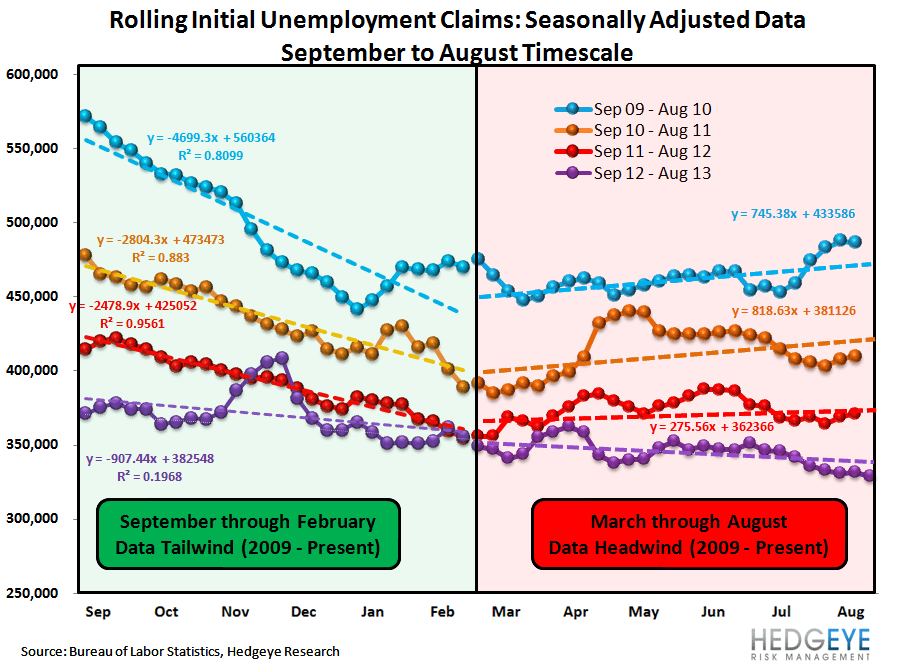

Remarkably Consistent

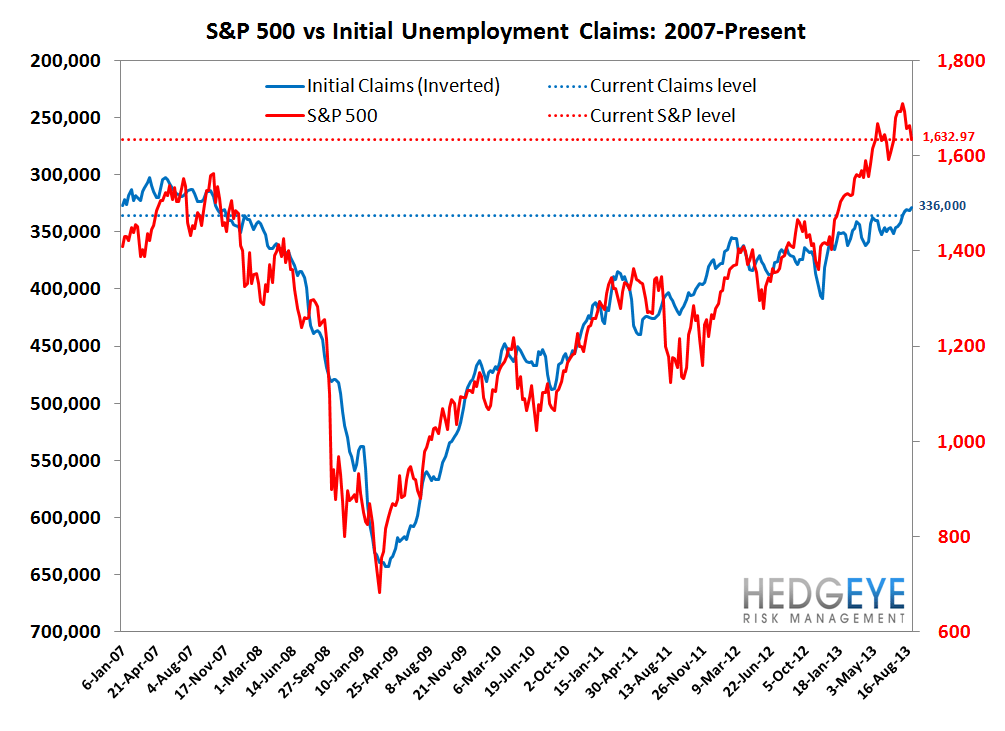

We're beginning to feel like a broken record with our call on initial jobless claims, stating almost every week how the data is improving at an accelerating rate. This week's data again reflects that trend. Nevertheless, we urge investors to continue to care. Why? With the broader market, and the Financials sector alongside it, gripped in uncertainty over whether we're poised for a meaningful correction, we continue to regard the claims data as the strongest indicator supporting our ongoing bullish bias and buy-the-dip view. Regrettably for those waiting patiently, there hasn't really been much of a dip.

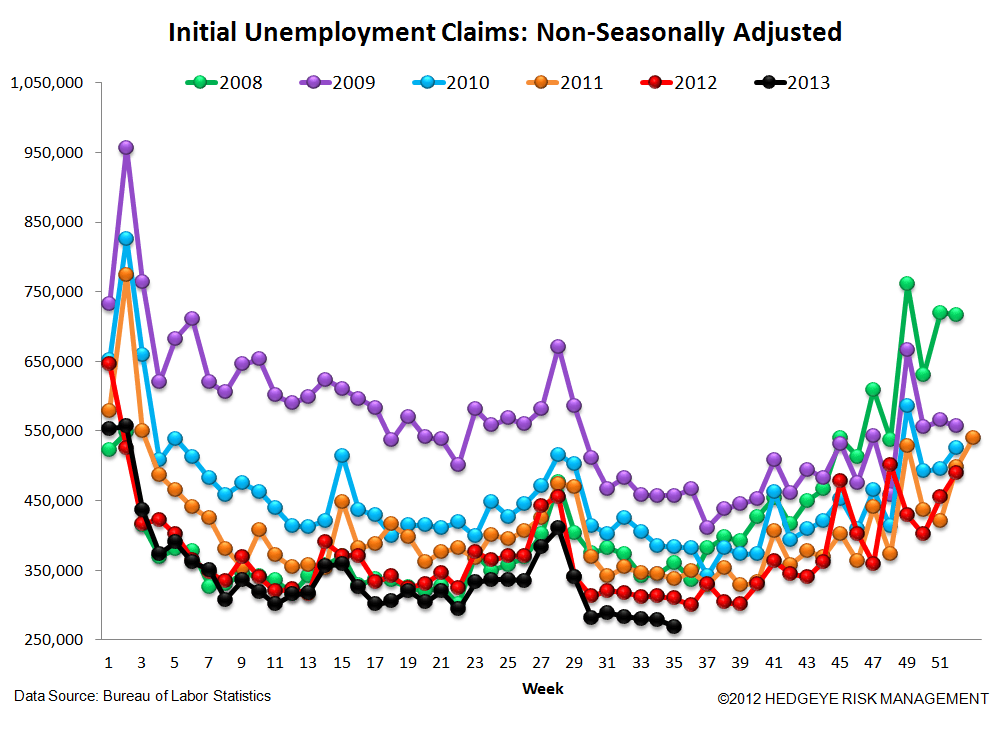

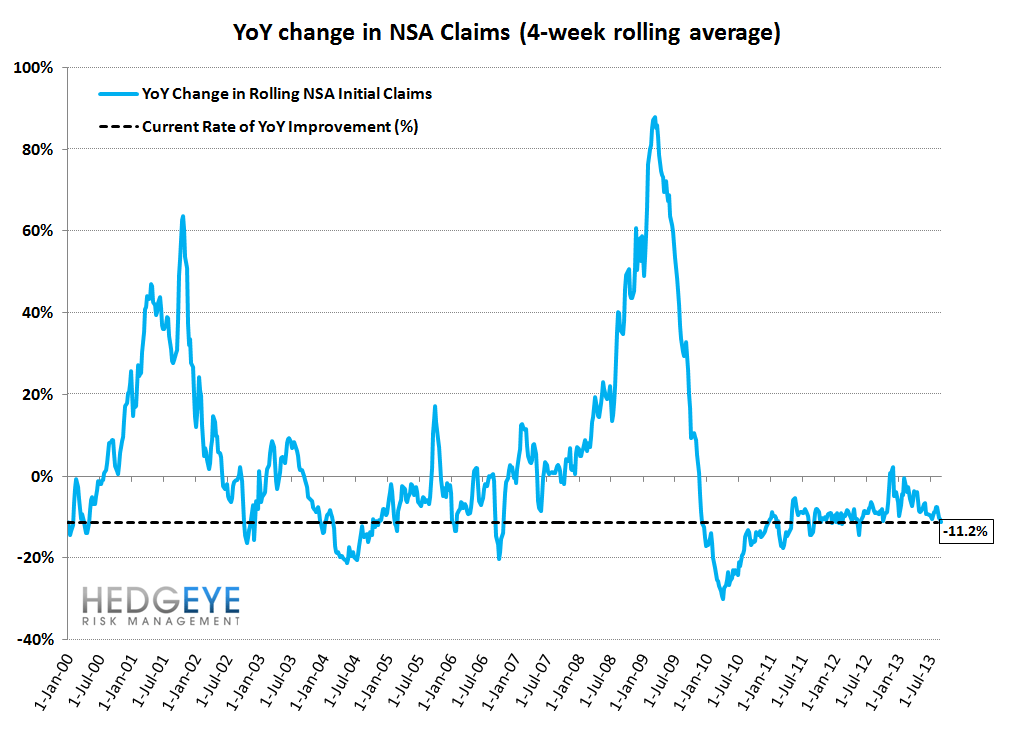

The bottom line is that the labor market is humming along nicely at this point with rolling NSA claims down 11.2% Y/Y, the fastest rate of improvement since May, 2012. Additional anecdotal evidence continues to emerge that at least a portion of the broadening base of employment is a reflection of employers responding to Obamacare. The bottom line, however, is that the labor market tends to be very self-reinforcing. Baring a significant external shock, we see little reason to expect the current trajectory to deviate from its trend.

As we've stated previously, we continue to think that credit-levered financials remain the best plays amid an accelerating rate of improvement in employment. Two of our favorite ideas on this theme remain Capital One (COF) and Bank of America (BAC).

The Data

Prior to revision, initial jobless claims fell 8k to 323k from 331k WoW, as the prior week's number was revised up by 1k to 332k.

The headline (unrevised) number shows claims were lower by 9k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -3k WoW to 328.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -11.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -10.4%

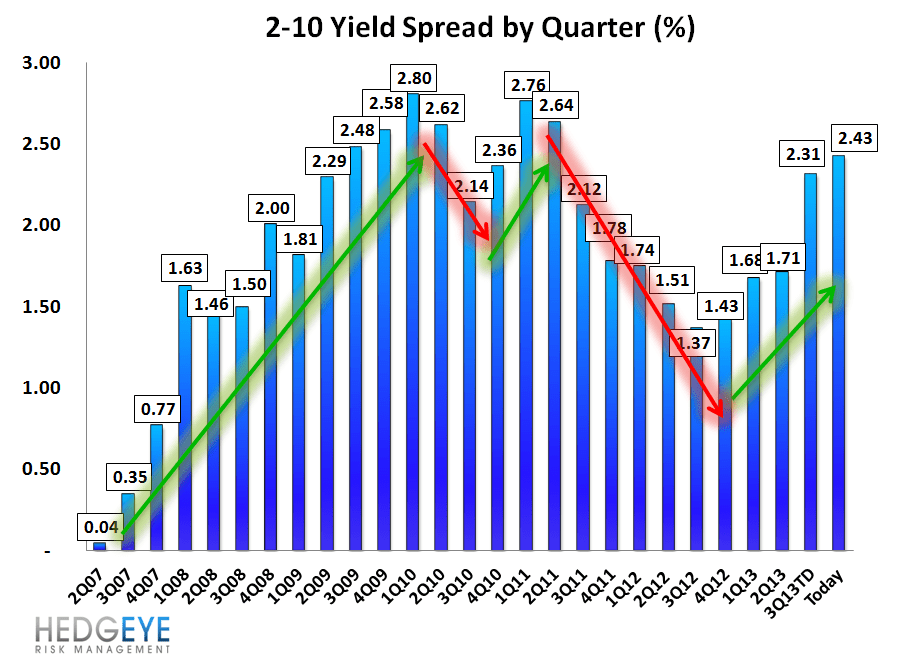

Yield Spreads

The 2-10 spread rose 7 basis points WoW to 243 bps. 3Q13TD, the 2-10 spread is averaging 231 bps, which is higher by 61 bps relative to 2Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT