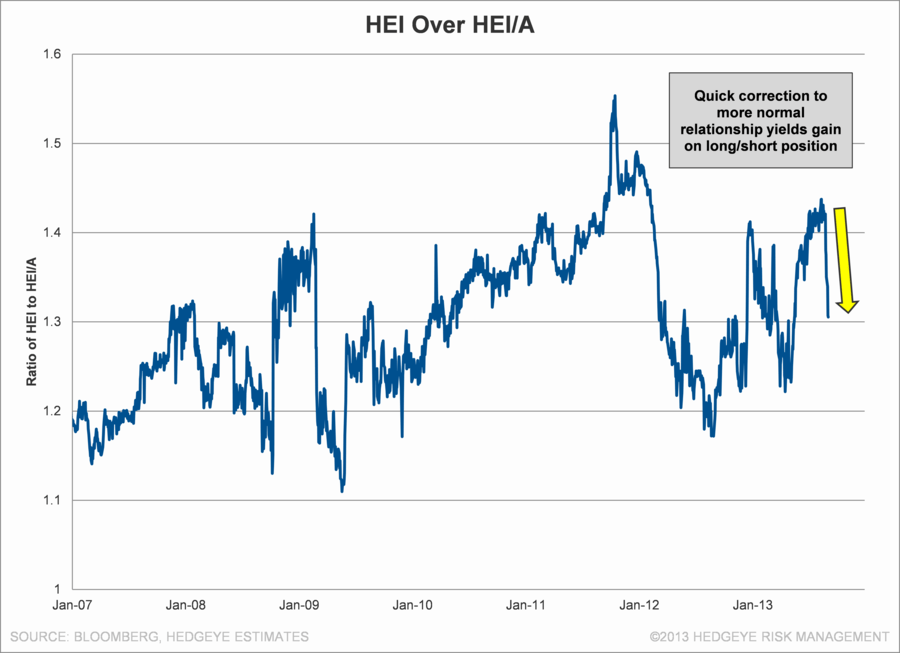

We put out a note here suggesting a short HEI, long HEI/A pair. At the time, the HEI premium was abnormally large and the extra votes for the common shares at Heico do not have much value for the average shareholder. The HEI premium has dropped about 12% since our 8/27/13 note, which is an excellent annualized return for a well matched pair. If readers have an interest in these kinds of trades, please ping us for background. There is no shame in generating some alpha the easy way.

Jay Van Sciver, CFA

Managing Director

HEDGEYE RISK MANAGEMENT

111 Whitney Avenue

New Haven, CT 06510